The Rapid Ascent of Verona Pharma: How the Stock of VRNA Increased 122% in Just Three Months

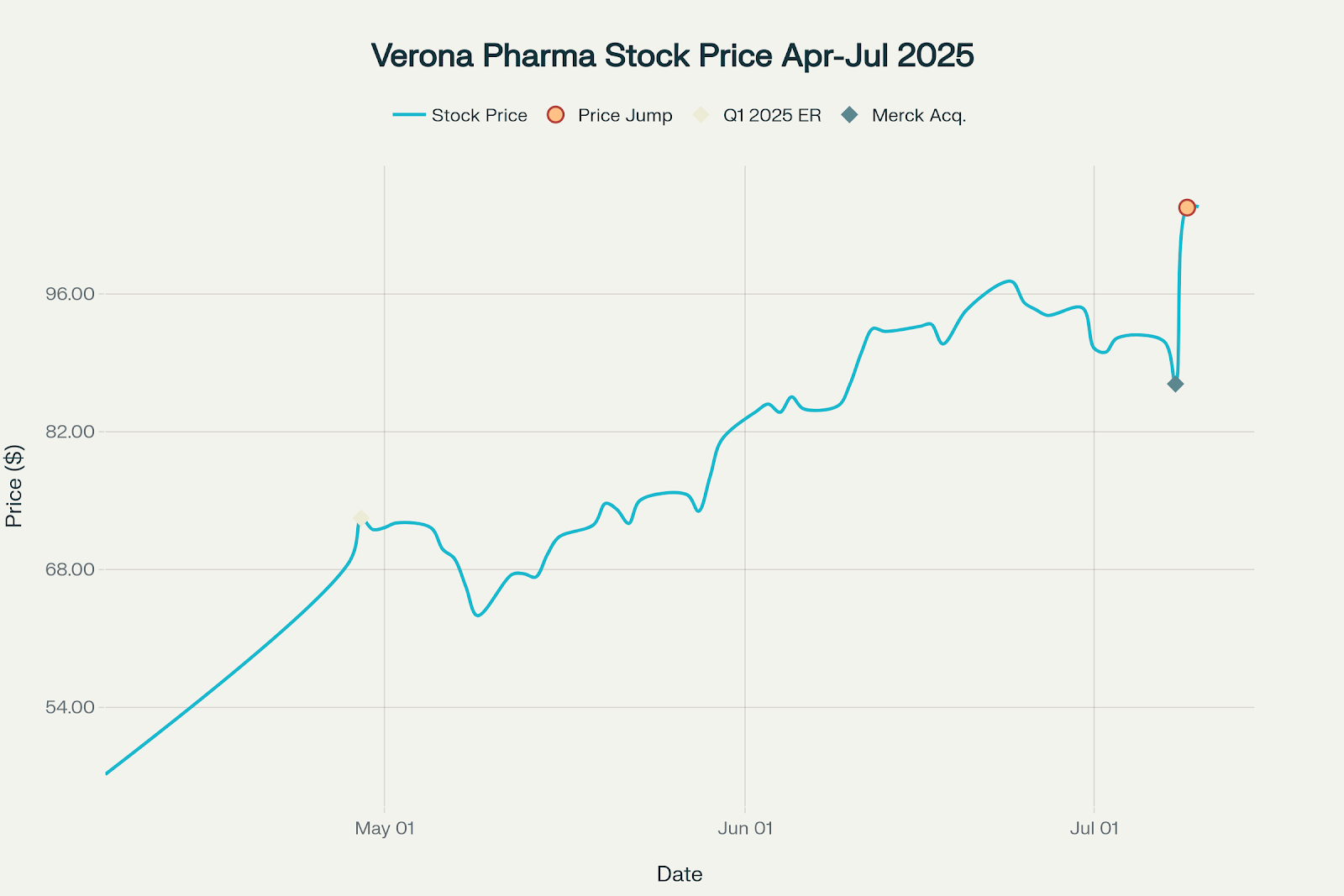

Verona Pharma plc (VRNA) has delivered one of the most spectacular stock performances in the biopharmaceutical sector, with shares skyrocketing 122% from their April 7, 2025 low of $47.20 to the July 10, 2025 closing price of $104.85. This remarkable ascent culminated in Merck's $10 billion acquisition announcement on July 8, 2025, representing a 23% premium to the previous day's closing price. The journey from a struggling biotech to a $9 billion market cap acquisition target represents a masterclass in successful drug commercialization and strategic value creation.

