The week of July 21-25, 2025, marked a pivotal period for global financial markets, characterized by record-breaking performances, significant earnings revelations, and evolving trade negotiations. Major indices reached unprecedented heights while investors carefully navigated through a complex landscape of corporate earnings, monetary policy expectations, and ongoing trade tensions.

Market Performance

Equity Markets Milestones

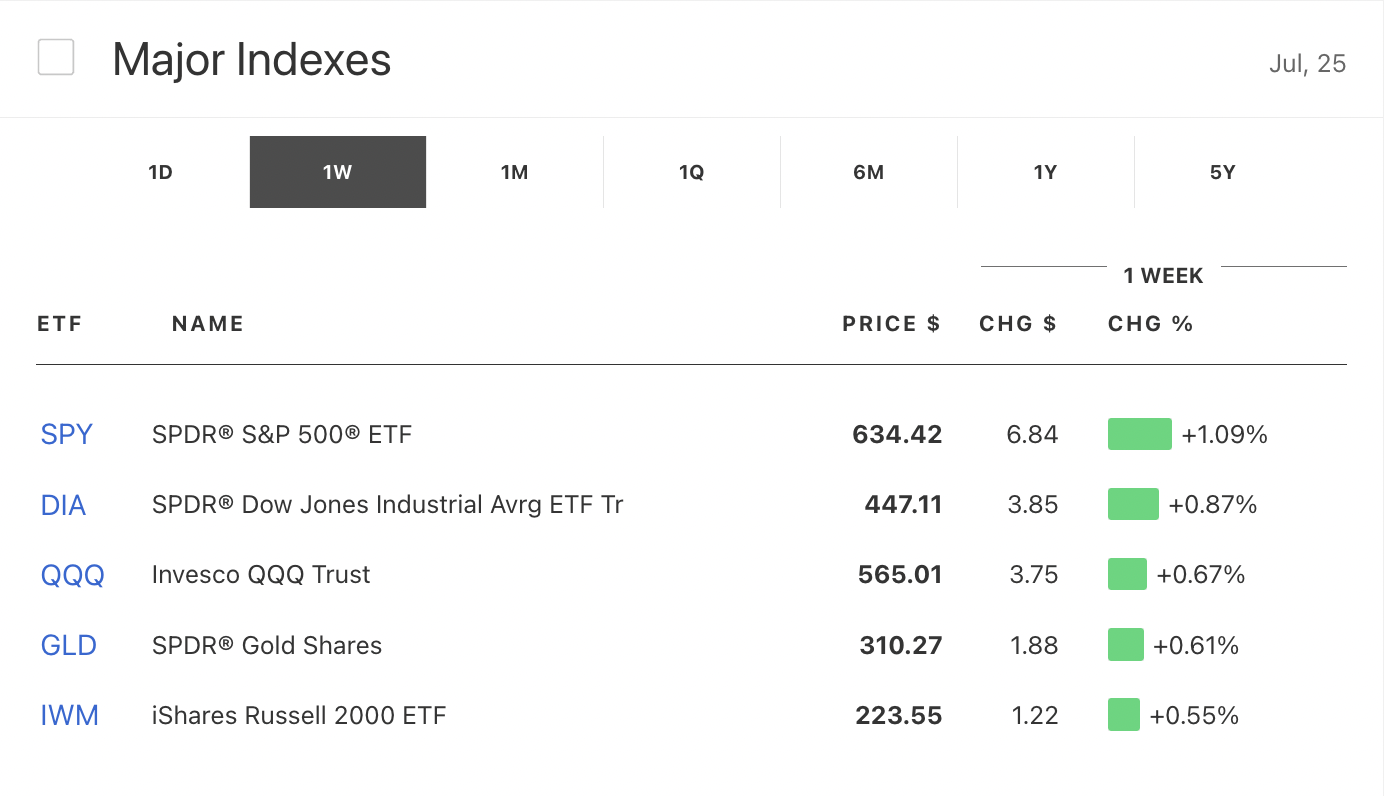

The week delivered remarkable achievements for U.S. equity markets, with multiple indices achieving record highs despite underlying uncertainties. The S&P 500 demonstrated exceptional strength, climbing to fresh record closes throughout the week and settling above 6,300 for the first time in history. On Wednesday alone, the index gained 0.78%, marking its 12th record closing of 2025. The index has now gained approximately 7% year-to-date.

