Joby Aviation’s (JOBY) 240% Surge: Redefining Leadership in the eVTOL Space

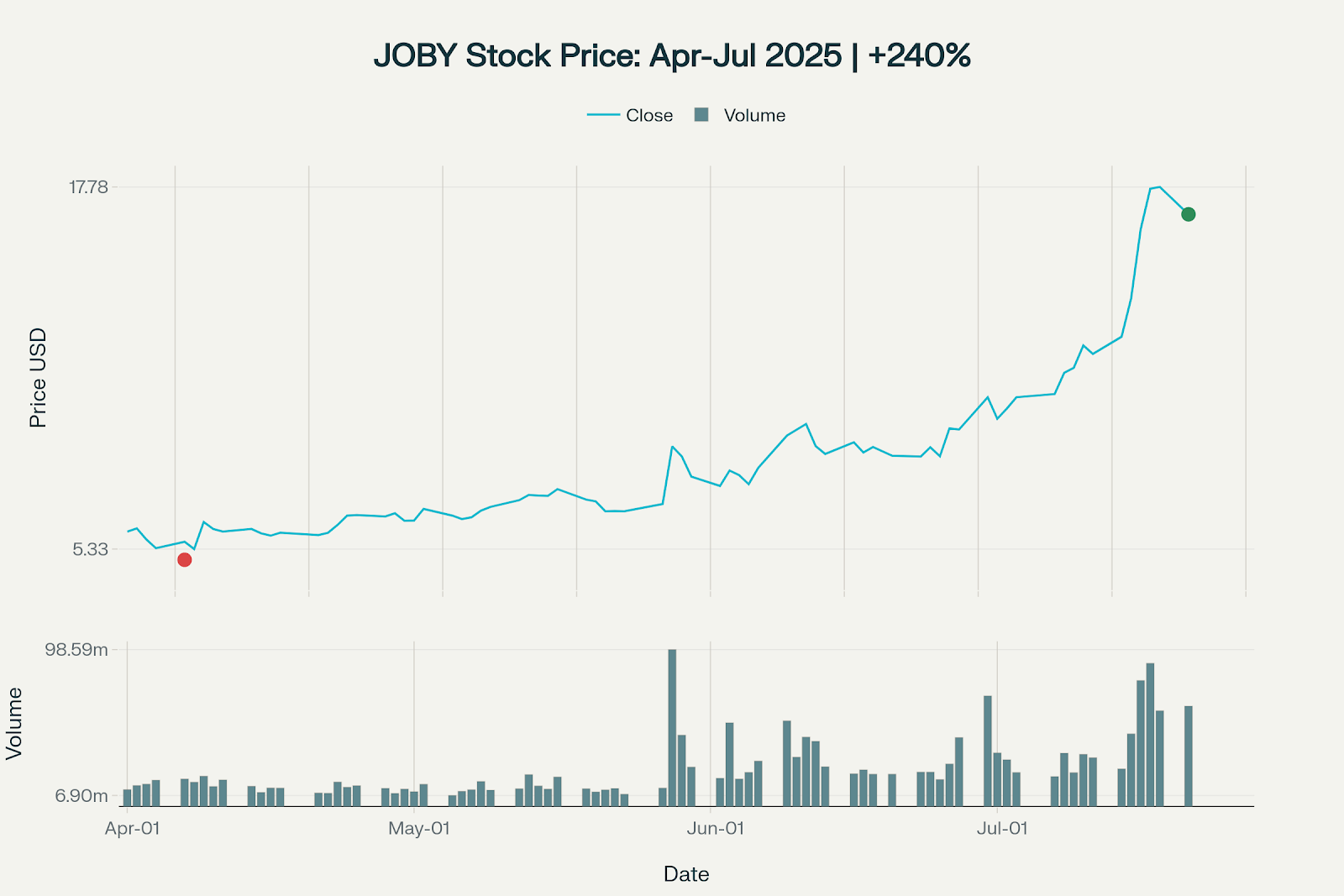

Joby Aviation Inc. (JOBY) has delivered one of the most spectacular performances in the aviation sector during 2025, with its stock price surging approximately 240% from its April low of $4.96 to the July 21 closing price of $16.84. This remarkable rally represents far more than typical market volatility—it signals a fundamental transformation in investor sentiment toward electric vertical takeoff and landing (eVTOL) aircraft and urban air mobility solutions. The company's journey from a speculative aerospace startup to a market leader commanding a $14+ billion valuation demonstrates the convergence of technological breakthroughs, regulatory progress, and strategic partnerships that have redefined the future of transportation.