Verona Pharma (VRNA) Stock Price Performance: April 7 - July 10, 2025

Understanding Verona Pharma: The Company Behind the Success

Core Business and Mission

Verona Pharma plc is a UK-based biopharmaceutical company founded in 2005 and incorporated in England and Wales. The company has devoted nearly two decades to developing innovative therapeutics for respiratory diseases with significant unmet medical needs. Headquartered in London with operations in Raleigh, North Carolina, Verona Pharma has transformed from a clinical-stage biotech into a commercial-stage pharmaceutical company with its flagship product Ohtuvayre.

The Ohtuvayre Breakthrough: A First-in-Class Innovation

At the heart of Verona Pharma's success lies Ohtuvayre (ensifentrine), a groundbreaking treatment for chronic obstructive pulmonary disease (COPD). This first-in-class selective dual inhibitor of phosphodiesterase 3 and 4 (PDE3 and PDE4) enzymes represents the first novel inhaled mechanism for COPD maintenance treatment in over 20 years. The drug combines bronchodilator and non-steroidal anti-inflammatory effects in a single molecule, delivered directly to the lungs through a standard jet nebulizer.

The FDA approved Ohtuvayre on June 26, 2024, for the maintenance treatment of COPD in adult patients. This approval was based on extensive clinical data from the Phase 3 ENHANCE trials, which demonstrated statistically significant improvements in lung function and substantial reductions in COPD exacerbations.

The Market Opportunity: COPD's Multi-Billion Dollar Potential

Market Size and Growth Trajectory

The COPD treatment market represents a massive commercial opportunity. The global COPD treatment market was valued at approximately $19.76 billion in 2024 and is projected to reach $37.26 billion by 2037, growing at a compound annual growth rate (CAGR) of 5%. In the seven major markets (US, France, Germany, Italy, Spain, UK, and Japan), the COPD market is forecast to grow from $11.6 billion in 2023 to $30.2 billion by 2033, representing a CAGR of 10%.

Merck specifically noted that the COPD market is expected to grow from $17 billion in 2025 to $27 billion by 2032. This growth is driven by an aging population, increased environmental pollution, and the persistent impact of smoking-related diseases.

Patient Population and Unmet Need

COPD affects approximately 400 million individuals globally, with 8.6 million receiving treatment in the United States alone. The disease is characterized by progressive airway obstruction, persistent symptoms including breathlessness and coughing, and frequent exacerbations that significantly impact patient quality of life and healthcare costs.

Despite existing treatments, most patients continue to experience daily symptoms and exacerbations, highlighting the significant unmet medical need that Ohtuvayre addresses. The drug's unique dual mechanism of action positions it to serve this underserved patient population effectively.

The Three-Month Journey: Key Catalysts and Milestones

Q1 2025 Earnings: The Foundation for Success

The transformation began with Verona Pharma's outstanding Q1 2025 financial results announced on April 29, 2025. The company reported total net revenue of $76.3 million, driven primarily by Ohtuvayre net sales of $71.3 million, representing a remarkable 95% increase compared to Q4 2024.

Key performance metrics that impressed investors included:

- Approximately 25,000 prescriptions filled in Q1 2025

- New patient starts increased by over 25% compared to Q4 2024

- Refills represented approximately 60% of prescriptions, indicating strong patient retention

- The prescriber base expanded to 5,300 healthcare professionals

For the first time in the company's history, quarterly revenue exceeded operating expenses excluding non-cash charges, marking a significant milestone toward profitability.

