Week (November 25 - 29) in Review: Financial Leaders

The week of November 25-29, 2024, brought notable shifts in market trends and investor sentiment. Small-cap stocks, represented by the IWM (Russell 2000), outperformed other indices with a stellar 4.50% weekly gain. This rise reflects growing optimism about the U.S. domestic economy, likely fueled by upbeat economic data or easing recessionary fears. Technology stocks, measured by the QQQ (NASDAQ 100), continued to attract investors, gaining 1.86%. Meanwhile, the SPY (S&P 500) and DIA (Dow Jones Industrial Average) rose 1.67% and 1.99%, respectively, demonstrating broad market strength.

A striking element of the week's market dynamics was the contrasting volatility trends. While the VIX (S&P 500 volatility index) and VXN (NASDAQ 100 volatility index) saw sharp declines of 5.58% and 6.35%, respectively, the RVX (Russell 2000) and VXD (Dow Jones volatility index) increased by 4.60% and 4.61%. This divergence underscores a nuanced investor outlook—cautious optimism for small-cap and Dow stocks amidst broader stability in large-cap and tech markets.

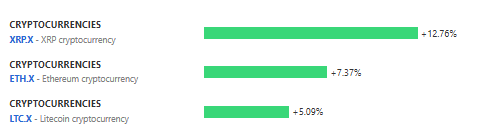

In commodities, United States Natural Gas (UNG) dropped sharply by 6.37%, reflecting potential oversupply concerns or weak seasonal demand. Cryptocurrencies, however, had an excellent week, with XRP surging 13.63%, Ethereum (ETH) gaining 7.40%, and Litecoin (LTC) up 5.24%. These trends highlight renewed interest in digital assets amid ongoing developments in blockchain technology and regulatory clarity.

Global Overview

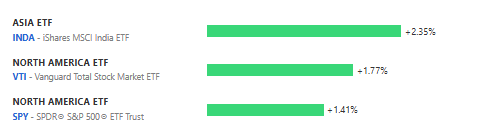

The global financial landscape exhibited mixed performance across regions and asset classes. In North America, the SPY and QQQ reinforced the strength of U.S. equities, gaining 1.41% and 1.86%, respectively. In Asia, the INDA (iShares MSCI India ETF) recorded a solid 2.35% increase, driven by strong corporate earnings and favorable macroeconomic data. Conversely, Latin America struggled; the EWZ (iShares MSCI Brazil ETF) dropped 2.58%, and the BRF (VanEck Brazil Small-Cap ETF) lost 2.57%. Weak commodity prices and political uncertainties likely contributed to this downturn.

Cryptocurrency markets also stood out globally, with XRP, ETH, and LTC gaining double and high single digits. This trend signals heightened investor interest in decentralized finance (DeFi) and evolving blockchain ecosystems.

Sector Overview

The week's sectoral performance reflected shifting investor priorities:

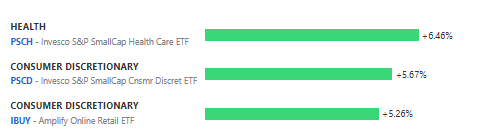

Top Performers

- Healthcare: The PSCH (Invesco S&P SmallCap Health Care ETF) led the gains with a 6.46% increase, signaling robust performance among small-cap healthcare companies.

- Consumer Discretionary: ETFs like the PSCD (+5.67%) and IBUY (+5.26%) surged as consumer spending trends remained resilient, driven by holiday shopping momentum and strong online retail activity.

Lagging Sectors

- Energy: The XLE (Energy Select Sector SPDR ETF) declined by 1.27%, as oil and gas markets experienced pressure from weaker demand forecasts.

- Materials: REMX (VanEck Rare Earth & Strategic Metals ETF) slipped by 0.99%, reflecting concerns about industrial demand in the face of slowing global growth.

International Overview

International markets mirrored the divergence seen in domestic sectors. In Asia, India's equity markets were buoyed by improving economic fundamentals, with the INDA ETF climbing 2.35%. However, Latin America faced headwinds, with the EWW (iShares MSCI Mexico ETF) down 2.29%. Currency weakness and subdued investor sentiment were likely contributors.

Market Volatility for QQQ, SPY, DIA, and IWM

Volatility indices revealed unique insights into investor sentiment:

- The QQQ and SPY benefitted from reduced fear in large-cap and tech markets, evidenced by declines in the VXN (-6.35%) and VIX (-5.58%).

- Conversely, the IWM and DIA faced rising caution, with the RVX and VXD up 4.60% and 4.61%, respectively. This divergence suggests lingering risks in small-cap and Dow-heavy industries despite broader optimism.

U.S. Market Performance and Rising Volatility: A Look into November 2024

The U.S. markets maintained their bullish trajectory in November, with the IWM leading gains at 4.50%. The sectoral breakdown indicates a tilt toward growth-oriented investments, especially in tech and consumer discretionary spaces. However, the uptick in RVX and VXD highlights investors' ongoing hedging against potential market disruptions, possibly stemming from geopolitical tensions or upcoming policy announcements.

Summary

The week ending November 29, 2024, showcased a mix of optimism and caution across markets. While small-cap and tech stocks dominated the gains, volatility indicators and lagging sectors hinted at underlying risks. Cryptocurrencies stood out with robust performance, reflecting growing confidence in blockchain innovation. Sectoral winners like healthcare and consumer discretionary ETFs highlight shifting investor priorities, while energy and materials remain under pressure.

As markets head into December, investors should monitor emerging risks, such as macroeconomic uncertainties and geopolitical developments, which could disrupt this rally.