Joby Aviation stock price surged ~240% from its April 2025 low of $4.96 to July 21, 2025 closing price of $16.84

Understanding Joby Aviation: The eVTOL Pioneer

Core Business and Technology

Joby Aviation stands at the forefront of the electric aviation revolution, developing all-electric vertical takeoff and landing aircraft designed to transform urban mobility. The company's flagship aircraft represents a paradigm shift from traditional transportation, combining the vertical capability of helicopters with the efficiency and environmental benefits of electric propulsion. This five-seat aircraft can transport a pilot and up to four passengers at speeds reaching 200 mph, with a range of up to 100 miles on a single charge.

The technical specifications showcase the sophistication of Joby's engineering approach. The aircraft features six tilting propellers powered by electric motors, enabling seamless transitions between vertical takeoff and horizontal cruise flight. This design philosophy prioritizes safety through redundancy—if one motor fails, the aircraft can still operate safely. The company's commitment to noise reduction has resulted in an aircraft that operates at significantly lower decibel levels than traditional helicopters, making it suitable for urban environments where noise pollution is a critical concern.

Market Positioning and Competitive Advantages

Within the rapidly evolving eVTOL landscape, Joby has established several key competitive advantages that distinguish it from rivals like Archer Aviation, Lilium, and Volocopter. The company's vertically integrated approach encompasses aircraft design, manufacturing, software development, and planned operational services. This comprehensive strategy provides greater control over quality, costs, and timelines compared to competitors who rely on external partnerships for critical components.

Joby's manufacturing capabilities represent another significant differentiator. The company operates multiple facilities across California, including headquarters in Santa Cruz, powertrain development in San Carlos, and expanded production in Marina. The recently announced expansion of the Marina facility doubles production capacity to 435,500 square feet, enabling annual production of up to 24 aircraft once fully operational. This expansion complements the company's Ohio facility in Dayton, which is being retrofitted for component manufacturing with eventual capacity to produce 500 aircraft annually.

The eVTOL Market Revolution

Industry Growth Projections

The electric vertical takeoff and landing aircraft market represents one of the fastest-growing sectors in aerospace, with multiple research firms projecting exceptional growth trajectories. According to MarketsandMarkets, the eVTOL aircraft market will expand from $0.76 billion in 2024 to $4.67 billion by 2030, representing a compound annual growth rate (CAGR) of 35.3%. More aggressive projections suggest even higher growth, with some analysts forecasting the market reaching $23.4 billion by 2030 at a 52% CAGR.

The broader urban air mobility market presents even more substantial opportunities. Eve Air Mobility's Global Market Outlook projects a $280 billion passenger revenue opportunity by 2045, supported by a fleet of approximately 30,000 eVTOL aircraft. These projections reflect growing urban population density, increasing traffic congestion, and heightened environmental consciousness driving demand for sustainable transportation alternatives.

Regional growth patterns indicate North America leading initial adoption, capturing 41.65% of 2024 revenue due to clear FAA regulations and strong defense sector connections. However, Asia-Pacific represents the fastest-growing region at a 28.24% CAGR, driven by rapid urbanization and government support for advanced air mobility initiatives. Europe follows as the second-fastest growing market, with regulatory frameworks from EASA supporting commercial deployment timelines.

Technological and Regulatory Convergence

The eVTOL market's acceleration stems from the convergence of several technological and regulatory factors. Battery technology improvements have reached critical thresholds, with energy densities approaching 500 Wh/kg necessary for commercially viable operations. Simultaneously, advances in electric motor efficiency, autonomous navigation systems, and air traffic management infrastructure are removing traditional barriers to urban air mobility deployment.

