Week (September 23 - 27) in Review: Financial Leaders

Interesting Facts and Market Dynamics

The week of September 23-27 saw global markets demonstrate resilience, with notable gains across major equity indices and significant movements in sector-specific ETFs. This period was characterized by increased investor optimism, as both large-cap and small-cap stocks exhibited strong performance. Key factors influencing this sentiment included lower-than-expected inflation data, bolstered corporate earnings, and stabilizing economic indicators. The technology-heavy Nasdaq (QQQ) and the broader S&P 500 (SPY) contributed significantly to the market's upward momentum, while small-cap stocks (IWM) outpaced large-cap indices, highlighting renewed confidence in growth-oriented companies.

On a macro level, the dip in volatility indices such as the VIX and VXN reflects decreased market uncertainty. The substantial drop in the RVX index for small-cap stocks (-14.47%) suggests that investors are becoming less concerned about risks in the small-cap sector. However, the slight increase in the VXD for the Dow Jones points to lingering caution around blue-chip stocks.

Global Overview

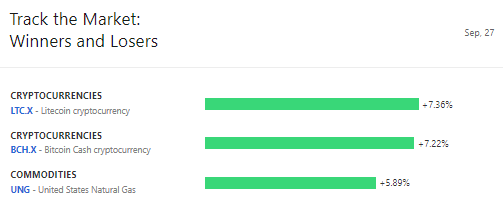

During the week, various global markets showed mixed results across asset classes. In the cryptocurrency space, Litecoin (LTC.X) and Bitcoin Cash (BCH.X) emerged as strong performers, gaining 7.46% and 7.01%, respectively. On the other hand, Monero (XMR.X) experienced a significant decline of 6.42%, pointing to selective investor interest within the crypto market.

Commodity markets were also active. United States Natural Gas (UNG) posted a notable 5.89% gain, reflecting tightening supply concerns as colder weather forecasts emerged. Conversely, United States Oil (USO) dropped by 5.14%, as global demand concerns and increased crude inventories weighed on oil prices.

Sector Overview

In sector-specific ETFs, the materials and industrials sectors led the gains. VanEck Rare Earth & Strategic Metals ETF (REMX) surged 11.41%, benefiting from strong demand for rare earth elements, which are critical to the tech and defense industries. Similarly, the KraneShares Electric Vehicles and Future Mobility ETF (KARS) jumped by 10.91%, as the electric vehicle sector continues to attract significant investor interest, particularly with advancements in battery technology and supportive policy measures.

On the losing side, the First Trust NASDAQ ABA Community Bank ETF (QABA) in the financial sector experienced a 5.34% drop, reflecting ongoing challenges for smaller banking institutions in the face of rising interest rates and tightening lending conditions. The VanEck Oil Services ETF (OIH) also declined by 5.16%, following the broader downturn in oil prices.

International Overview

International markets showcased a blend of winners and losers. In Asia, ETFs like iShares MSCI All Country Asia ex Japan ETF (AAXJ) rose by 7.72%, supported by strong growth in Asian technology and manufacturing sectors. South Korea's iShares MSCI South Korea ETF (EWY) also performed well, gaining 4.96%, driven by robust demand for semiconductor products and favorable economic data.

However, Latin American markets faced headwinds, with Brazil's ETFs underperforming. The VanEck Brazil Small-Cap ETF (BRF) fell by 1.89%, as political uncertainty and slower-than-expected economic growth dampened investor sentiment.

Market Volatility

The week’s market volatility story was largely positive, with most volatility indices reflecting a drop in expected fluctuations. The VIX (S&P 500 volatility index) decreased by 2.47%, signaling reduced fear in the market. The VXN (Nasdaq volatility index) dropped even further, down 4.37%, as tech stocks continued their bullish run. The small-cap RVX index exhibited a significant reduction, falling by 14.47%, indicating a strong confidence boost in the Russell 2000 stocks. However, the VXD (Dow Jones volatility index) rose slightly by 2.00%, suggesting some caution remains around blue-chip stocks despite overall market strength.

Summary

Overall, the week of September 23-27 witnessed a strong and broad-based rally across major U.S. indices, with the IWM (Russell 2000) leading gains among small-cap stocks. Declining volatility across most indices reflected growing investor confidence, although caution persisted around blue-chip stocks. The materials and industrials sectors were among the top performers, while the energy sector lagged due to falling oil prices. Globally, Asian markets outperformed, while Latin American equities struggled with economic and political uncertainties. As we head into the final quarter of the year, the markets seem poised for continued growth, albeit with some pockets of caution.