Key Points

Record-Breaking Markets: The S&P 500 achieved its ninth record close of 2025 at 6,297.36, while the Nasdaq logged its fourth consecutive record high, driven by technology sector strength and positive economic data.

Cryptocurrency Surge: Bitcoin reached a new all-time high above $122,000 before pulling back to $116,500 as traders took profits, while Ethereum soared above $3,400 following Peter Thiel's investment in BitMine.

Inflation Concerns: US CPI inflation accelerated to 2.7% year-over-year in June, the highest reading of 2025, fueling concerns about tariff-driven price pressures and Federal Reserve policy implications.

Corporate Developments: Nvidia surged 4% after announcing the resumption of H20 chip sales to China, while Lucid jumped 36% on a $300 million robotaxi partnership with Uber.

Banking Sector Mixed: JPMorgan reported a 17% profit decline but beat estimates, while Goldman Sachs crushed earnings expectations with record equities trading revenue.

Overview

The week of July 14-18, 2025, was characterized by remarkable market resilience and record-breaking performance across major indices, despite emerging inflationary pressures and ongoing trade tensions. The financial markets demonstrated their ability to navigate complex macroeconomic challenges while maintaining bullish momentum, with technology stocks leading the charge and cryptocurrency markets reaching new milestones. This period highlighted the market's confidence in economic fundamentals, corporate earnings strength, and the continued appeal of risk assets amid evolving policy landscapes.