Regulatory progress represents another crucial catalyst. The Federal Aviation Administration's establishment of Special Federal Aviation Regulation (SFAR) for powered-lift aircraft in October 2024 created a clear certification pathway for eVTOL operations. Similar regulatory frameworks are emerging globally, with the European Union Aviation Safety Agency (EASA) and other international regulators developing parallel standards that facilitate cross-border operations.

Dissecting the 240% Rally: Key Catalysts and Timeline

April 2025: The Foundation Period

The remarkable stock performance began from a position of relative weakness, with JOBY trading near multi-month lows in early April 2025. The stock reached its trough of $4.96 on April 7, 2025, representing significant pessimism about the company's near-term prospects. This low point coincided with broader market concerns about pre-revenue technology companies and questions regarding the timeline for eVTOL commercialization.

However, April also marked the beginning of several positive developments that would fuel the subsequent rally. The company's Q1 2025 earnings release, scheduled for May 7, was anticipated to provide updated guidance on certification progress and operational milestones. Additionally, manufacturing expansion announcements and partnership developments were creating underlying momentum that would eventually translate into stock price appreciation.

May 2025: Financial Strength and Strategic Partnerships

Toyota Investment Completion

One of the most significant catalysts occurred in late May when Joby announced the closing of the first $250 million tranche from Toyota's total $500 million investment commitment. This capital injection, announced on May 28, 2025, sent JOBY stock soaring 20% in a single trading session as investors recognized the validation and financial security provided by one of the world's largest automakers.

The Toyota partnership extends beyond mere financial investment, encompassing deep manufacturing collaboration that leverages Toyota's production expertise. Toyota engineers are embedded within Joby's operations, providing guidance on design optimization, manufacturing processes, and quality assurance systems. This relationship has already yielded tangible results, with Joby reporting a 30% reduction in final aircraft integration time due to new sub-assembly processes developed with Toyota's support.

Q1 2025 Financial Performance

Joby's Q1 2025 earnings results, released on May 7, demonstrated better-than-expected financial discipline while highlighting significant operational progress. The company reported an earnings per share (EPS) loss of -$0.11, substantially better than analyst expectations of -$0.19, representing a positive surprise of approximately 42%. While the company remains pre-revenue, this performance indicated effective cost management and strategic capital allocation.

More importantly, the earnings report highlighted record certification progress for the second consecutive quarter, with Joby completing 43% of FAA requirements on Stage 4 of the five-stage type certification process. The company also became the first eVTOL manufacturer to conduct routine transition flights with a pilot onboard, marking a critical milestone toward beginning Type Inspection Authorization (TIA) testing with FAA pilots.

June 2025: International Expansion and Market Validation

Saudi Arabia Partnership Agreement

June brought another major catalyst with the announcement of a Memorandum of Understanding between Joby and Abdul Latif Jameel, Saudi Arabia's largest diversified conglomerate. This partnership, announced on June 3, 2025, outlines potential delivery of up to 200 aircraft and related services valued at approximately $1 billion over the coming years.

The Saudi Arabia agreement represents more than a single-market opportunity—it validates Joby's global expansion strategy and demonstrates the scalability of its business model across diverse regulatory and operational environments. Abdul Latif Jameel's 70-year history as Toyota's exclusive distributor in Saudi Arabia creates natural synergies with Joby's existing Toyota partnership. The agreement caused JOBY stock to jump 9% in Tuesday trading following the announcement.

Dubai Operations Progress

Concurrent with the Saudi announcement, Joby made substantial progress on its Dubai operations, which represent the company's first commercial market launch. The partnership with Dubai's Roads and Transport Authority (RTA), originally announced in 2024, gained momentum with the successful completion of piloted wingborne flights in Dubai airspace. These flights marked the transition from testing to operational readiness, demonstrating that Joby's aircraft can perform effectively in the challenging desert environment.

The Dubai operations timeline targets initial passenger service launch in late 2025 or early 2026, making this market crucial for demonstrating commercial viability. Construction of the first vertiport at Dubai International Airport is progressing, with partner Skyports managing infrastructure development to support seamless passenger operations.

