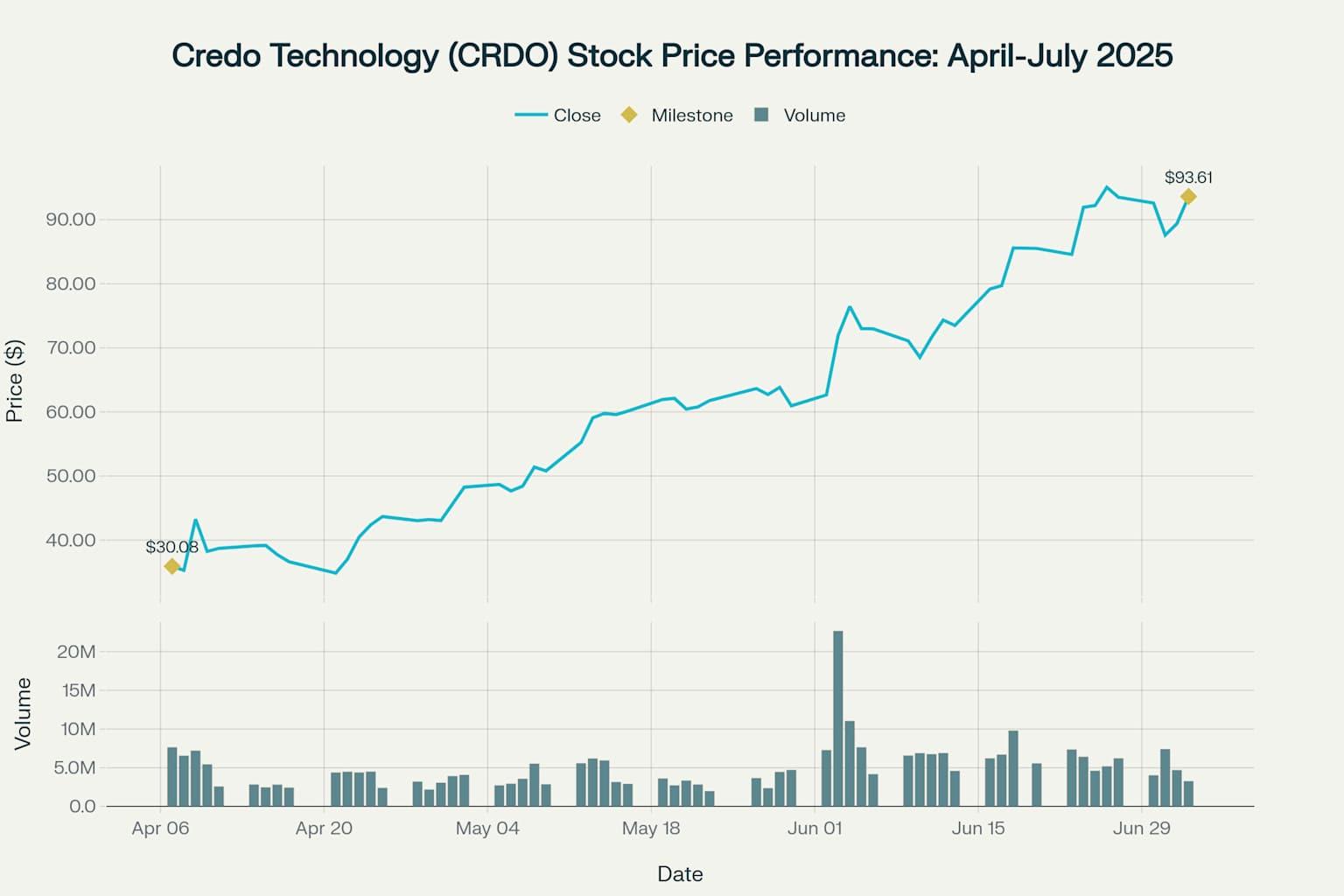

Credo Technology Group Holding Ltd (CRDO) has delivered one of the most spectacular stock performances in the semiconductor sector during the spring and summer of 2025, with shares surging an extraordinary 221% from the April 7 low of $30.08 to the July 3 close of $93.61. This remarkable rally has positioned CRDO at all-time highs, transforming what was once a relatively unknown connectivity solutions provider into a Wall Street darling riding the artificial intelligence infrastructure boom.

Credo Technology (CRDO) stock price performance from April to July 2025, showing the remarkable 221% surge from the April 7 low of $30.08 to the July 3 close of $93.61, driven by strong earnings results and AI infrastructure demand.

Understanding Credo Technology: The Unsung Hero of AI Infrastructure

What Credo Does: Connecting the AI Ecosystem

Credo Technology operates at the critical intersection of hardware and connectivity in the rapidly expanding AI infrastructure market. The San Jose-based company specializes in developing high-speed connectivity solutions that serve as the "connective tissue" for AI servers, data centers, and hyperscale computing environments.