The technology-heavy Nasdaq Composite matched this performance with its own series of records, surpassing the 21,000 mark for the first time and posting gains of nearly 9% for the year. Monday's session saw the Nasdaq rise 0.4% to 20,974.17, while Tuesday brought another 0.6% advance that pushed the index beyond 21,000.

The Dow Jones Industrial Average showed equally impressive momentum, surging 508 points (1.1%) on Wednesday to reach 45,010.29, coming within just four points of its all-time high. The 30-stock index needs only a modest four-point gain to establish a new record, highlighting the broad-based nature of the current rally.

Sector Performance and Market Dynamics

Technology stocks led the advance, with the "Magnificent Seven" companies playing a central role in driving market gains. Alphabet surged 2.7% ahead of its earnings announcement, while Amazon gained 1.2% and Apple rose 1%. This technology-driven rally reflects continued investor confidence in artificial intelligence capabilities and cloud computing growth.

The week also witnessed the resurgence of meme stock trading, exemplified by Opendoor Technologies's spectacular volatility. The real estate technology company soared as much as 120% intraday Monday before closing up 43%, driven by retail trading frenzy and options-driven gamma squeezes. The stock has tripled in value over the past week, demonstrating that retail investor enthusiasm remains a significant market force.

Corporate Earnings Season

Technology Giants Deliver Mixed Results

The earnings season's marquee events came from two Magnificent Seven companies, delivering contrasting results that highlighted both opportunities and challenges in the technology sector.

Alphabet Exceeds Expectations

Alphabet delivered a strong performance that exceeded both revenue and earnings expectations. The Google parent reported second-quarter revenue of $96.43 billion, surpassing the consensus estimate of $94 billion, representing 14% year-over-year growth. Earnings per share reached $2.31, beating the expected $2.18.

The company's diverse revenue streams all contributed to the strong performance. YouTube advertising revenue totaled $9.8 billion, above the $9.56 billion consensus, while Google Cloud generated $13.62 billion, also exceeding forecasts. However, the most significant development was management's decision to raise 2025 capital expenditures guidance to $85 billion, up from the previous $75 billion forecast. This $10 billion increase reflects CEO Sundar Pichai's confidence in "strong and growing demand" for Google Cloud and AI infrastructure.

Tesla Faces Headwinds

Tesla presented a more challenging picture, with second-quarter results highlighting the pressures facing the electric vehicle industry. The company reported revenue of $22.5 billion, falling short of the $22.64 billion consensus and representing a 12% decline from the previous year. Earnings per share of $0.40 met expectations, but automotive revenue plunged 16% to $16.7 billion.

The company's delivery challenges were evident, with Tesla selling 384,122 vehicles in Q2, approximately 60,000 fewer than the same period last year. CEO Elon Musk warned investors that the company "probably could have a few rough quarters," citing higher tariffs and expiring EV tax credits as significant headwinds. Regulatory credit sales, a key profit driver, fell sharply to $439 million from $890 million a year ago.

Additional Corporate Developments

Domino's Pizza Delivers Growth

Domino's Pizza provided a bright spot in the consumer sector, with shares jumping 6% to $490 following strong second-quarter results. Revenue climbed 4.3% year-over-year to $1.15 billion, driven by improving North American momentum and strong global demand. Same-store sales rose 3.4% in North America, a significant turnaround from the previous quarter's 0.5% decline. Despite missing earnings expectations with $3.81 per share versus the $3.95 consensus, investors focused on the revenue growth trajectory.

