Key Points

Record-Breaking Momentum: US equity indices achieved multiple all-time highs, with the S&P 500 (SPY) closing at a record 6,279.36 and the Nasdaq Composite (QQQ) hitting 20,601.10. The tech-heavy index delivered an extraordinary 33% gain from its April low.

Dollar's Historic Decline: The US Dollar Index (DXY) experienced its worst first-half performance since 1973, plummeting nearly 11%[3] to three-year lows around 96.60, creating significant opportunities for investors in foreign currencies and international assets.

Bitcoin's Quarterly Triumph: Bitcoin (BTC.X) soared 32% during Q2, trading at $109,000 and positioned just 3% below its all-time high of $111,000, demonstrating remarkable resilience and institutional adoption.

Meta's AI Revolution: Meta (META) reached an all-time high of $738.09, driven by the announcement of "Meta Superintelligence Labs" and a $14.3 billion investment in Scale AI, positioning the company at the forefront of artificial intelligence development.

Robust Employment Data: The June nonfarm payrolls report exceeded expectations with 147,000 jobs added, compared to forecasts of 110,000, while unemployment declined to 4.1% from 4.2%, signaling continued labor market strength.

Overview

The shortened week of June 30 - July 4, 2025, marked a pivotal moment in global financial markets as investors witnessed historic achievements across major asset classes. The period was characterized by unprecedented record highs in US equities, a dramatic weakening of the US dollar to levels not seen since the early 1970s, and a remarkable surge in cryptocurrency valuations. This confluence of factors created a dynamic trading environment where traditional safe-haven assets were challenged, and risk appetite reached extraordinary levels despite ongoing geopolitical uncertainties and trade tensions.