Commercial Execution Excellence

Verona Pharma's commercial strategy demonstrated exceptional execution throughout the period. The company expanded its field-based sales team and announced plans to add approximately 30 new sales representatives in Q3 2025 to accelerate market penetration. This expansion reflects management's confidence in the drug's commercial trajectory and the significant market opportunity.

The company's specialty pharmacy distribution model proved highly effective, with partners maintaining optimal inventory levels of 2-3 weeks and ensuring broad patient access. The gross-to-net discount improved significantly throughout the period, falling to "well below 20%" by the end of Q1 2025, indicating favorable pricing dynamics and payer acceptance.

Strategic Partnerships and Global Expansion

Verona Pharma's strategic partnership with Nuance Pharma for Greater China development continued to yield positive results. In March 2025, Nuance Pharma completed the last treatment of the final patient in their Phase 3 clinical study, triggering a $5 million milestone payment to Verona. Additionally, Nuance Pharma announced approval of Ohtuvayre in Macau for COPD maintenance treatment in February 2025, marking the first regulatory approval outside the United States.

Pipeline Advancement and Future Opportunities

The company made significant progress advancing its clinical pipeline during the period. Verona Pharma initiated two Phase 2 studies: one evaluating ensifentrine for non-cystic fibrosis bronchiectasis (NCFBE) and another assessing a fixed-dose combination of ensifentrine and glycopyrrolate for COPD maintenance treatment.

The bronchiectasis opportunity represents a substantial additional market, as NCFBE is a chronic lung disease with no FDA-approved treatments. The fixed-dose combination with glycopyrrolate (a long-acting muscarinic antagonist) could further expand Ohtuvayre's addressable market in COPD by providing enhanced bronchodilation.

Analyst Recognition and Market Validation

Wall Street's Growing Confidence

Throughout the three-month period, Verona Pharma garnered increasing analyst attention and positive coverage. The momentum culminated with Wolfe Research initiating coverage on July 1, 2025, with an "outperform" rating and a $170 price target. This bold price target reflected confidence in the company's commercial execution and long-term growth prospects.

Other notable analyst actions included:

- Cantor Fitzgerald raising their price target from $90 to $100 with an "overweight" rating

- HC Wainwright increasing their price target from $85 to $90 with a "buy" rating

- Multiple firms maintaining positive ratings throughout the period

Institutional Interest and Market Dynamics

The strong commercial performance and positive analyst coverage attracted significant institutional interest. By the end of Q1 2025, 149 institutional investors had added VRNA shares to their portfolios, while only 102 decreased their positions. This institutional backing provided important validation and contributed to the stock's upward trajectory.

The Merck Acquisition: Strategic Rationale and Financial Impact

Deal Structure and Valuation

On July 8, 2025, Merck announced its agreement to acquire Verona Pharma for $107 per American Depositary Share (ADS), representing a total transaction value of approximately $10 billion. The offer represented a 23% premium to Verona's closing price on July 8 and a 39% premium to the 60-day volume-weighted average price.

The acquisition represents Merck's largest biotech deal since the $11.5 billion Acceleron acquisition in 2021 and $10.8 billion Prometheus acquisition in 2023. The deal is expected to close in Q4 2025, subject to regulatory approvals and shareholder approval.

Strategic Fit and Rationale

For Merck, the acquisition aligns perfectly with its strategy to diversify revenue streams ahead of Keytruda's patent expiration in 2028. Keytruda generated $29.5 billion in sales in 2024, representing 46% of Merck's total revenue. The addition of Ohtuvayre provides Merck with a first-in-class COPD treatment with significant growth potential.

The acquisition also complements Merck's existing respiratory portfolio, including Winrevair for pulmonary arterial hypertension. The shared prescriber base between these conditions creates meaningful commercial synergies, with many physicians treating both COPD and PAH patients.