Financial Markets Weekly Recap

Equities

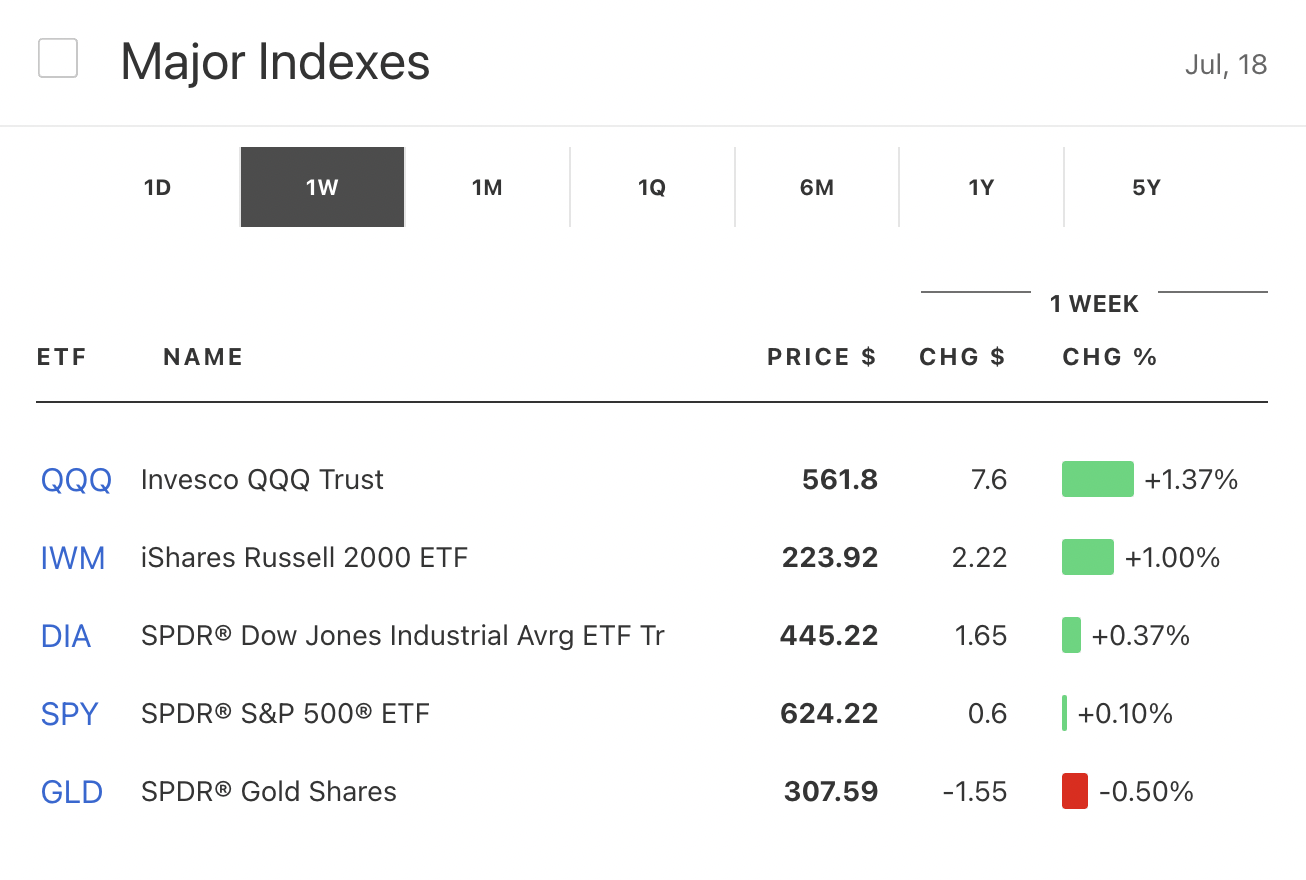

Market Indices: The S&P 500 delivered an impressive performance, closing at 6,297.36 with a 0.54% gain on Thursday alone, marking its ninth record close of 2025. The index has now gained 11.05% since President Trump's tariff announcements in April, demonstrating remarkable resilience in the face of trade policy uncertainty. The Nasdaq Composite was the standout performer, achieving four consecutive record closes during the week and reaching its tenth record high of 2025 at 20,884.27. The technology-heavy index benefited significantly from semiconductor strength and artificial intelligence optimism. The Dow Jones Industrial Average experienced more volatility, falling 436 points on Tuesday due to inflation concerns and mixed bank earnings before recovering to close higher by week's end.

Sector Performance: The technology sector dominated market leadership, with the Technology Select Sector SPDR Fund gaining over 1% on multiple sessions. Semiconductor stocks were particularly strong, with the Philadelphia Semiconductor Index reaching new highs. The financial sector showed mixed results, with investment banks like Goldman Sachs outperforming traditional commercial banks. Energy stocks remained relatively stable despite geopolitical tensions, while consumer discretionary stocks benefited from strong retail sales data showing a 0.6% jump in June.

Corporate Highlights:

Nvidia: The artificial intelligence chip giant surged 4% to reach a new record high after CEO Jensen Huang announced the company's plans to resume H20 chip sales to China. This development came after assurances from the U.S. government regarding export license approvals, marking a significant reversal from the previous restrictive stance. The company's market capitalization now exceeds $4.2 trillion, maintaining a $400 billion lead over Microsoft.

Rocket Lab: The space company experienced a dramatic 8% surge to a record high of $42, extending its one-year gains to an astronomical 650%. The rally was fueled by Citi's upgrade with a price target increase to $50, betting on the company's long-term revenue potential from launch contracts and satellite construction projects.

Lucid Motors: Shares rocketed 36% on news of a $300 million investment from Uber for a luxury robotaxi fleet. The partnership aims to deploy over 20,000 autonomous Lucid vehicles over six years, representing a potential doubling of the company's expected 2025 production.

Netflix: Despite reporting record quarterly revenue of $11.08 billion and raising its full-year outlook, shares dipped 2% as investors wanted more than just a beat. The company warned of margin compression in the second half due to higher content costs.