July 2025: Manufacturing Scale-Up and All-Time Highs

Production Expansion Announcements

July 2025 marked the culmination of Joby's rally with a series of announcements demonstrating operational scale and manufacturing readiness. On July 15, the company announced the completion of its Marina, California facility expansion, doubling production capacity across 435,500 square feet of manufacturing space. This expansion enables production of up to 24 aircraft annually at the Marina facility, representing nearly one aircraft every two weeks once fully operational.

The manufacturing announcement was accompanied by the rollout of Joby's sixth aircraft, which achieved airworthiness certification within just one week of completion. This rapid certification timeline demonstrates the maturation of Joby's production processes and quality systems, critical factors for scaling commercial operations.

Stock Performance Peak

The combination of manufacturing progress, certification advances, and partnership developments drove JOBY stock to unprecedented levels. The stock achieved its all-time high closing price of $17.78 on July 18, 2025, with intraday trading reaching $18.55. This performance represented a market capitalization exceeding $14 billion and positioned Joby as one of the most valuable pure-play eVTOL companies globally.

Trading volume during this period reached exceptional levels, with daily volumes frequently exceeding 40-60 million shares compared to the typical average of approximately 16 million shares. This increased activity reflected both institutional accumulation and retail investor enthusiasm for the eVTOL sector's commercialization prospects.

Breakthrough Technologies and Operational Milestones

Hydrogen-Electric Flight Achievement

One of the most significant technical breakthroughs contributing to investor confidence was Joby's successful demonstration of hydrogen-electric flight capability. On June 24, 2024 (announced July 2024), Joby's converted aircraft completed a landmark 523-mile flight powered entirely by hydrogen fuel cells, with water vapor as the only emission. This achievement, conducted in collaboration with subsidiary H2FLY, represents a threefold increase in range compared to the battery-electric version and opens entirely new market opportunities for regional transportation.

The hydrogen flight demonstration showcases Joby's technology leadership and positions the company for long-term market expansion beyond initial urban air mobility applications. The ability to achieve 500+ mile range with zero emissions enables point-to-point regional travel between major metropolitan areas without requiring airport infrastructure. This breakthrough has significant implications for total addressable market size and competitive positioning.

FAA Certification Progress

Joby's systematic progress through the FAA certification process represents perhaps the most critical factor in its stock performance. The company has completed three of the five required certification stages and is approximately 43% complete with Stage 4 (Testing & Analysis) requirements. This progress positions Joby ahead of most eVTOL competitors and supports management's timeline for commercial operations beginning in 2025-2026.

The certification process includes several key components:

Certification Stage

Status

Completion Percentage

Stage 1: Project Specific Certification Plan

Complete

100%

Stage 2: Means of Compliance

Essentially Complete

~95%

Stage 3: Conforming Configuration

Complete

100%

Stage 4: Testing & Analysis

In Progress

43% (FAA side), 62% (Joby side)

Stage 5: Type Inspection Authorization (TIA)

Beginning

<10%

The entry into TIA testing represents the final certification hurdle, where FAA test pilots evaluate aircraft performance and safety systems according to previously approved test plans. Joby's achievement of routine piloted transition flights positions the company to begin TIA testing in 2025, a crucial milestone for commercial launch timelines.

Manufacturing and Quality Systems

Joby's manufacturing capabilities have evolved substantially throughout 2025, transitioning from prototype production to scalable commercial manufacturing systems. The company's approach emphasizes vertical integration, with in-house capabilities spanning aircraft design, component manufacturing, system integration, and quality assurance.

The Marina facility expansion exemplifies this integrated approach, incorporating advanced manufacturing technologies including 3D printing, automated assembly systems, and comprehensive testing capabilities. The facility will house Joby's certified full-motion flight simulator, pilot training programs, and aircraft maintenance operations, creating a complete ecosystem for commercial operations.

Quality achievements include the rapid airworthiness certification of new aircraft, with the sixth production aircraft receiving certification within one week of completion. This timeline demonstrates mature quality processes and regulatory familiarity, critical factors for maintaining production schedules as commercial operations commence.

Strategic Partnerships Driving Growth

Toyota Motor Corporation Alliance

The Toyota partnership represents far more than a financial investment—it constitutes a comprehensive strategic alliance that accelerates Joby's path to commercialization. Toyota's total commitment of approximately $894 million (including the initial $394 million investment in 2020 and the current $500 million commitment) makes it Joby's largest shareholder.