Financial Projections and Market Potential

Analysts project Ohtuvayre could achieve peak annual sales of approximately $4 billion by the mid-2030s. Merck expects most of the $10 billion valuation to be derived from US sales, with the company noting that 14,500 physicians in the US treat COPD patients. Given that 5,300 healthcare professionals had already prescribed Ohtuvayre by Q1 2025, significant expansion opportunity remains.

The drug's favorable profile for combination with existing background therapies makes it particularly attractive, as it can be added to patients' current treatment regimens without requiring significant changes to established care patterns.

Competitive Landscape and Market Positioning

COPD Market Dynamics

The COPD treatment market is dominated by established pharmaceutical giants including GlaxoSmithKline (GSK), AstraZeneca (AZN), Boehringer Ingelheim, and Novartis (NVS). These companies have significant resources and established commercial infrastructures, making market entry challenging for smaller biotech companies.

Key competitive products include GSK's Trelegy Ellipta, AstraZeneca's Symbicort, and Boehringer Ingelheim's Spiriva. However, Ohtuvayre's unique dual mechanism of action and first-in-class status provide significant differentiation from these established therapies.

Emerging Competition

The COPD market is experiencing increased innovation, with several new entrants targeting different patient populations. GSK's Nucala received FDA approval in May 2025 as an add-on maintenance treatment for adults with inadequately controlled COPD and an eosinophilic phenotype. Additionally, Amgen and AstraZeneca are developing their asthma drug Tezspire as a potential COPD treatment.

Despite increasing competition, Ohtuvayre's broad indication for COPD maintenance treatment and its ability to be used as monotherapy or in combination with existing treatments provide significant competitive advantages.

Financial Performance Analysis

Revenue Growth and Trajectory

Verona Pharma's financial transformation has been remarkable. The company generated $42.3 million in net product sales for full-year 2024, with Q4 2024 sales of approximately $36 million. The Q1 2025 performance of $71.3 million in net sales represents a 95% sequential increase, demonstrating exceptional commercial momentum.

The company's revenue trajectory suggests strong continued growth, with analysts projecting Q2 2025 Ohtuvayre sales of $91.8 million and full-year 2025 sales of $409.1 million. This growth is driven by expanding prescriber adoption, increasing patient starts, and strong retention rates.

Path to Profitability

A significant milestone achieved in Q1 2025 was the company's first quarter where revenue exceeded operating expenses excluding non-cash charges. This achievement demonstrates the strong unit economics of Ohtuvayre and the scalability of Verona's commercial model.

The company reported a net loss of $16.3 million in Q1 2025, significantly improved from the $25.8 million loss in Q1 2024. Adjusted net income (excluding share-based compensation) was $20.5 million, compared to an adjusted net loss of $21.5 million in the prior year.

Balance Sheet Strength

Verona Pharma maintained a strong financial position throughout the period, with cash and cash equivalents of $401.5 million as of March 31, 2025. The company's robust cash position provided the financial flexibility to invest in commercial expansion and pipeline development while maintaining operational independence.

Risk Factors and Considerations

Single Product Dependence

Verona Pharma's success remains heavily dependent on Ohtuvayre's continued commercial performance. While the drug has demonstrated strong early adoption, the company faces risks related to competitive pressure, pricing dynamics, and potential safety or efficacy concerns that could impact future sales.

Regulatory and Market Access Challenges

The company's international expansion plans face regulatory uncertainties, particularly in Europe where Ohtuvayre has not yet received approval. Additionally, healthcare systems' increasing focus on cost containment could impact pricing and reimbursement decisions.

Integration Risks

Following the Merck acquisition, Verona Pharma will face integration challenges as it becomes part of a larger pharmaceutical organization. While Merck's resources and commercial infrastructure offer significant advantages, successful integration will be critical to realizing the full potential of the combination.

Future Outlook and Strategic Implications

Pipeline Development Opportunities

Verona Pharma's pipeline offers multiple opportunities for future growth beyond Ohtuvayre's current indication. The ongoing Phase 2 studies in bronchiectasis and the fixed-dose combination with glycopyrrolate represent significant near-term value creation opportunities.