Currencies

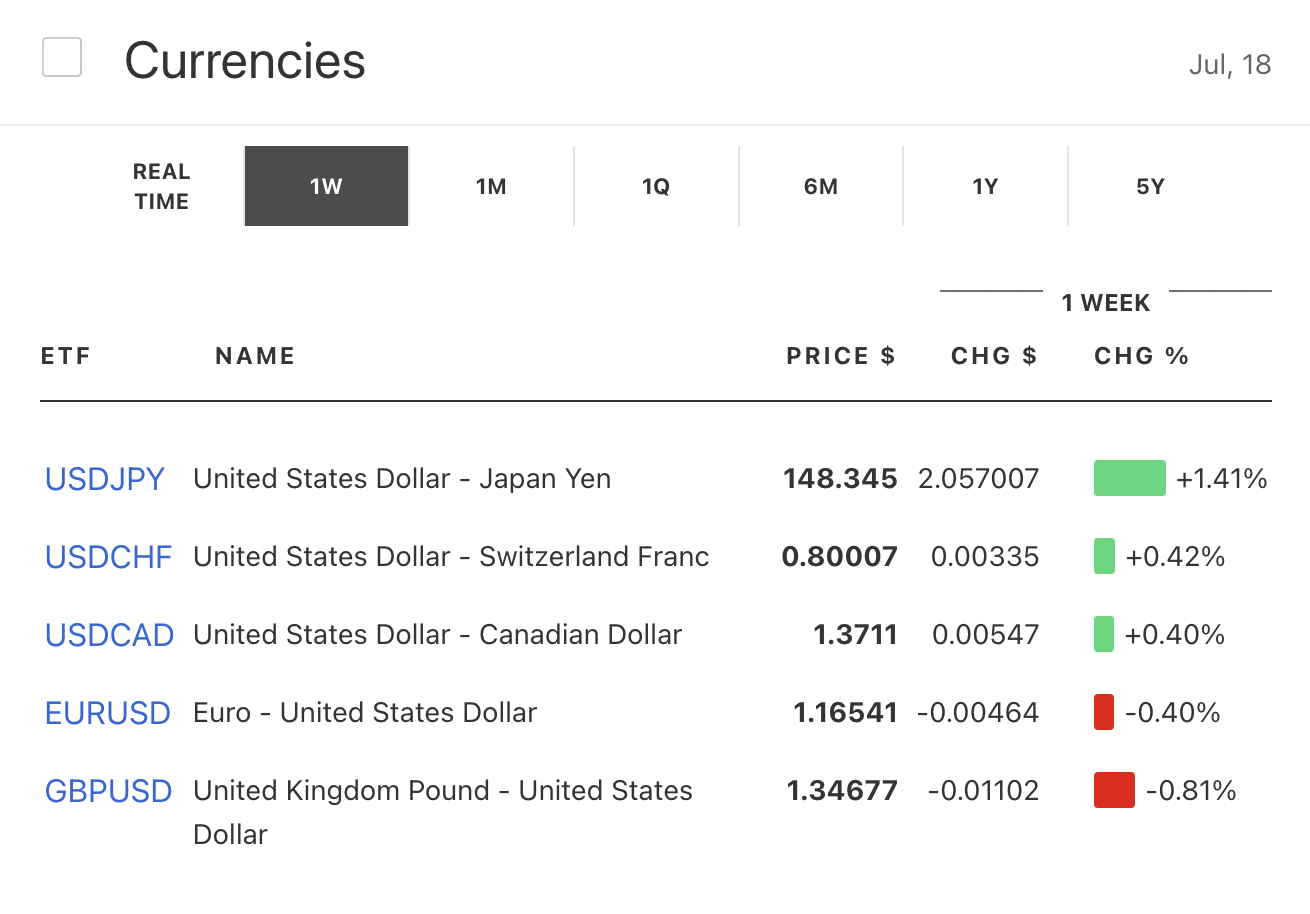

US Dollar: The dollar index showed resilience, bouncing from four-year lows near 96.30 to trade around 98.00 as forex traders digested the implications of rising inflation data. The greenback's strength was supported by safe-haven demand amid trade tensions and speculation about Federal Reserve policy adjustments.

EUR/USD: The euro demonstrated surprising strength, recovering to $1.17 despite Trump's announcement of 30% tariffs on EU imports starting August 1. European Commission President Ursula von der Leyen warned of proportionate countermeasures, setting the stage for potential trade escalation.

GBP/USD: Sterling surged above $1.34 after UK inflation data showed a surprise jump to 3.6% in June, well above the expected 3.4%. The hotter-than-expected inflation reading complicated the Bank of England's easing path and supported the pound against dollar weakness.

USD/JPY: The Japanese yen maintained relative stability as markets weighed competing factors of U.S. dollar strength and global risk sentiment shifts.