The operational benefits of this partnership include:

- Manufacturing Expertise: Toyota engineers embedded within Joby operations provide guidance on production optimization, quality systems, and cost reduction initiatives

- Supply Chain Access: Leverage Toyota's global supplier network for powertrain components, actuation systems, and manufacturing equipment

- Quality Standards: Implementation of Toyota Production System principles to enhance manufacturing efficiency and product reliability

- Technology Sharing: Collaboration on electric propulsion systems, battery management, and autonomous vehicle technologies

Airline Industry Partnerships

Joby has established strategic relationships with major airlines that provide both operational expertise and customer access for commercial launch. The Delta Air Lines partnership, initially announced in 2022, has expanded to include operational planning for U.S. market entry and international expansion. Delta's 49% ownership stake in Virgin Atlantic creates additional synergies for UK market development.

The Virgin Atlantic partnership, announced in March 2025, focuses specifically on UK market entry with plans for zero-emission short-range flights connecting Virgin's hubs at London Heathrow and Manchester Airport. This relationship provides:

- Customer Access: Virgin Atlantic customers can book Joby flights through existing airline channels and loyalty programs

- Regulatory Support: Collaborative engagement with UK Civil Aviation Authority for certification and operational approvals

- Infrastructure Development: Joint development of vertiport networks at major airports and city centers

- Brand Integration: Seamless passenger experience connecting long-haul international flights with short-haul air taxi services

Government and Defense Relationships

Joby's relationships with government agencies and defense organizations provide both revenue opportunities and operational validation. The U.S. Air Force partnership includes delivery of aircraft to Edwards Air Force Base under a $131 million contract. These military applications help validate aircraft performance and safety systems while generating revenue during the commercial certification period.

The company's participation in the FAA's Advanced Air Mobility initiative demonstrates collaboration with regulators on policy development and operational frameworks. This engagement helps ensure that regulatory requirements align with Joby's technical capabilities and commercial objectives.

Financial Performance and Market Dynamics

Capital Structure and Liquidity Position

Joby's financial position provides substantial runway for commercial launch execution and initial operations scaling. As of Q1 2025, the company maintained $813 million in cash and short-term investments, excluding the additional $500 million commitment from Toyota. This liquidity position, totaling approximately $1.3 billion including committed capital, provides financial flexibility for certification completion, manufacturing scale-up, and initial commercial operations.

The company's cash utilization guidance of $500-540 million for 2025 indicates careful financial management while maintaining aggressive development timelines. This burn rate supports continued certification activities, manufacturing expansion, and operational preparation without requiring additional capital raising in the near term.

Revenue Projections and Business Model

While Joby remains pre-revenue, analyst projections indicate substantial revenue growth potential beginning with commercial operations. Wall Street forecasts suggest the company could achieve $6.2 million in revenue for 2025, growing to $80 million in 2026 and $217.3 million in 2027. These projections reflect initial commercial operations in Dubai and potential U.S. market entry during this timeframe.

The revenue model encompasses multiple streams:

Revenue Source

Timeline

Market Opportunity

Passenger Operations (Direct)

2026+

Premium urban mobility, airport connections

Aircraft Sales (B2B)

2025+

Government, corporate customers, international partners

Maintenance & Support Services

2026+

Recurring revenue from operational fleet

Software/Technology Licensing

2027+

Platform services, air traffic management

Short Interest and Market Dynamics

JOBY stock's dramatic rally occurred against a backdrop of significant short interest, creating conditions for additional price acceleration. As of June 30, 2025, short interest totaled 63.75 million shares, representing 14.24% of the float. This elevated short interest level, combined with positive operational developments, contributed to potential short squeeze dynamics during the stock's rally periods.

The short interest ratio of 3.0 days indicates that covering all short positions would require approximately three days of average trading volume. During periods of positive news flow and increased buying pressure, this dynamic can amplify price movements as short sellers cover positions, adding additional buying pressure to the market.