Financial Markets Weekly Recap

Equities

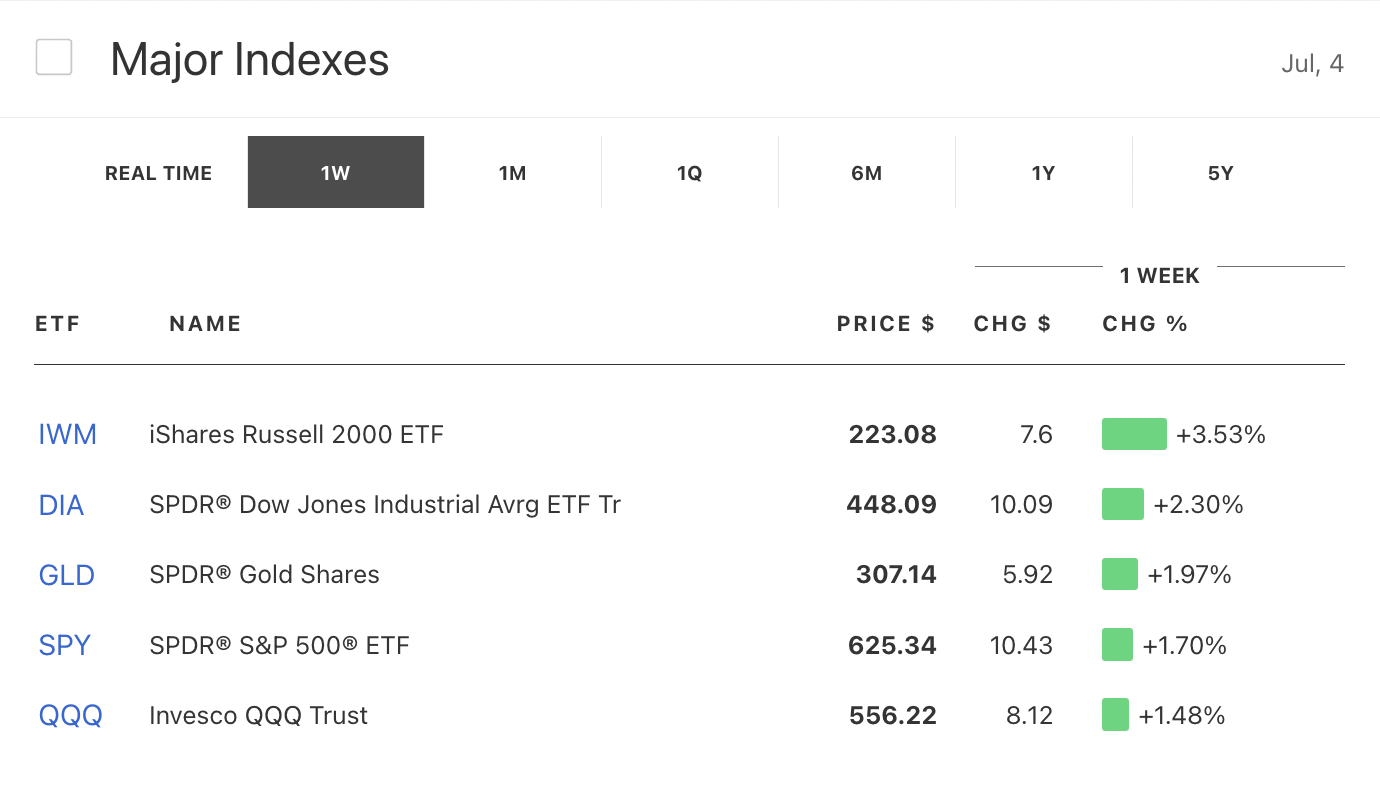

Index Performance: The equity markets delivered spectacular performance during this shortened holiday week. The S&P 500 (SPY) achieved a record closing high of 6,279.36, representing a valuation near $53 trillion. Futures opened Monday with approximately 0.5% gains, extending the momentum from Friday's record finish. The Nasdaq Composite (QQQ) demonstrated even more impressive performance, logging a historic 33% increase from its April lows to reach 20,601.10, with over $10 trillion in net new money flowing into the tech-heavy index.

Corporate Highlights:

Meta (META) achieved unprecedented success, reaching an all-time high of $738.09 with an intraday peak of $747.90. The stock demonstrated exceptional year-to-date performance with 23% gains, outperforming all Magnificent Seven peers. The surge was catalyzed by CEO Mark Zuckerberg's announcement of "Meta Superintelligence Labs" (MSL), a new division combining foundation model teams including the open-source Llama project. The company's $14.3 billion investment in Scale AI and recruitment of Scale's CEO Alexandr Wang demonstrated its commitment to AI leadership.

Tesla (TSLA) faced challenges with Q2 2025 deliveries declining 14% year-over-year to 384,122 vehicles. Despite production remaining relatively stable at 410,244 vehicles, the delivery shortfall highlighted ongoing demand pressures. The Model 3/Y segment delivered 373,728 units, while "Other Models" including Cybertruck, Model S, and Model X saw deliveries drop to 10,394 units, representing a 52% decline compared to the previous year.