Intel Faces Transition Challenges

Intel demonstrated the challenges facing traditional technology companies amid rapid industry evolution. Despite beating revenue expectations with $12.9 billion versus the $11.97 billion consensus, the chipmaker posted a 10-cent per share loss, missing expectations for a modest profit. New CEO Lip-Bu Tan, just five months into his tenure, provided guidance for the current quarter of $12.6-$13.6 billion in revenue, above Wall Street's midpoint estimate. However, the stock declined 5% in premarket trading as investors remained cautious about the company's turnaround progress.

LVMH Luxury Concerns

LVMH highlighted challenges in the luxury goods sector, with the company posting its second consecutive quarter of sales missing estimates. The luxury powerhouse's performance reflects broader concerns about consumer spending patterns and global economic uncertainty affecting high-end retail markets.

Amazon Insider Activity

Amazon saw significant insider activity as founder Jeff Bezos sold 6.6 million shares worth approximately $1.5 billion. Despite this substantial sale, Bezos retains significant holdings in the e-commerce and cloud computing giant. The transaction had minimal impact on the stock price, demonstrating market confidence in the company's fundamentals.

Monetary Policy and Economic Environment

Federal Reserve Expectations

The Federal Reserve's upcoming July 30-31 policy meeting garnered significant attention, with markets widely expecting the central bank to maintain current interest rates. The federal funds rate has remained unchanged at 4.25%-4.50% for four consecutive meetings as policymakers await clearer inflation and economic activity signals. Federal Reserve data shows the effective federal funds rate at 4.33% throughout the week.

President Trump's continued criticism of Fed Chair Jerome Powell added political complexity to monetary policy discussions. However, Trump's Wednesday visit to the Federal Reserve headquarters resulted in more conciliatory comments, with the president stating he was not contemplating Powell's dismissal and expressing confidence that the chair would "make the right call" on interest rates.

Strong employment data released during the week reinforced expectations for unchanged policy. The jobs report highlighted 235,000 nonfarm payrolls added in June and a 3.7% unemployment rate, signaling labor market resilience and supporting the Fed's "higher for longer" approach. This data pushed Bitcoin to a seven-day low and reduced market expectations for rate cuts this year.

European Central Bank Maintains Stability

The European Central Bank delivered its expected decision to hold interest rates steady at Thursday's meeting. The deposit facility rate remained at 2.00%, while the main refinancing operations rate stayed at 2.15%. This pause marked the end of the ECB's current easing cycle after eight cuts over the past year.

The ECB's decision reflected balanced economic conditions, with inflation stabilizing at the 2% target while trade uncertainty and global tensions persist. Policymakers emphasized the economy's resilience, noting stronger-than-expected growth in early 2025, though firms remain cautious about investment due to tariff concerns and global uncertainty. The stronger euro has also made exports more expensive while improving import affordability.

Trade Negotiations and Geopolitical Developments

Progress in U.S. Trade Agreements

The week witnessed significant developments in international trade negotiations, with President Trump announcing new agreements that helped ease market concerns about escalating tariff wars. Trump secured trade deals with Japan, Indonesia, and the Philippines, signaling a more conciliatory approach ahead of the August 1 tariff deadline.

The Japan agreement proved particularly significant, with the U.S. and Japan reaching a compromise that reduced auto tariffs to 15% from the previously threatened 25%. The deal eliminated quotas on Japanese car imports while requiring Japan to open its markets more fully to American cars and rice. Trump characterized the agreement as "perhaps the largest Deal ever made," though markets viewed it as a successful de-escalation of trade tensions.

European Union Negotiations

EU-U.S. trade discussions remained complex, with European leaders meeting to develop responses to Trump's 30% blanket tariff threats. The Financial Times reported that the EU and U.S. were approaching a deal with similar terms to the Japan agreement, potentially establishing a 15% tariff instead of the previously threatened 25% or 30%. The EU maintained its suspension of retaliatory tariffs until August 1 while preparing additional countermeasures if negotiations fail.