Competitive Landscape Analysis

Primary Competitors Assessment

The eVTOL market features several well-funded competitors, each pursuing different technological approaches and market strategies. Joby's primary competitors include:

Archer Aviation (ACHR) focuses on urban air mobility with its Midnight aircraft, emphasizing partnerships with United Airlines and rapid production scaling. Archer's approach prioritizes manufacturing efficiency and high-volume production, with partnerships including Stellantis for manufacturing support. The company has raised substantial capital and maintains aggressive commercialization timelines similar to Joby.

Lilium (LILM) represents a different technological approach, utilizing jet-powered eVTOL architecture with 36 ducted fans for longer-range regional transportation. However, Lilium has faced significant financial challenges, with recent reports of insolvency proceedings creating uncertainty about the company's future operations.

Vertical Aerospace (UK-based) develops the VX4 aircraft focusing on European and international markets with partnerships including Virgin Atlantic (prior to the Joby agreement). The company emphasizes safety through conventional aircraft design principles adapted for electric vertical flight.

Volocopter (Germany-based) takes a multirotor approach with the VoloCity aircraft optimized for short urban flights. The company has conducted extensive public demonstrations and maintains partnerships with various European cities for initial operations.

Competitive Advantages Analysis

Joby's competitive positioning reflects several key advantages:

Certification Leadership: Joby is further advanced in FAA certification than most competitors, having completed three of five required stages. This regulatory progress provides first-mover advantages in the critical U.S. market.

Manufacturing Integration: The vertically integrated approach provides greater control over costs, quality, and production schedules compared to competitors relying on external manufacturing partners.

Strategic Partnerships: Relationships with Toyota, Delta Air Lines, and Virgin Atlantic provide manufacturing expertise, operational guidance, and customer access that many competitors lack.

Technology Breadth: The successful hydrogen-electric flight demonstration showcases technical capabilities beyond current battery-electric offerings, positioning Joby for expanded market opportunities.

Financial Strength: The combination of internal cash resources and committed Toyota investment provides superior financial runway compared to many competitors facing capital constraints.

Risk Factors and Market Challenges

Regulatory and Certification Risks

Despite substantial progress, regulatory approval remains the primary risk factor for Joby and the broader eVTOL industry. The FAA certification process is complex and unprecedented for this aircraft category, creating potential for delays or additional requirements that could impact commercial launch timelines. Changes in regulatory standards or safety requirements could necessitate design modifications or additional testing, potentially delaying operations and increasing costs.

International regulatory harmonization presents additional challenges. While Joby has applied for validation with the UK Civil Aviation Authority and other international regulators, each jurisdiction maintains separate requirements that could delay global expansion. Differences in regulatory approaches between countries could fragment the market and complicate operational planning.

Operational and Infrastructure Challenges

The successful deployment of eVTOL services requires substantial infrastructure development beyond aircraft certification. Vertiport networks, air traffic management systems, and ground support operations must be established in coordination with existing aviation infrastructure. Delays in infrastructure development or conflicts with existing airspace users could limit initial operational capabilities.

Pilot training and qualification represent another operational challenge. While Joby has established Part 141 flight training certification and is developing simulator-based training programs, scaling qualified pilot availability to match aircraft production will require substantial coordination.

Market Adoption and Competition Risks

Consumer acceptance of eVTOL transportation remains unproven at commercial scale. While demonstration flights have generated positive responses, sustained commercial operations will require establishing consumer confidence in safety, reliability, and cost-effectiveness compared to existing transportation alternatives. Initial pricing may need to remain elevated to achieve profitability, potentially limiting market adoption rates.

Competitive dynamics continue evolving as multiple well-funded companies pursue similar markets. Success by competitors could fragment market share and impact pricing power. Additionally, traditional aviation companies or automotive manufacturers could enter the market with substantial resources, creating additional competitive pressure.

Financial and Execution Risks

Despite strong liquidity, Joby's pre-revenue status creates ongoing cash utilization pressure. Commercial operations must achieve profitability within reasonable timeframes to avoid additional capital requirements that could dilute existing shareholders. Manufacturing scale-up presents execution risks, as transitioning from prototype to commercial production often encounters unforeseen challenges.