Commodities

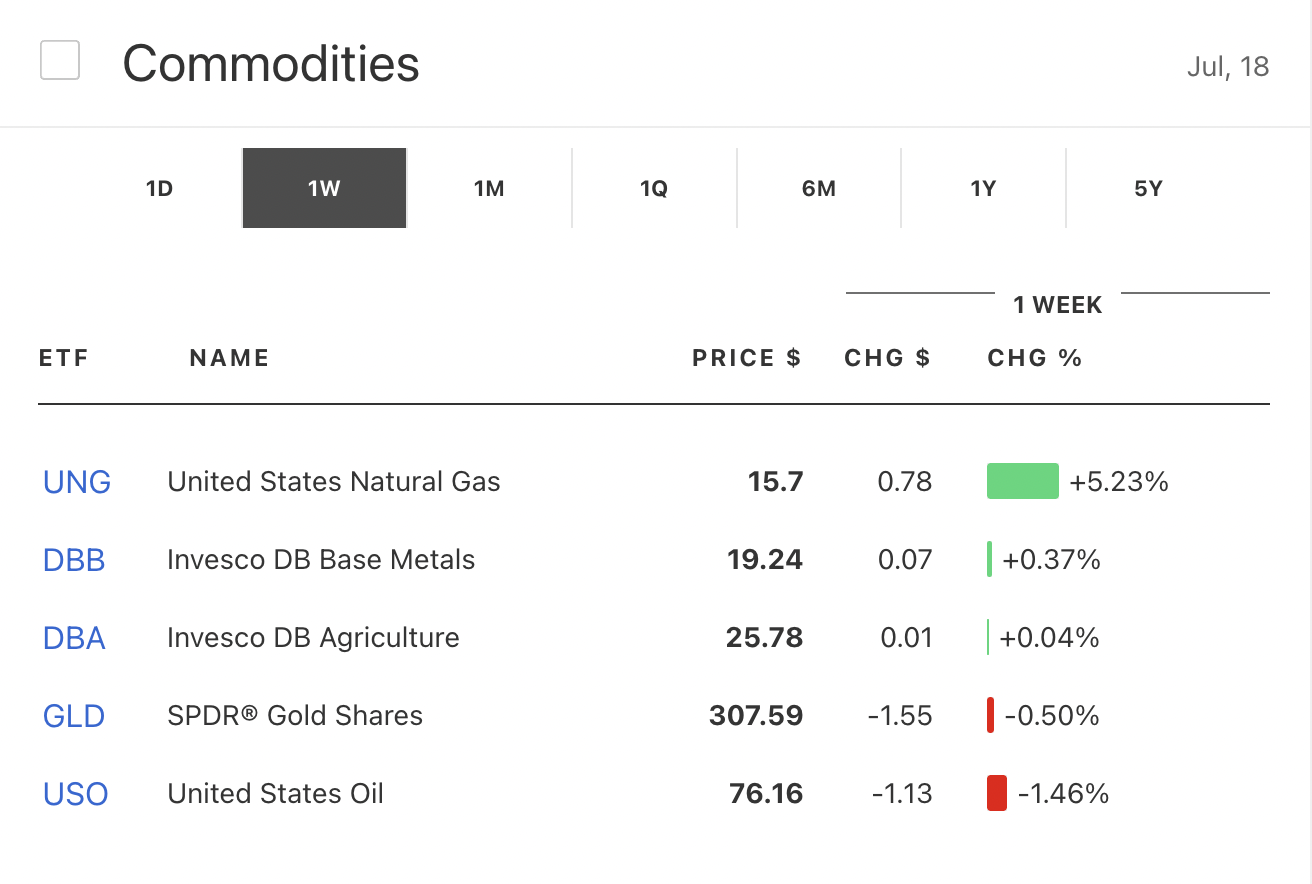

Gold: Gold prices experienced significant volatility, initially rallying on rumors that Trump was preparing to fire Fed Chair Jerome Powell, before erasing gains when the speculation proved unfounded. The precious metal closed the week at $3,325 per ounce, down 1.1% as dollar strength and reduced safe-haven demand weighed on prices.

Oil: West Texas Intermediate crude oil gained 0.6% to $66.75 per barrel, supported by geopolitical tensions and supply concerns, though remaining within recent trading ranges.