Currencies

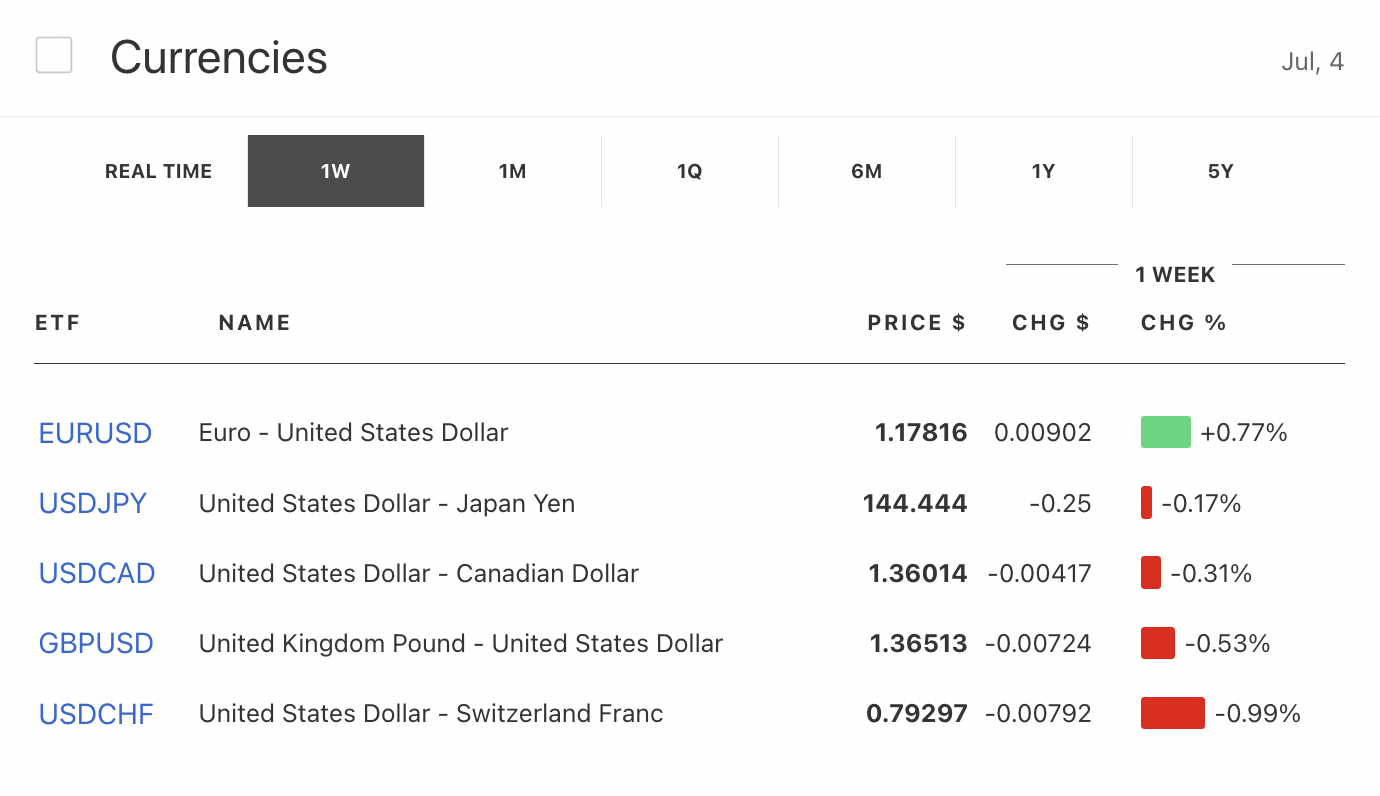

US Dollar Collapse: The most significant development was the US Dollar's historic decline, with the DXY experiencing its worst first-half performance since 1973. The index plummeted nearly 11% to languish near three-year lows of 96.60, territory last seen in March 2022. This dramatic reversal reflected mounting concerns about Trump's inconsistent tariff policies, Washington's expanding fiscal deficits, and perceived threats to Federal Reserve independence.

EUR/USD Surge: The euro emerged as a primary beneficiary of dollar weakness, climbing toward $1.18 - levels not witnessed since September 2021. The pair demonstrated remarkable strength with year-to-date gains exceeding 13%. However, technical analysis suggested potential fatigue after eight consecutive green days, with the pair showing consolidation signs around $1.17 as traders questioned sustainability at these elevated levels.

GBP/USD Performance: Sterling continued its impressive run, achieving its best half-year performance since 2009. The pair reached highs of 1.3789 on July 1, benefiting from both dollar weakness and relative UK economic resilience. British Pound strength was supported by persistent inflation concerns that reduced Bank of England rate cut expectations.

USD/JPY Dynamics: The yen strengthened significantly as Japan's July 9 tariff deadline approached. President Trump's refusal to extend trade negotiations and threats of 30-35% tariffs on Japanese imports created substantial uncertainty. The pair faced additional pressure from speculation about potential Bank of Japan policy shifts.