Future Outlook and Investment Implications

Commercial Operations Timeline

Joby's commercial operations timeline centers on Dubai as the initial market, with passenger service targeted for late 2025 or early 2026. This timeline appears achievable based on current certification progress and operational preparation, though regulatory approvals and infrastructure completion remain critical path items. Success in Dubai will provide operational validation and revenue generation while supporting expansion into additional markets.

U.S. commercial operations depend on FAA certification completion, currently projected for 2026 based on Stage 4 progress and anticipated TIA testing timelines. Initial U.S. operations will likely focus on premium markets such as airport connections in Los Angeles and New York City, leveraging partnerships with Delta Air Lines for customer access and operational support.

Analyst Price Targets and Market Sentiment

Wall Street analyst sentiment regarding JOBY stock remains generally positive despite the dramatic price appreciation. Current analyst price targets average approximately $9.33, with a range from $5.00 to $13.00. These targets, established before the recent rally, may require upward revision as operational milestones are achieved and commercial operations approach.

The consensus rating of "Buy" from major analysts reflects confidence in Joby's execution capabilities and market positioning. However, some analysts express caution about near-term upside potential given the stock's substantial appreciation and pre-revenue status. Price target revisions will likely depend on certification progress, operational achievements, and initial commercial results.

Long-Term Market Potential

The long-term outlook for Joby reflects the broader urban air mobility market opportunity, which analysts project could reach $280 billion in passenger revenue by 2045. Joby's positioning as a potential market leader in this emerging sector creates substantial value creation potential, though execution risks remain significant.

Technology evolution, including the hydrogen-electric capabilities demonstrated by Joby, could expand addressable markets beyond initial urban mobility applications. Regional transportation connections, cargo operations, and specialized missions could provide additional revenue growth opportunities as operational experience develops and regulatory frameworks mature.

Tickeron: AI Trading Tools for the Next Generation of Transportation

As companies like Joby Aviation push the limits of what’s possible in air mobility and electric aviation, Tickeron gives traders the tools to identify these high-momentum opportunities early. With advanced machine learning and real-time analytics, Tickeron helps investors navigate breakthrough sectors—from aerospace to AI-driven tech—with confidence and speed.

Tickeron transforms raw market data into actionable insights—ideal for traders following innovation-fueled stocks like JOBY.

Key features include:

- AI Trading Bots (60min / 15min / 5min): Intraday machine-learning agents that generate time-specific trade ideas based on short-term market action.

- AI Pattern Search Engine that spots breakout chart setups with projected targets and statistical confidence.

- Trend Prediction Engine delivering early price forecasts minutes after the opening bell.

- Real-Time Signal Screener scanning thousands of stocks, ETFs, and crypto assets for live buy/sell signals.

When ambitious companies take flight—both literally and financially—Tickeron helps traders stay one step ahead of the curve.

Investment Strategy Considerations

JOBY stock represents a high-risk, high-reward investment opportunity requiring careful position sizing and risk management. The stock's volatility, demonstrated by the 240% rally from April to July 2025, indicates potential for substantial gains or losses based on operational developments and market sentiment.

Investment timing considerations include:

Near-term Catalysts: FAA certification progress, Dubai operations launch, and U.S. market entry timeline updates provide potential positive catalysts through 2026.

Operational Milestones: Manufacturing scale-up, pilot training program development, and infrastructure deployment will indicate execution capability.

Financial Metrics: Revenue generation from initial operations and progress toward profitability will validate business model assumptions.

Competitive Developments: Success or failure of competitors will impact overall market sentiment and Joby's relative positioning.

The investment thesis for JOBY stock ultimately depends on the successful transition from development-stage company to commercial aviation operator. While substantial risks remain, Joby's technological leadership, strategic partnerships, and financial resources position the company favorably for capitalizing on the emerging urban air mobility opportunity. Investors should monitor certification progress, operational achievements, and market development closely while maintaining appropriate risk management given the stock's volatility and pre-revenue status.

The 240% rally from April to July 2025 reflects growing confidence in Joby's commercial prospects, but future performance will depend on executing against ambitious operational timelines and establishing sustainable competitive advantages in an evolving market. Success could generate substantial returns for investors willing to accept the inherent risks of investing in revolutionary transportation technology, while failure could result in significant losses for those unprepared for the volatility inherent in emerging technology investments.

