Introduction: A Stellar Year for Netflix (NASDAQ:NFLX) Stock

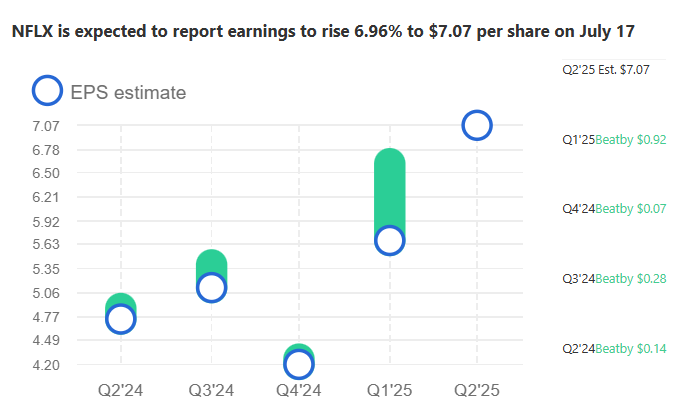

Netflix, Inc. (NASDAQ: NFLX) has delivered a remarkable performance in 2025, with its stock surging 91.64% year-to-date as of July 15, 2025. This meteoric rise, fueled by an average daily trading volume of approximately 4 million shares, underscores Netflix’s position as one of the top performers in the S&P 500. Investors and analysts alike are buzzing with anticipation as the company approaches its Q2 2025 earnings call on July 17, where it is expected to report earnings per share (EPS) of $7.07, a 6.96% increase from the prior quarter. This article explores the catalysts behind Netflix’s extraordinary growth, evaluates its potential for further upside, and examines correlated stocks, inverse ETFs, and the role of AI-driven trading tools in navigating this dynamic market. With a robust content pipeline, innovative monetization strategies, and strong financial fundamentals, Netflix’s trajectory offers a compelling case study for investors.

Financial Performance: A Foundation for Growth

Netflix’s financial performance in 2025 has been a cornerstone of its stock’s meteoric rise. In Q1 2025, the company reported revenue of $10.5 billion, a 13% year-over-year increase, and an EPS of $6.61, up 25% from the previous year. This momentum is expected to continue into Q2, with management forecasting revenue of $11.04 billion, reflecting a 15.4% year-over-year growth, and an EPS of $7.03, a 44.1% increase from Q2 2024. Wall Street analysts are slightly more optimistic, projecting Q2 revenue at $11.05 billion and EPS at $7.07. The company’s operating margin has also expanded significantly, reaching 32% in Q1 2025 (up from 28%) and projected to hit 33.3% in Q2. This margin expansion reflects Netflix’s ability to scale efficiently while managing costs, even as it invests heavily in content and advertising infrastructure.

The shift away from subscriber growth as the primary metric has refocused investor attention on traditional financial indicators such as revenue, profit margins, and free cash flow. Netflix’s Q1 2025 free cash flow was robust, and the company is on track to achieve its 2025 goal of $8 billion in free cash flow, bolstered by its capital-light advertising revenue stream. With a net debt-to-EBITDA ratio below 1.0 and $9.5 billion in cash reserves against $15.5 billion in total debt, Netflix has moved past its cash-burning days, providing a strong financial cushion for future investments. These metrics highlight Netflix’s operational efficiency and financial discipline, key drivers of its 91.64% stock surge.

Content Momentum: Fueling Subscriber and Revenue Growth

Netflix’s content strategy has been a pivotal driver of its 2025 performance. The company’s robust slate, including highly anticipated releases like Squid Game 3, Wednesday, and Stranger Things in the second half of 2025, has bolstered user engagement and viewership. The success of Squid Game 3 has been particularly notable, with BMO Capital raising its price target for Netflix from $1,200 to $1,425, citing impressive viewership numbers and favorable foreign exchange conditions. Additionally, Netflix’s expansion into live sports, including exclusive streaming rights for NFL games, has broadened its appeal and attracted new audiences. This strategic pivot toward premium and live content has strengthened Netflix’s position in the competitive streaming landscape.

The company’s ad-supported tier, launched in 2022, has also gained significant traction. By early 2025, the ad-supported plan reached 94 million monthly active users globally, up from 40 million the previous year. Netflix projects global ad sales to grow from $2.15 billion to $9 billion, a substantial increase that underscores the scalability of this revenue stream. The introduction of Netflix’s proprietary ad tech platform, Netflix AdsSuite, has enhanced user experience through personalized ads with low ad loads, further driving engagement. These content and advertising initiatives have not only fueled revenue growth but also reinforced investor confidence in Netflix’s long-term prospects.