Commodities

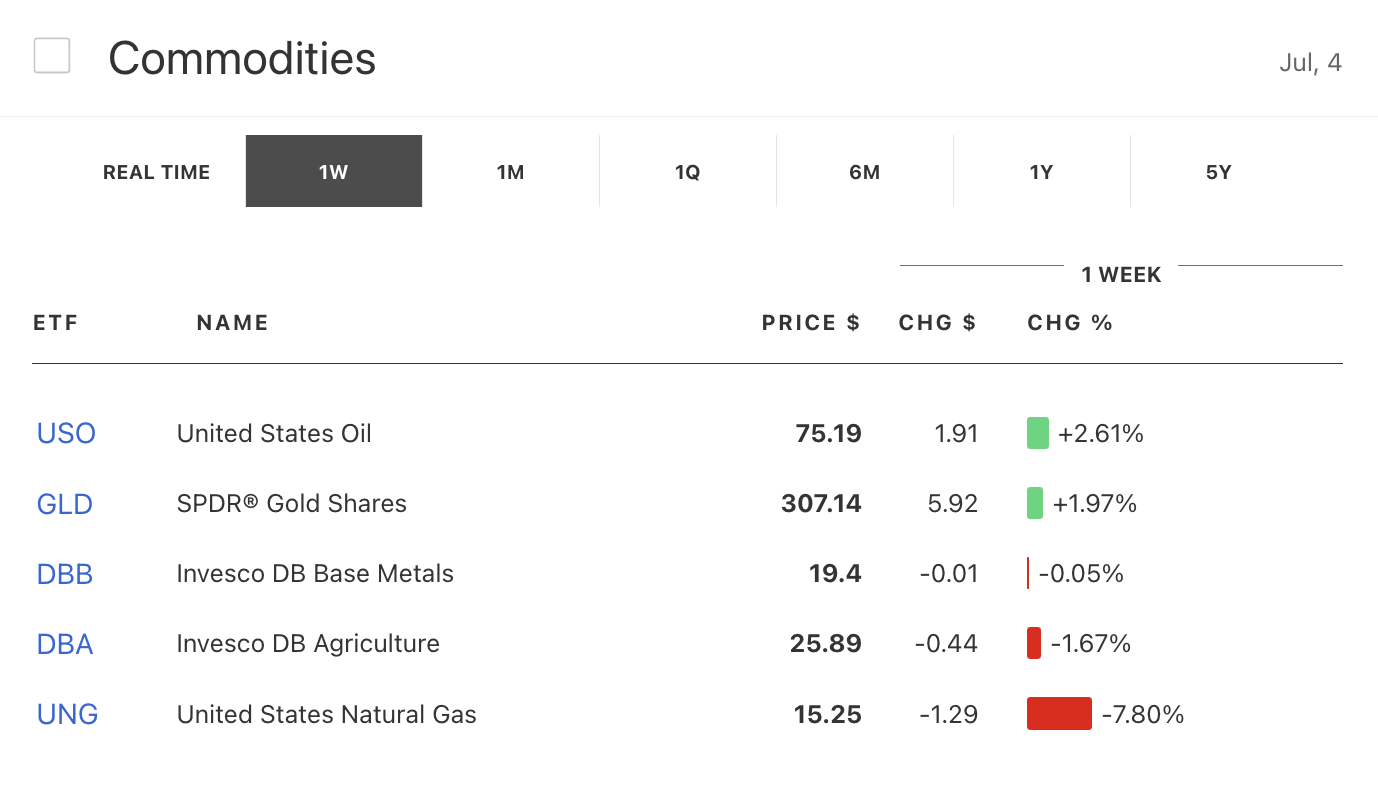

Gold Rally: Gold prices experienced substantial gains, reaching levels above $3,360 during a two-day rally. The precious metal benefited from the dramatic dollar weakness and safe-haven demand amid trade tensions. Gold's 2025 performance has been exceptional, with prices soaring over 25% year-to-date and setting records above $3,500 per ounce in April. Central bank accumulation, particularly from China's People's Bank, continued to provide structural support.