The company's core mission centers on delivering breakthrough solutions that enable the next generation of AI-driven applications. Credo's product portfolio encompasses three main categories:

The AI Infrastructure Imperative

Credo's solutions address a fundamental challenge in AI infrastructure: as AI models grow exponentially in size and complexity, the demand for high-speed, low-latency data transfer between GPUs, CPUs, and storage systems has become critical. The company's technologies enable multiple physical devices to work on the same AI model at high speed and low latency, making them essential for the massive AI clusters deployed by hyperscale data centers.

The scale of this opportunity is staggering. Hyperscale customers are pursuing AI/ML infrastructure that requires back-end scale-out interconnectivity densities that are an order of magnitude higher than their general compute infrastructure. Scale-up networks have grown from 8 GPUs to rack scale of 72 GPUs in 2024, with plans to expand even further.

The Earnings Catalyst: Record-Breaking Q4 2025 Results

Exceptional Financial Performance

The primary catalyst behind CRDO's meteoric rise was the company's "impressive" beat-and-raise earnings report released on June 2, 2025. The results exceeded expectations across virtually every metric:

The stock surged over 18% in after-hours trading immediately following the earnings announcement, with shares jumping approximately 15% in pre-market trading the following day.

Guidance Drives Continued Optimism

Perhaps more importantly than the strong Q4 results was Credo's bullish forward guidance. For Q1 fiscal 2026, the company projected revenue between $185-195 million, representing a remarkable 218% year-over-year increase at the midpoint and significantly exceeding analyst expectations of $163 million.

The company's fiscal 2026 revenue guidance of over $800 million represents more than 85% year-over-year growth, with management targeting a non-GAAP net margin approaching 40%.

Key Growth Drivers Behind the Surge

1. Explosive Demand for Active Electrical Cables

Credo's Active Electrical Cables (AECs) have emerged as a standout growth driver, with the product line posting double-digit sequential growth in Q4 2025. AECs offer several compelling advantages over traditional solutions:

The company's flagship HiWire AECs integrate retimer, gearbox, and forward error correction functionality into smaller gauge copper cables, providing a high-performance alternative to short, thick DACs and high-power, high-cost AOCs.

2. Hyperscaler Customer Momentum

Credo has established relationships with all major hyperscalers, including Microsoft, Amazon, and other leading cloud infrastructure providers. The company's Q4 results were driven by significant increases in volume of unit shipments of AEC products to hyperscaler customers, which contributed over 95% of the product sales revenue increase.

In Q4 2025, each of the company's top three customers contributed more than 10% to revenues. Management expects three to four customers to exceed 10% of revenues in upcoming quarters, driven by increasing volumes from existing hyperscalers and the expected ramp-up of two new hyperscale customers in the second half of fiscal 2026.

3. Optical DSP Business Expansion

Momentum in Credo's optical business, particularly for Optical Digital Signal Processors (DSPs), has been a key growth engine. The company achieved revenue targets for this business in fiscal 2025 and expects expansion of customer diversity across lane rates, port speeds and applications to accelerate revenue growth.

In April 2025, Credo unveiled its new Lark family of ultra-low power 800G optical DSPs, designed specifically for the challenging power and cooling requirements of the world's largest AI data centers. The Lark 850 is optimized for 800G Linear Receive Optics (LRO) with power consumption under 10W.

4. PCIe Solutions for AI Scale-Out Networks

Credo is expanding its addressable market through PCIe solutions designed for AI scale-out and scale-up networks. The company's PCIe Gen6 retimers deliver 40dB reach and sub-7ns latency at 11W, allowing designers to extend PCIe traces while ensuring best-in-class system performance.

With demonstration of PCIe Gen6 AECs and increasing hyperscaler interest, this product line is expected to remain a growth engine going forward.

Competitive Advantages: The SerDes Technology Moat

Proprietary Technology Platform

Credo's competitive advantage stems from its foundational intellectual property in SerDes technology. The company's proprietary SerDes and DSP technologies enable it to achieve similar performance to leading competitors' products but at a lower cost and using more highly available legacy node (n-1 advantage).

This technology leadership provides several key benefits:

System-Level Approach

Unlike many competitors, Credo owns the entire stack of SerDes IP, Retimer ICs, system-level design, qualification and production. This integrated approach allows for faster innovation cycles and strong cost efficiency, giving the company a competitive edge in rapidly evolving markets.

Strategic Partnerships

Credo has established strategic partnerships with industry leaders, most notably its collaboration with Microsoft on HiWire Switch AEC and open-source implementation. This partnership helps realize Microsoft's vision for highly reliable network-managed dual-Top-of-Rack (ToR) architecture, providing Credo with validation and market credibility.