Currency Market Implications

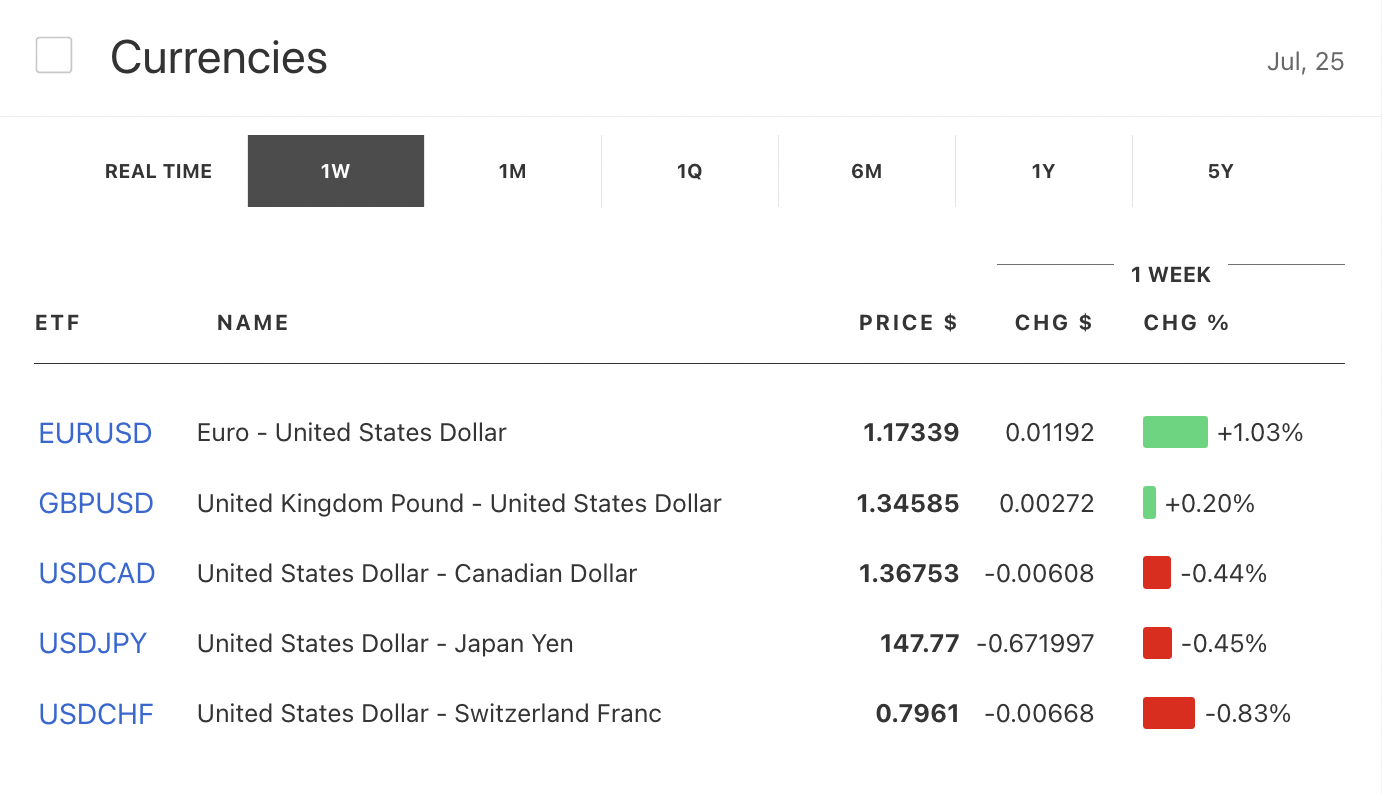

The EUR/USD pair reflected these trade developments, initially strengthening to $1.1650 as EU leaders prepared for high-stakes negotiations. However, the currency later stabilized near $1.1750 following the ECB's decision to pause rate cuts. The pair's movements demonstrated market sensitivity to both trade negotiations and monetary policy divergence between the U.S. and eurozone.

The USD/JPY pair traded near ¥147.00, initially declining on news of the Japan trade deal before recovering as broader dollar weakness emerged. The yen's performance reflected both the successful trade negotiations and ongoing monetary policy divergence between the Federal Reserve and Bank of Japan.