Cryptocurrencies

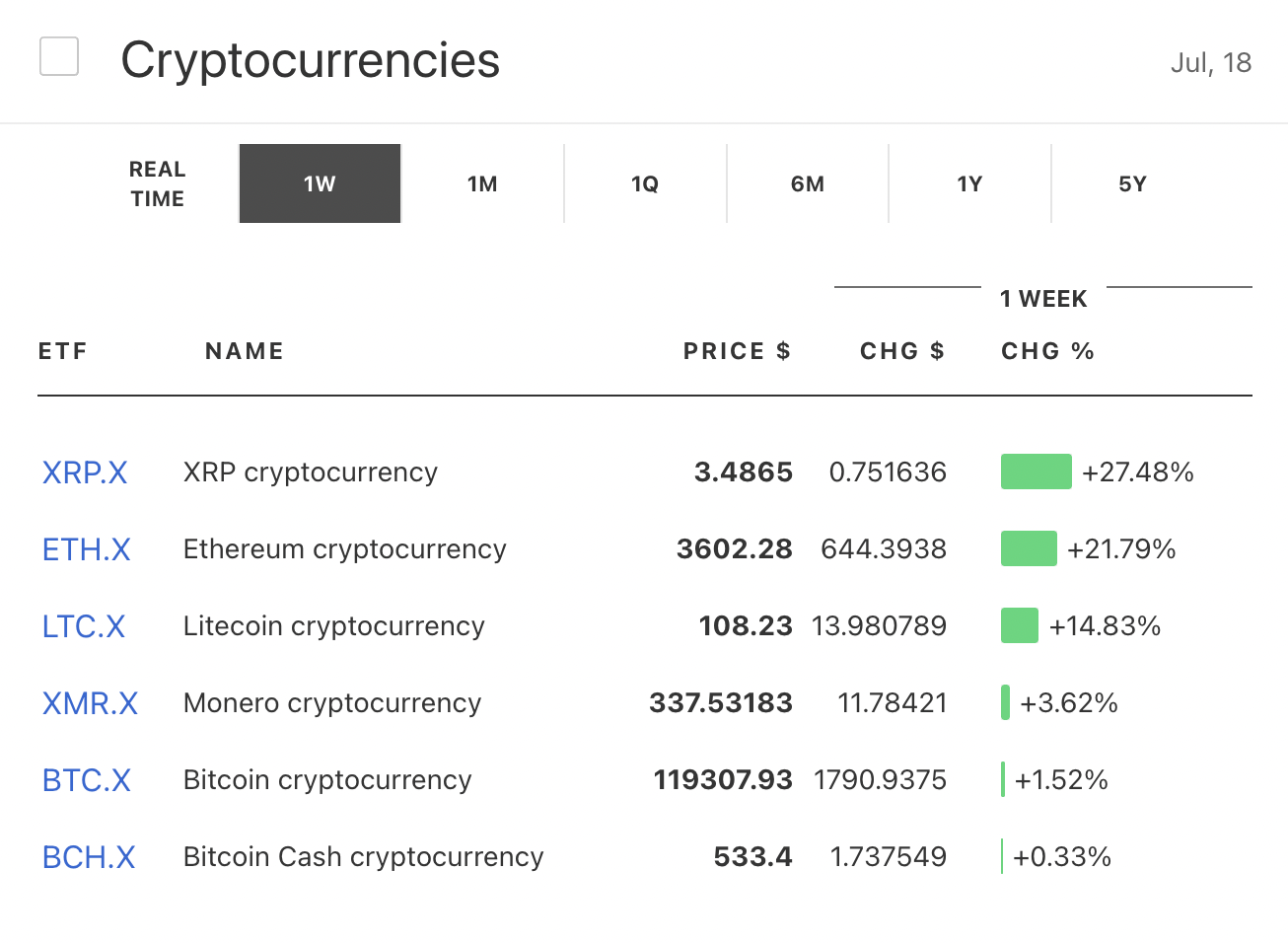

Bitcoin: The flagship cryptocurrency achieved a historic milestone, reaching a new all-time high above $122,000 on Monday before experiencing a classic profit-taking pullback to $116,500. The surge was driven by institutional demand, with Bitcoin ETFs seeing over $2.7 billion in inflows during the week. The cryptocurrency maintained its year-to-date gain of approximately 30%, significantly outperforming traditional asset classes.

Ethereum: The second-largest cryptocurrency surged above $3,400, marking a six-month high as Peter Thiel disclosed a 9.1% stake in BitMine, a company holding over $500 million worth of Ethereum. The move signaled growing institutional interest in Ethereum as a treasury diversification asset.