Valuation Concerns: A Double-Edged Sword

Despite its impressive performance, Netflix’s valuation has sparked debate among analysts. Trading at a forward price-to-earnings (P/E) ratio of 49.35x, the stock is considered expensive, particularly given projected earnings growth of 28% in 2025 and 21.9% in 2026. Morningstar assigns Netflix a 1-star rating, suggesting the stock is significantly overvalued compared to its long-term fair value estimate of $750, which implies a P/E multiple of 29 times 2025 earnings. Loop Capital, while raising its price target to $1,150, maintains a Hold rating due to valuation concerns, noting that the stock’s 50x earnings multiple reflects much of its expected growth.

However, bullish analysts argue that Netflix’s premium valuation is justified by its dominant market position and growth potential. Wedbush’s Alicia Reese, for instance, reiterated a Buy rating with a $1,400 price target, citing the ad tier’s momentum and Netflix’s pricing power. Needham raised its price target to $1,500, emphasizing Netflix’s superior labor productivity and returns-driven model compared to peers like Apple (NASDAQ:AAPL) and Meta (NASDAQ:META). The consensus among analysts, with 15 Buy ratings and only one Sell rating, leans toward optimism, with an average price target of $1,314.48, implying a 4.3% upside from current levels. This dichotomy underscores the challenge of balancing Netflix’s strong fundamentals against its lofty valuation.

Correlated Stocks: Tracking Parallel Movements

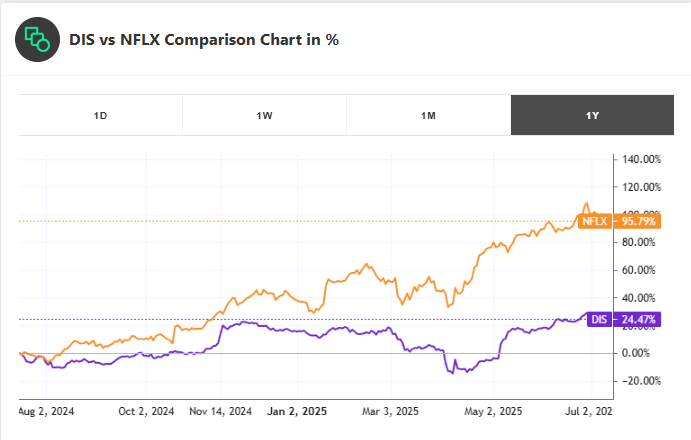

Netflix’s stock performance is closely correlated with other growth-oriented technology and media companies, particularly those in the streaming and entertainment sectors. One highly correlated stock is The Walt Disney Company (NYSE:DIS), which operates Disney+ and Hulu, direct competitors to Netflix. Over the past three years, NFLX and DIS have exhibited a correlation coefficient of approximately 0.75, reflecting similar market dynamics driven by streaming subscriber trends and content investments. Disney’s stock has also benefited from its pivot toward profitability in its streaming segment, with analysts forecasting a 12% revenue increase for Disney’s fiscal Q3 2025. Both companies are capitalizing on ad-supported tiers and premium content, making DIS a useful benchmark for investors tracking Netflix’s performance. Monitoring DIS alongside NFLX can provide insights into sector-wide trends and potential market shifts.