Cryptocurrencies

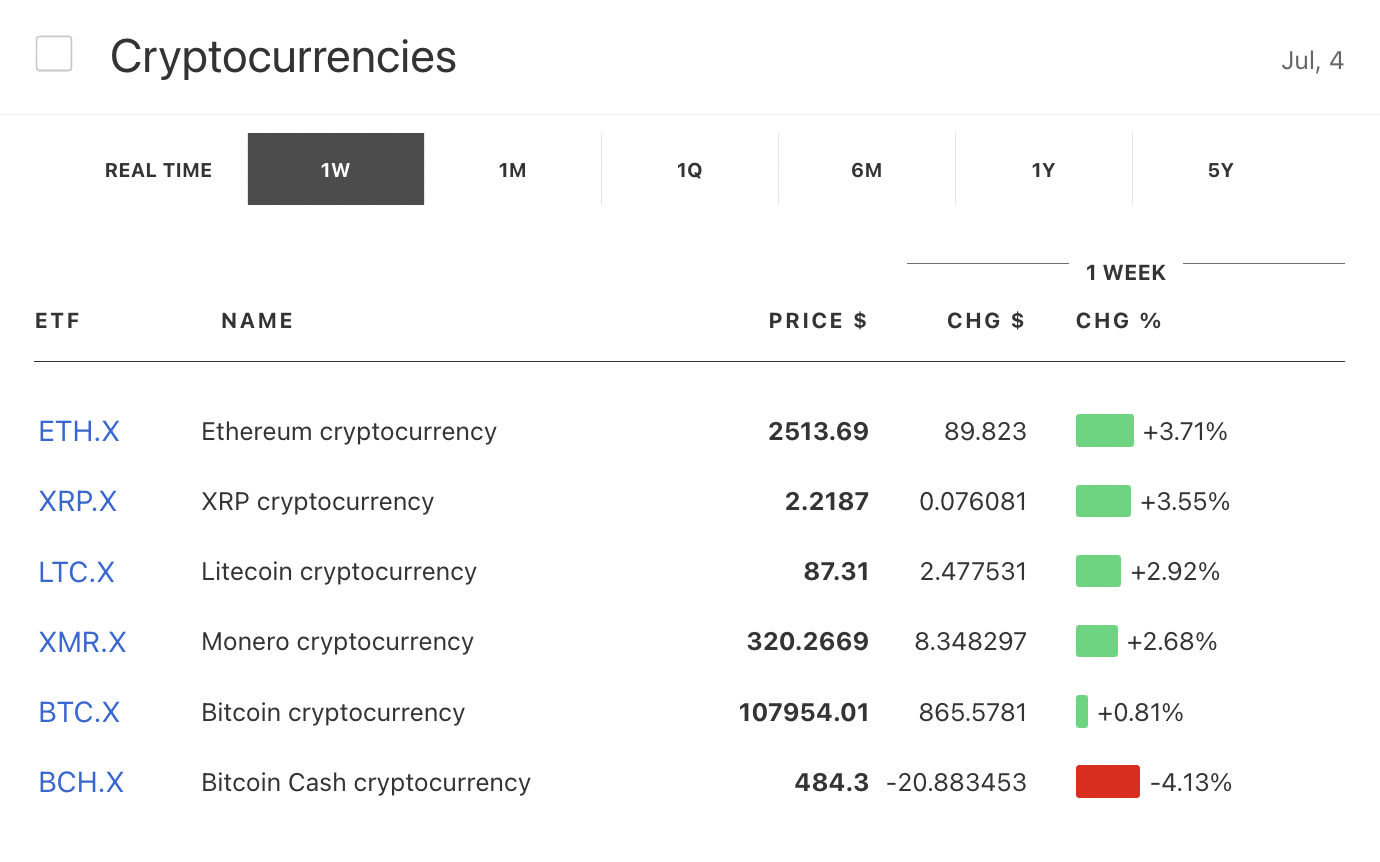

Bitcoin's Momentum: Bitcoin (BTC.X) delivered outstanding Q2 performance with 32% gains, ending the quarter at approximately $109,000. The cryptocurrency positioned itself just 3% below its all-time high of $111,000, completing three consecutive months of positive returns. Institutional adoption and correlation with risk assets supported the rally, while technical traders focused on resistance levels around $111,000.