Commodities and Alternative Assets

Gold Market Dynamics

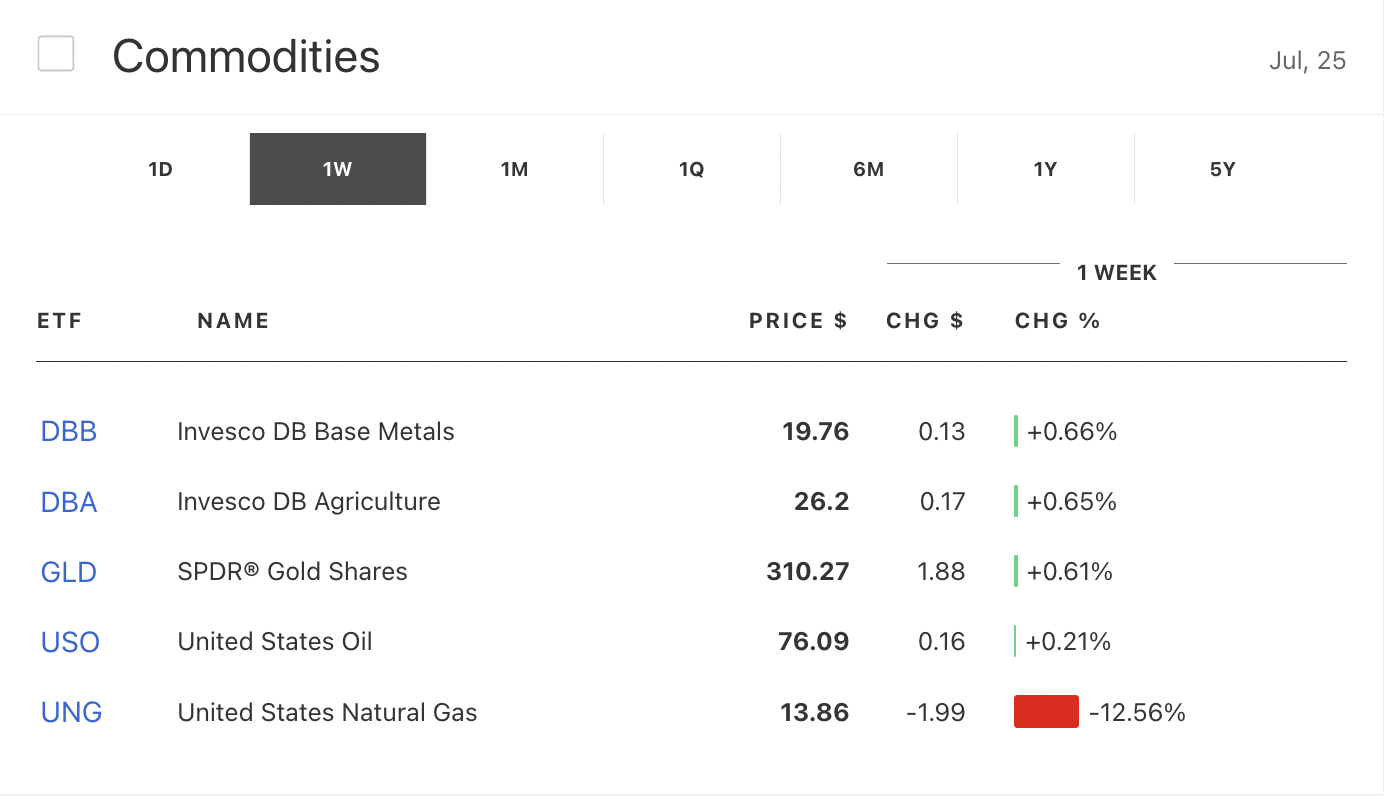

Gold prices experienced significant volatility, initially jumping to $3,402—its highest level in over a month—before paring gains to around $3,380 per ounce. The precious metal's strength reflected weaker dollar conditions, lower yields, and rising global tensions surrounding trade negotiations. However, as trade optimism increased and risk appetite returned, gold prices retreated in a steep three-day decline, hitting $3,350.