Inverse ETF Anticorrelation: Hedging with SCC

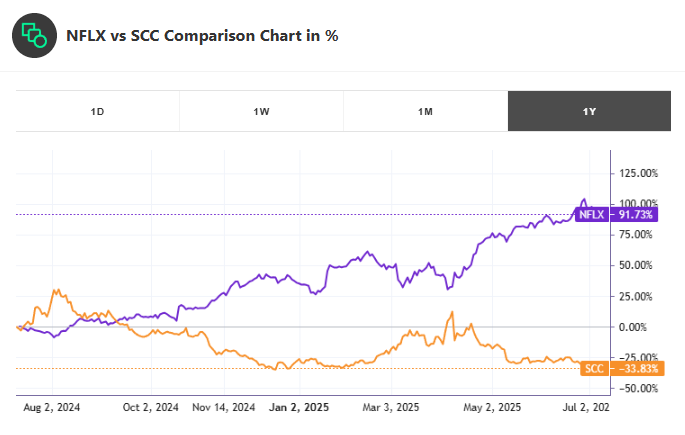

For investors seeking to hedge against potential volatility in Netflix’s stock, the ProShares UltraShort Consumer Services ETF (SCC) offers a compelling option due to its high anticorrelation with consumer discretionary stocks like Netflix. SCC exhibits a correlation coefficient of -0.87 with consumer discretionary names such as Levi Strauss & Co. (NYSE:LEVI), which shares similar market sensitivities to NFLX. This inverse ETF is designed to deliver twice the inverse daily performance of the Dow Jones U.S. Consumer Services Index, which includes media and entertainment companies. By incorporating SCC into a portfolio, investors can mitigate downside risk from a potential post-earnings pullback in NFLX, especially given concerns about its high valuation. AI Screener highlights SCC as a top choice for traders seeking inverse exposure to consumer discretionary volatility, offering a strategic hedge in turbulent markets.

Market News Impacting NFLX: July 15, 2025

The broader market environment on July 15, 2025, provides critical context for Netflix’s performance. The Q2 earnings season is in full swing, with major financial institutions like BlackRock (NYSE:BLK) and Bank of New York Mellon (NYSE:BK) reporting results, signaling robust corporate earnings despite modest S&P 500 EPS growth projections of 4.8%. However, the Energy sector faces challenges, with earnings expected to decline by 13.3% due to negative revisions, potentially creating a mixed market backdrop. Netflix’s stock has faced selling pressure recently, dropping below its ascending channel pattern, with key support levels at $1,200, $1,110, and $1,065, and resistance near $1,340. Investors are closely monitoring macroeconomic indicators, including U.S. GDP contraction and job growth, which could influence consumer spending and Netflix’s subscription revenue. These market dynamics underscore the importance of Netflix’s Q2 earnings in shaping investor sentiment.

AI-Powered Trading Tools

Has emerged as a leader in AI-driven trading solutions, offering a suite of tools that empower investors to navigate complex markets like Netflix’s. The company’s Financial Learning Models (FLMs) analyze vast datasets, including price action, volume, and news sentiment, to deliver real-time insights and predictive analytics. AI Trend Prediction Engine identifies market trends, while the AI Patterns Search Engine and AI Real-Time Patterns detect actionable trading signals. The AI Screener and Time Machine features allow users to filter stocks and backtest strategies, optimizing portfolio performance. Additionally, Daily Buy/Sell Signals provide clear, data-driven recommendations, enhancing decision-making for both retail and institutional traders. These tools are accessible at real-time trading strategies detailed at Virtual Agents and Signals.

AI Trading Agents: Revolutionizing NFLX Trades

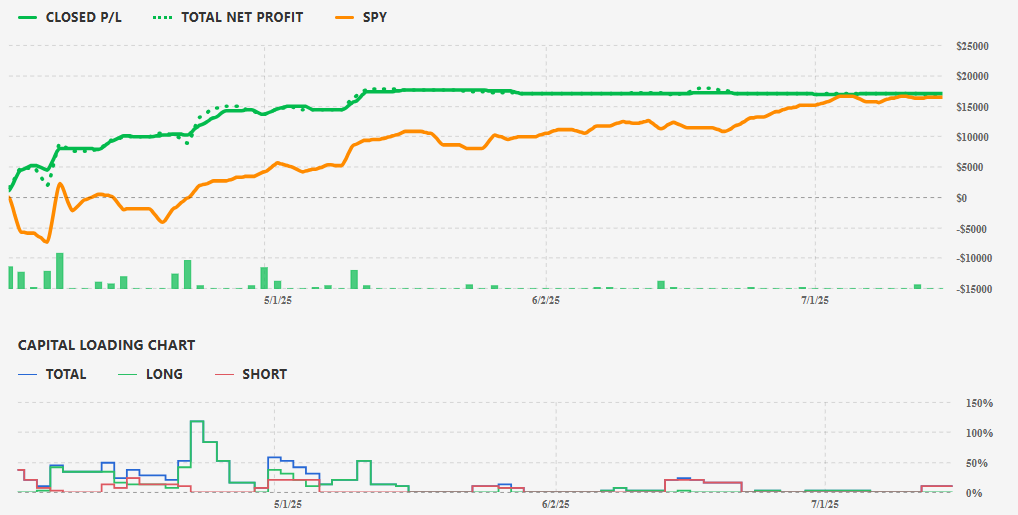

The latest innovation, its 15-minute and 5-minute AI Trading Agents, has transformed trading strategies for stocks like Netflix and inverse ETFs like SCC. Built on enhanced Financial Learning Models (FLMs), these agents process market data at shorter time frames, enabling faster responses to intraday price movements. Backtests show these models outperform traditional 60-minute strategies by 15%, offering precise entry and exit signals. For NFLX, which exhibits high volatility around earnings, these agents can capitalize on rapid price swings, while SCC traders benefit from inverse exposure during downturns. Double Agent Bot, leveraging real-time intraday signals, posted a 9.77% quarterly gain while the S&P 500 dropped 9.28%, demonstrating the power of AI-driven trading. Explore these capabilities at Real Money Trading and follow updates on the X account.