Financial Transformation: From Losses to Profitability

Dramatic Financial Turnaround

One of the most impressive aspects of Credo's recent performance has been its transition from losses to strong profitability. The company achieved several financial milestones in fiscal 2025:

Strong Balance Sheet

Credo maintains a robust financial position with $431.3 million in cash and short-term investments as of Q4 2025. The company generated $57.8 million in operating cash flow during Q4, with free cash flow of $54.2 million.

Analyst Sentiment: Wall Street Embraces the Story

Price Target Upgrades

The strong Q4 results triggered a wave of analyst upgrades and price target increases:

Consensus Outlook

Based on analyst coverage, CRDO maintains strong Wall Street support:

Market Context: The AI Infrastructure Boom

Hyperscaler Capital Expenditure Surge

Credo's growth is directly tied to the massive capital expenditure programs of hyperscale data center operators. Key customers are investing heavily in AI infrastructure:

Market Size and Growth

The data infrastructure market served by Credo is experiencing unprecedented growth driven by several factors:

Competitive Landscape: David vs. Goliath

Major Competitors

Credo competes against significantly larger semiconductor companies:

Competitive Positioning

Despite facing much larger competitors, Credo has carved out a strong niche through:

Risk Factors and Challenges

Customer Concentration Risk

Credo derives a significant portion of revenue from a limited number of large customers. Any reduction in demand from major hyperscalers could significantly impact financial results, as occurred in early 2023 when the company's largest customer reduced demand forecasts.

Intense Competition

The company faces competition from much larger players with greater resources and broader product portfolios. Maintaining technological leadership against well-funded competitors represents an ongoing challenge.

Valuation Concerns

With CRDO trading at a P/S ratio of 15.16 (nearly double the sector average), some analysts question whether the current valuation adequately reflects execution risks. The stock's dramatic run-up has created high expectations for continued growth.

Supply Chain and Manufacturing Risks

As a fabless semiconductor company, Credo relies on third-party manufacturers for production. Any disruptions to key suppliers or manufacturing partners could impact product availability and margins.

Future Outlook: Sustainable Growth or Overvaluation?

Management's Long-Term Vision

CEO Bill Brennan has outlined an ambitious growth trajectory, targeting fiscal 2026 revenue exceeding $800 million (85%+ growth) with non-GAAP net margins approaching 40%. Key growth drivers include:

Technology Roadmap

Credo continues investing heavily in R&D, spending $146 million in fiscal 2025 (33% of revenue). Key development areas include:

Market Opportunity

The total addressable market for high-speed connectivity solutions continues expanding as AI adoption accelerates. Key growth vectors include:

Investment Thesis: Riding the AI Infrastructure Wave

Bull Case

Credo represents a pure-play investment in the AI infrastructure buildout with several compelling attributes:

Bear Case

Several factors could challenge Credo's continued outperformance:

As companies like Credo Technology become critical enablers of the AI revolution, platforms like Tickeron are helping traders spot opportunities born from this transformative wave. Tickeron applies advanced machine learning to analyze market behavior and generate precise trade ideas across equities, ETFs, and crypto—helping traders act with confidence in fast-evolving tech sectors.

Whether you're tracking semiconductor breakouts or AI infrastructure leaders, Tickeron offers a streamlined set of tools to enhance short-term timing and long-term positioning.

Key features include:

In a market where technological breakthroughs can reshape entire industries overnight, Tickeron gives traders the analytical edge needed to stay agile and informed.

Conclusion: A Remarkable Transformation

Credo Technology's 221% stock surge from April to July 2025 reflects a fundamental transformation from a niche connectivity provider to a critical enabler of the AI revolution. The company's record-breaking financial results, strong customer relationships, and positioning in high-growth markets have created a compelling investment narrative that has captivated Wall Street.

However, with great success comes great expectations. Trading at premium valuations and facing intensifying competition from much larger players, Credo must continue executing flawlessly to justify current stock levels. The company's ability to maintain its technology leadership, expand its customer base, and scale operations will determine whether this remarkable rally represents the beginning of a long-term growth story or a spectacular but unsustainable surge.

For investors, Credo exemplifies both the tremendous opportunities and inherent risks of investing in the AI infrastructure theme. While the company's solutions are undeniably critical to the ongoing AI buildout, the stock's valuation requires continued exceptional execution in an increasingly competitive and rapidly evolving market. As CEO Bill Brennan noted, "We continue to see growing demand for our solutions across hyperscaler customers to power advanced AI services, a trend we believe will persist for the foreseeable future". The question for investors is whether Credo can maintain its technological edge and market position as this AI infrastructure boom continues to unfold.