The gold market's performance highlighted its continued role as a safe-haven asset, with traders closely monitoring the August 1 tariff deadline and its potential impact on global economic stability. Federal Reserve Chair Powell's upcoming speech and potential shifts in monetary policy stance remained key factors influencing bullion prices.

Cryptocurrency Market Correction

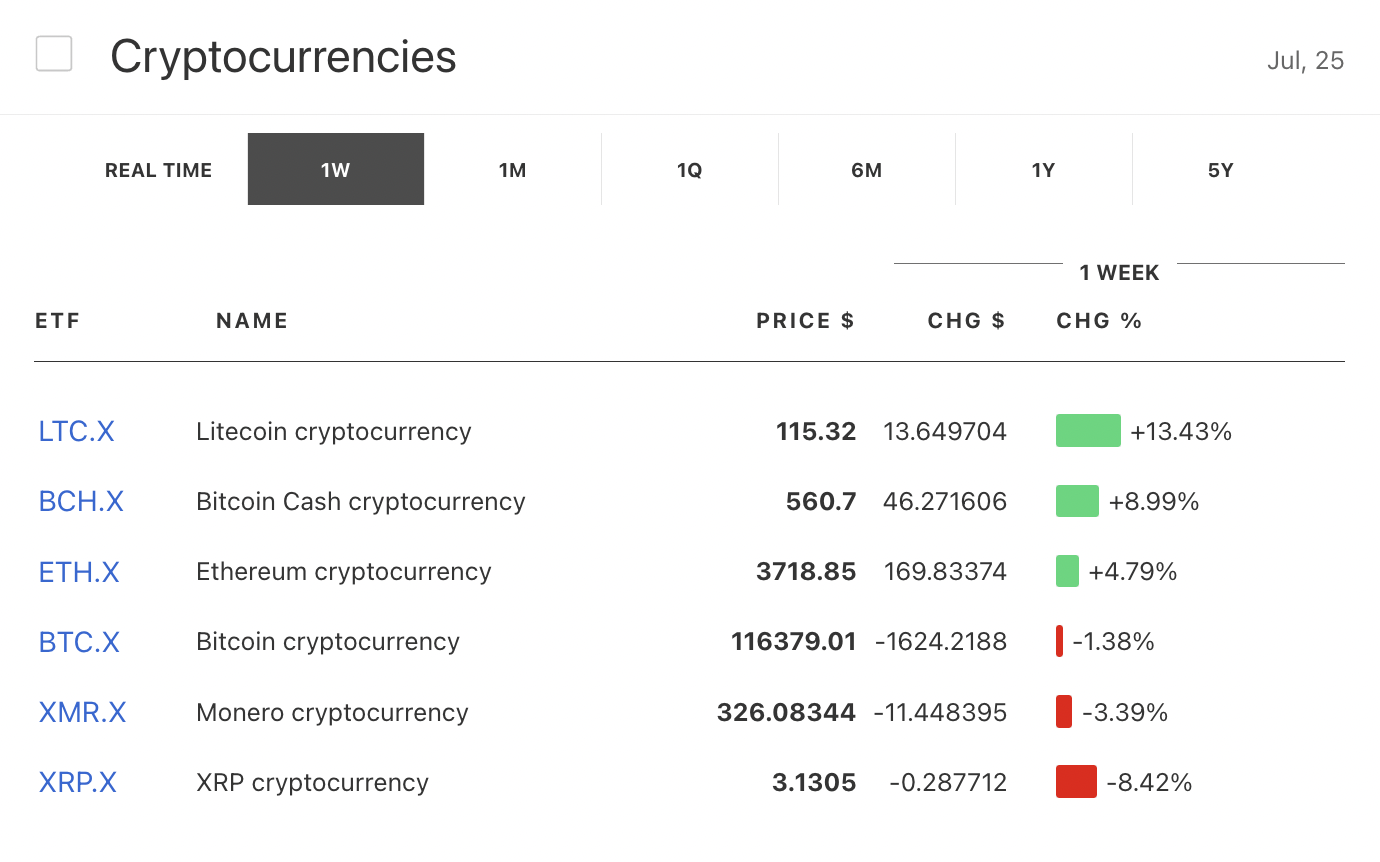

Bitcoin faced selling pressure throughout the week, sliding 6% from recent record highs as traders positioned for the next major catalyst. The cryptocurrency dropped to $115,122 on July 23, marking a 2.72% decline driven by stronger-than-expected jobs data that reduced Federal Reserve rate cut expectations. Bitcoin's decline to near $116,000 reflected the broader risk-off sentiment and concerns about Federal Reserve policy tightening.

The cryptocurrency's performance demonstrated its continued correlation with traditional risk assets, declining alongside equities when economic data suggested prolonged higher interest rates. Market analysts noted that Bitcoin's sensitivity to macroeconomic developments and liquidity dynamics remained elevated.

Electric Vehicle Sector Developments

Tesla's Charging Network Expansion

The electric vehicle sector saw important infrastructure developments, with Lucid Motors gaining access to Tesla's Supercharger network. Lucid shares surged 11% to $3.13 following the announcement that Air sedan owners would be able to use Tesla's charging infrastructure by month-end. This development required a $220 adapter and reduced charging speeds to approximately 50kW, but provided valuable infrastructure access for Lucid customers.

The Supercharger network's expansion to include more non-Tesla vehicles—including Ford, GM, Rivian, and now Lucid—demonstrates Tesla's infrastructure becoming the de facto standard for U.S. electric vehicles. However, analysts warned that increased network usage could lead to longer wait times and potential congestion issues.

Market Outlook and Risk Factors

Technical Analysis and Momentum

Market technicals remained supportive, with both the S&P 500 and Nasdaq achieving multiple record closes and demonstrating strong underlying momentum. Goldman Sachs projected the S&P 500 could rise another 4% to around 6,600 by year-end, while Wells Fargo Securities offered a more optimistic forecast of 7,000—representing an 11% increase driven by long-term AI trends.