Momentum Indicator for JOBY turns positive, indicating new upward trend

JOBY saw its Momentum Indicator move above the 0 level on September 16, 2025. This is an indication that the stock could be shifting in to a new upward move. Traders may want to consider buying the stock or buying call options. Tickeron's A.I.dvisor looked at 94 similar instances where the indicator turned positive. In of the 94 cases, the stock moved higher in the following days. The odds of a move higher are at .

Technical Analysis (Indicators)

Bullish Trend Analysis

The Moving Average Convergence Divergence (MACD) for JOBY just turned positive on September 15, 2025. Looking at past instances where JOBY's MACD turned positive, the stock continued to rise in of 50 cases over the following month. The odds of a continued upward trend are .

JOBY moved above its 50-day moving average on September 19, 2025 date and that indicates a change from a downward trend to an upward trend.

Following a +1 3-day Advance, the price is estimated to grow further. Considering data from situations where JOBY advanced for three days, in of 256 cases, the price rose further within the following month. The odds of a continued upward trend are .

Bearish Trend Analysis

The RSI Oscillator demonstrated that the stock has entered the overbought zone. This may point to a price pull-back soon.

The Stochastic Oscillator entered the overbought zone. Expect a price pull-back in the foreseeable future.

The 10-day moving average for JOBY crossed bearishly below the 50-day moving average on September 02, 2025. This indicates that the trend has shifted lower and could be considered a sell signal. In of 17 past instances when the 10-day crossed below the 50-day, the stock continued to move higher over the following month. The odds of a continued downward trend are .

Following a 3-day decline, the stock is projected to fall further. Considering past instances where JOBY declined for three days, the price rose further in of 62 cases within the following month. The odds of a continued downward trend are .

JOBY broke above its upper Bollinger Band on September 19, 2025. This could be a sign that the stock is set to drop as the stock moves back below the upper band and toward the middle band. You may want to consider selling the stock or exploring put options.

The Aroon Indicator for JOBY entered a downward trend on September 15, 2025. This could indicate a strong downward move is ahead for the stock. Traders may want to consider selling the stock or buying put options.

The Tickeron Price Growth Rating for this company is (best 1 - 100 worst), indicating steady price growth. JOBY’s price grows at a higher rate over the last 12 months as compared to S&P 500 index constituents.

The Tickeron PE Growth Rating for this company is (best 1 - 100 worst), pointing to average earnings growth. The PE Growth rating is based on a comparative analysis of stock PE ratio increase over the last 12 months compared against S&P 500 index constituents.

The Tickeron Valuation Rating of (best 1 - 100 worst) indicates that the company is significantly overvalued in the industry. This rating compares market capitalization estimated by our proprietary formula with the current market capitalization. This rating is based on the following metrics, as compared to industry averages: P/B Ratio (15.798) is normal, around the industry mean (40.594). JOBY has a moderately low P/E Ratio (0.000) as compared to the industry average of (32.911). JOBY's Projected Growth (PEG Ratio) (0.000) is very low in comparison to the industry average of (1.383). JOBY has a moderately low Dividend Yield (0.000) as compared to the industry average of (0.030). JOBY's P/S Ratio (5000.000) is very high in comparison to the industry average of (146.658).

The Tickeron SMR rating for this company is (best 1 - 100 worst), indicating weak sales and an unprofitable business model. SMR (Sales, Margin, Return on Equity) rating is based on comparative analysis of weighted Sales, Income Margin and Return on Equity values compared against S&P 500 index constituents. The weighted SMR value is a proprietary formula developed by Tickeron and represents an overall profitability measure for a stock.

The Tickeron Profit vs. Risk Rating rating for this company is (best 1 - 100 worst), indicating that the returns do not compensate for the risks. JOBY’s unstable profits reported over time resulted in significant Drawdowns within these last five years. A stable profit reduces stock drawdown and volatility. The average Profit vs. Risk Rating rating for the industry is 66, placing this stock worse than average.

Industry description

Market Cap

High and low price notable news

Volume

Fundamental Analysis Ratings

The average fundamental analysis ratings, where 1 is best and 100 is worst, are as follows

Advertisement

General Information

Industry AirFreightCouriers

Advertisement