The company is also developing ensifentrine in dry powder inhaler (DPI) and pressurized metered-dose inhaler (pMDI) formulations, which could expand the addressable market and provide additional lifecycle management opportunities.

Global Market Expansion

Under Merck's ownership, Ohtuvayre will have access to global commercial infrastructure and regulatory expertise that could accelerate international expansion. While Merck noted that most of the $10 billion valuation assumes US-focused sales, international markets could provide significant upside potential.

Long-term Market Position

The acquisition positions the combined entity to compete more effectively against established COPD market leaders. Merck's scale, resources, and commercial capabilities should enable more rapid market penetration and prescriber adoption than Verona could achieve independently.

Investment Implications and Market Lessons

Biotech Value Creation Model

Verona Pharma's success demonstrates the significant value creation possible when biotech companies successfully navigate the clinical development process and achieve commercial success. The company's journey from a sub-$50 stock to a $107 per share acquisition target illustrates the potential rewards for investors who can identify and invest in companies with differentiated assets and strong execution capabilities.

Importance of Commercial Execution

The rapid uptake of Ohtuvayre highlights the critical importance of commercial execution in the biotech sector. Verona Pharma's ability to build an effective sales organization, establish favorable payer relationships, and achieve strong prescriber adoption was instrumental in the company's success and ultimate acquisition attractiveness.

Strategic Positioning and Timing

The timing of Merck's acquisition reflects the pharmaceutical industry's need to replace revenue from patent-expiring blockbuster drugs. As large pharmaceutical companies face significant patent cliffs, acquiring successful biotech companies with proven commercial products becomes increasingly attractive, even at premium valuations.

Tickeron: AI-Powered Trading Tools for High-Momentum Stocks

As biotech stories like Verona Pharma show how breakthrough innovation can drive triple-digit returns in weeks, platforms like Tickeron help traders capitalize on such momentum with precision. Tickeron’s AI-based analytics track market behavior in real time, identifying trade opportunities across sectors—from pharmaceuticals and healthcare to tech and crypto.

Whether you’re navigating FDA catalysts, M&A rumors, or earnings surges, Tickeron provides the decision support tools needed to stay agile and informed.

Key features include:

- AI Trading Agents (60min / 15min / 5min): Time-specific machine-learning agents delivering intraday trade ideas based on short-term market patterns.

- AI Pattern Search Engine that detects chart setups with defined breakout levels and statistical confidence.

- Trend Prediction Engine forecasting potential price moves shortly after market open.

- Real-Time Signal Screener offering dynamic buy/sell signals across stocks, ETFs, crypto, and more.

In volatile markets where clinical trials and acquisition news can spark rapid moves, Tickeron gives traders the tools to act quickly and confidently.

Conclusion: A Remarkable Transformation

Verona Pharma's 122% stock price appreciation over three months represents one of the most successful biotech stories in recent years. The company's transformation from a clinical-stage biotech to a $10 billion acquisition target demonstrates the significant value creation possible when innovative science meets exceptional commercial execution.

The success of Ohtuvayre validates the substantial unmet need in COPD treatment and the market's appetite for innovative therapeutics that can meaningfully improve patient outcomes. For Merck, the acquisition provides a strategic asset that can help offset the expected revenue decline from Keytruda's patent expiration while establishing a strong position in the growing COPD market.

For investors, Verona Pharma's story serves as a reminder of the significant opportunities available in the biotech sector, while also highlighting the importance of rigorous due diligence and long-term thinking when evaluating investment opportunities in this high-risk, high-reward sector.

The acquisition marks the end of Verona Pharma's journey as an independent company, but it represents the beginning of a new chapter where Ohtuvayre's potential can be fully realized within Merck's global pharmaceutical platform. As the respiratory disease market continues to evolve, this combination is well-positioned to deliver significant value to patients, healthcare providers, and shareholders alike.

Advertisement

General Information

a r&d company for the treatment of allergic rhinitis and other chronic respiratory diseases

Industry Biotechnology

Advertisement