Growth Catalysts: Advertising and Global Expansion

Netflix’s strategic focus on its ad-supported tier and global expansion has significantly contributed to its 2025 stock surge. The ad tier’s 94 million monthly active users reflect a 135% year-over-year increase, driven by competitive pricing and enhanced ad tech. Analysts project ad revenue to double in 2025, supporting Netflix’s goal of tripling operating income to $30 billion and expanding its subscriber base to 410 million by 2027. Price hikes in key markets, coupled with strong average revenue per user, have further bolstered financial performance. Geographically, Netflix’s revenue from Europe, the Middle East, and Africa is expected to reach $3.47 billion in Q2, up 15.3% year-over-year. These initiatives highlight Netflix’s ability to diversify revenue streams and sustain growth in a competitive landscape.

Risks and Challenges: Navigating Economic Uncertainty

Despite its strong performance, Netflix faces risks that could impact its growth trajectory. Economic uncertainty, including U.S. GDP contraction and potential consumer spending cutbacks, may pressure subscription revenue. Additionally, increased content production costs and marketing expenses in the second half of 2025 could compress margins, with management guiding full-year operating margins at 29% compared to Q2’s 33%. The stock’s high valuation also raises the risk of a post-earnings pullback if results fall short of expectations, as noted by some X users expressing anxiety over potential misses. Investors must weigh these risks against Netflix’s robust fundamentals and long-term growth prospects.

Technical Analysis: Support and Resistance Levels

From a technical perspective, Netflix’s stock has recently broken below its ascending channel pattern, signaling potential near-term consolidation. Key support levels to watch include $1,200, $1,110, and $1,065, while resistance lies near $1,340. The stock’s relative strength index (RSI) is approaching overbought territory at 68, suggesting caution for short-term traders. However, the 50-day moving average, currently at $1,150, provides a strong support base, aligning with Loop Capital’s revised price target. For traders using Tickeron’s AI tools, real-time pattern recognition can help identify optimal entry points, particularly around earnings-driven volatility. Visit Tickeron.com for advanced technical analysis tools.

Analyst Sentiment and Earnings Outlook

Analyst sentiment remains predominantly bullish, with 15 Buy ratings and a consensus price target of $1,314.48. Citigroup’s Jason Bazinet expects Netflix to exceed Q2 revenue and EBIT estimates, driven by foreign exchange tailwinds. Goldman Sachs’ Eric Sheridan forecasts a 3-5% revenue beat, citing strong content performance. However, valuation concerns persist, with some analysts downgrading NFLX to Neutral due to its high P/E multiple. The Zacks Earnings ESP of +2.84% and Netflix’s history of beating estimates (e.g., a 16.17% surprise in Q1 2025) suggest a potential earnings beat on July 17. This optimism is tempered by the need for Netflix to deliver on its ambitious full-year guidance, including $45 billion in revenue and $9 billion in free cash flow.

Long-Term Prospects: A Streaming Powerhouse

Netflix’s long-term outlook remains compelling, driven by its dominant market position, innovative monetization strategies, and global reach. The company’s ability to generate $9 billion in free cash flow while funding $18 billion in content costs underscores its financial resilience. Strategic initiatives like live sports streaming and ad tech investments position Netflix to capture a growing share of the global entertainment market. Analysts like Alicia Reese from Wedbush believe Netflix’s contribution margin could surpass estimates, driving outsized free cash flow. With a projected subscriber base of 410 million by 2027, Netflix is well-positioned for sustained growth, despite near-term valuation challenges.

Conclusion: Balancing Opportunity and Caution

Netflix’s 91.64% stock surge in 2025 reflects its strong financial performance, innovative content strategy, and successful pivot to advertising revenue. As the company approaches its Q2 earnings on July 17, expectations for a 6.96% EPS increase and 15.4% revenue growth signal continued momentum. However, its high valuation and economic uncertainties warrant caution. Investors can leverage correlated stocks like DIS for sector insights and hedge with inverse ETFs like SCC to manage volatility. Tickeron’s AI-driven tools, including its 15-minute and 5-minute Trading Agents, offer a powerful edge in navigating NFLX’s price movements.