Economic Indicators and Policy Developments

US Inflation Data: The Consumer Price Index for June rose 2.7% year-over-year, marking the highest inflation reading of 2025 and exceeding expectations of 2.6%. The month-over-month increase of 0.3% represented a clear acceleration from May's 0.1% gain, raising concerns about tariff-driven price pressures. Core inflation also accelerated to 2.9% annually, complicating the Federal Reserve's policy outlook.

UK Economic Data: The UK inflation rate jumped to 3.6% in June, surpassing expectations of 3.4% and marking an uptick from May's 3.4%. Core inflation rose to 3.7% year-over-year, indicating persistent underlying price pressures that could influence Bank of England policy decisions.

US Consumer Spending: Retail sales provided a strong positive surprise, rising 0.6% in June—triple the expected 0.2% increase. This robust consumer spending data reinforced the narrative of economic resilience and supported market optimism about corporate earnings prospects.

Labor Market Strength: Initial jobless claims fell to 221,000, down 7,000 from the previous week, demonstrating continued labor market tightness and supporting the case for economic stability.

Geopolitical and Trade Developments

US-China Trade Relations: President Trump's announcement that Nvidia would be permitted to resume H20 chip sales to China marked a significant shift in trade policy. This development came after intense lobbying by CEO Jensen Huang, who argued that restricting sales would only benefit Chinese competitors like Huawei.

European Union Tariffs: Trump's announcement of 30% tariffs on EU imports starting August 1 created new trade tensions, though markets showed resilience as investors bet on potential last-minute negotiations similar to previous trade disputes.

Cryptocurrency Legislation: The House of Representatives prepared for "Crypto Week," with discussions on three major bills: the GENIUS Act for stablecoin regulation, the Digital Asset Market Clarity Act for comprehensive cryptocurrency framework, and the CBDC Anti-Surveillance State Act to prevent Federal Reserve digital currency issuance.

Corporate Earnings and Financial Sector Performance

Banking Sector Results: The second-quarter earnings season kicked off with mixed results from major financial institutions. JPMorgan Chase reported a 17% decline in profit to $14.9 billion, largely due to the absence of last year's $7.9 billion Visa stake gain, but still beat analyst expectations. Wells Fargo disappointed with lowered net interest income forecasts, causing shares to slide 5%. In contrast, Goldman Sachs delivered outstanding results with $14.58 billion in revenue, significantly above the $13.5 billion expected, driven by record equities trading revenue of $4.3 billion.

Technology Earnings Preview: Taiwan Semiconductor provided positive signals for the broader tech sector, reporting record quarterly profits and strong AI chip demand, which lifted U.S. semiconductor stocks across the board.

Market Outlook

As markets head into the following week, several key factors will influence direction:

Federal Reserve Policy: The hotter-than-expected inflation data has complicated the Fed's easing path, with markets now pricing in approximately 54% odds of a September rate cut, down from previous expectations. Fed Chair Powell's potential dismissal rumors, though later dismissed by Trump, highlighted the ongoing political pressure on monetary policy.

Earnings Season Continuation: The focus will shift to major technology companies' earnings reports, with investors particularly interested in AI-related revenue growth and guidance. The strong performance of Taiwan Semiconductor has set high expectations for the broader tech sector.

Trade Policy Implementation: Markets will closely monitor the August 1 tariff deadline for EU imports and any potential breakthrough in negotiations. The resolution of trade tensions remains crucial for global supply chain stability and inflation expectations.

Cryptocurrency Regulatory Framework: The progression of cryptocurrency legislation through Congress could provide significant catalysts for digital asset markets, with potential for increased institutional adoption and clearer regulatory guidelines.

The week demonstrated the market's remarkable ability to digest complex information flows while maintaining upward momentum. Record-high closes across major indices, combined with strong economic data and corporate earnings beats, suggest underlying economic strength despite emerging challenges. However, the acceleration in inflation and ongoing trade tensions present potential headwinds that will require careful navigation in the coming weeks.

The financial markets' performance during this period reflects a mature bull market that has learned to balance optimism with caution, technological innovation with traditional economic fundamentals, and policy uncertainty with corporate execution. As we move forward, the sustainability of these gains will depend on the market's ability to continue adapting to an evolving economic and policy landscape.