However, some analysts cautioned about "intense investor FOMO" and warned that enthusiasm might be fleeting despite strong corporate fundamentals. With approximately 85% of S&P 500 companies beating earnings estimates so far this season, expectations remained elevated for continued strong performance.

Key Risk Factors

Several factors could influence market direction in coming weeks:

Trade Policy Uncertainty: The August 1 tariff deadline remains a critical inflection point, with markets sensitive to any changes in negotiation progress or implementation details.

Monetary Policy Divergence: Differences between Federal Reserve and European Central Bank policies could influence currency markets and international capital flows.

Earnings Sustainability: While current earnings season results have been strong, questions remain about sustainability given economic headwinds and increased competition.

Geopolitical Tensions: Global uncertainties, including trade disputes and regional conflicts, continue to influence market sentiment and safe-haven demand.

Upcoming Catalysts

The following week promises additional market-moving events:

Federal Reserve Meeting: The July 30-31 FOMC meeting will provide crucial guidance on interest rate policy and economic outlook.

Additional Earnings: More Magnificent Seven companies, including Apple, Microsoft, Meta, and Amazon, are scheduled to report results.

Trade Negotiations: Continued discussions with the European Union and other trading partners ahead of the August 1 deadline.

Economic Data: Additional employment and inflation indicators that could influence Federal Reserve policy decisions.

The week of July 21-25, 2025, demonstrated financial markets' ability to achieve new heights while navigating complex challenges. Record-breaking equity performance, mixed but generally strong corporate earnings, and progress in trade negotiations created a supportive environment for risk assets. However, underlying tensions regarding monetary policy, trade relationships, and economic sustainability suggest continued vigilance will be necessary as markets advance into the final months of 2025.

The combination of artificial intelligence-driven growth, infrastructure investments, and evolving trade relationships positions markets for potential continued advancement, though investors must remain attentive to policy changes and global developments that could influence this trajectory. As earnings season continues and policy decisions unfold, the coming weeks will likely prove equally significant in determining market direction for the remainder of 2025.