Ethereum Consolidation: Ether (ETH.X) faced more challenging conditions, losing 25% during the first half of 2025 while trading near $2,500. The second-largest cryptocurrency underperformed Bitcoin significantly, with prices consolidating in a range between $2,375 and $2,520. Despite institutional inflows into spot Ethereum ETFs totaling $1.17 billion in June, the token struggled to match Bitcoin's momentum.

Economic Indicators and Policy Developments

Employment Strength: The June nonfarm payrolls report provided crucial insights into labor market resilience. Employment increased by 147,000 jobs, substantially exceeding consensus expectations of 110,000. The unemployment rate declined to 4.1% from 4.2%, while average hourly earnings growth moderated to 3.7% year-over-year, suggesting cooling wage inflation pressures.

Federal Reserve Outlook: Market expectations increasingly pointed toward a September rate cut rather than action at the July 29-30 meeting. Fed Chair Jay Powell's scheduled Tuesday commentary was anticipated to provide additional clarity on monetary policy direction. The combination of solid employment growth and moderating wage inflation created a complex environment for Fed decision-making.

Trade Policy Tensions: The approaching July 9 deadline for trade negotiations created significant market uncertainty. President Trump's refusal to extend the deadline and threats of substantial tariffs on Japan highlighted the administration's aggressive trade stance. The suspension of country-specific reciprocal tariffs was set to expire, potentially reactivating rates ranging from 11% to 50% across various trading partners.

Geopolitical Developments

US-Japan Trade Tensions: The most significant development involved escalating tensions between the United States and Japan. President Trump expressed skepticism about reaching a trade agreement, threatening tariffs of "30, 35 or whatever number we decide" on Japanese imports. This represented a substantial increase from the previously suspended 24% rate, creating uncertainty for one of America's largest trading partners.

Canadian Relations: Canada's decision to scrap its digital services tax on tech giants like Meta (META) and Google (GOOGL) represented an attempt to improve US relations. However, President Trump's Friday threat to impose new tariffs on Canada within a week demonstrated the administration's confrontational approach to trade policy.

Market Outlook

As markets transition into the second half of 2025, several critical factors will shape performance:

Monetary Policy Evolution: The Federal Reserve's September meeting assumes greater importance as markets price in potential rate cuts. The combination of robust employment data and moderating inflation creates a complex backdrop for policy decisions. Powell's upcoming testimony and economic data releases will be closely scrutinized for directional guidance.

Trade Policy Resolution: The July 9 deadline for trade negotiations represents a crucial inflection point. The potential reactivation of reciprocal tariffs could significantly impact global trade flows and currency valuations. Japan's response to US demands and the broader implications for international trade relationships remain key uncertainties.

Dollar Trajectory: The historic dollar decline creates opportunities and challenges across global markets. Continued weakness could benefit emerging markets and commodities while potentially complicating Federal Reserve policy decisions. The sustainability of current levels depends heavily on trade policy developments and relative economic performance.

Technology Sector Momentum: The exceptional performance of technology stocks, led by companies like Meta (META) with its AI investments, suggests continued investor appetite for growth and innovation. The sector's ability to maintain momentum depends on successful execution of AI strategies and sustained earnings growth.

Cryptocurrency Evolution: Bitcoin's proximity to record highs and institutional adoption trends suggest potential for further gains. However, regulatory developments and macroeconomic conditions will continue to influence cryptocurrency valuations. Ethereum's relative underperformance presents both challenges and opportunities for the broader digital asset ecosystem.

The week's events established a foundation for significant market developments in the third quarter, with policy decisions, trade negotiations, and corporate earnings likely to drive substantial volatility across asset classes. Investors should prepare for continued uncertainty while positioning for potential opportunities arising from historic currency realignments and shifting monetary policy expectations.