Methode Electronics, Inc. (NYSE: MEI), a global manufacturer of electronic components and systems, has long been a player in industries such as automotive, industrial, and consumer electronics. With a focus on custom-engineered solutions, MEI serves a diverse client base, but its stock performance has faced challenges in recent years. This article provides a comprehensive financial analysis of MEI as of June 19, 2025, incorporating earnings reports, dividend policies, market movements, comparisons with correlated stocks, and strategies involving inverse ETFs. It also highlights key market news from June 17, 2025, to contextualize MEI’s position.

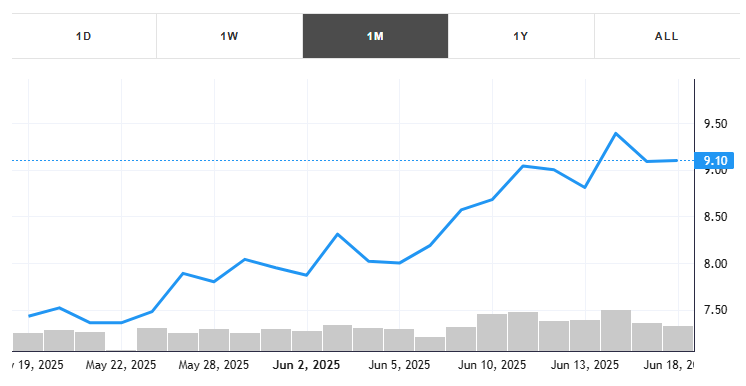

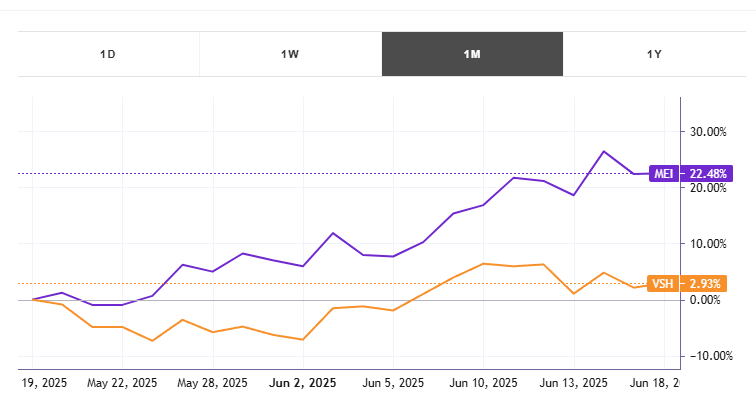

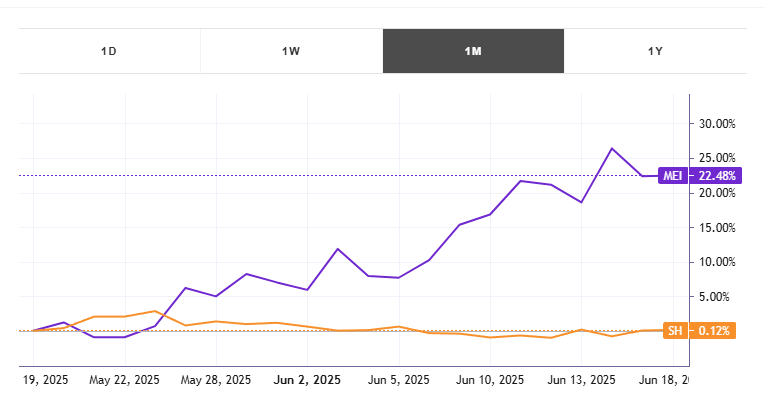

This month, the stock gained +22.48% with an average daily volume of 252722 shares traded.

Company Overview and Financial Snapshot

Methode Electronics designs and manufactures electromechanical devices, including user interfaces, sensors, and power distribution systems. Headquartered in Chicago, Illinois, the company operates across North America, Europe, and Asia, with a significant presence in the automotive sector, which accounted for approximately 65% of its fiscal 2024 revenue. MEI’s market capitalization stands at $325.49 million as of June 18, 2025, reflecting a modest size within the electronics manufacturing industry.

Key financial metrics paint a mixed picture. MEI’s price-to-earnings (P/E) ratio is -3.49, indicating negative earnings and potential investor caution. Its beta of 0.97 suggests volatility roughly in line with the broader market. The stock’s 52-week range spans a low of $5.08 to a high of $17.45, with a current price near $9.13 (based on the 200-day moving average). The 50-day moving average of $7.19 signals a short-term downtrend, underscoring recent struggles.

Earnings Report: Fiscal Q4 2024 and Outlook

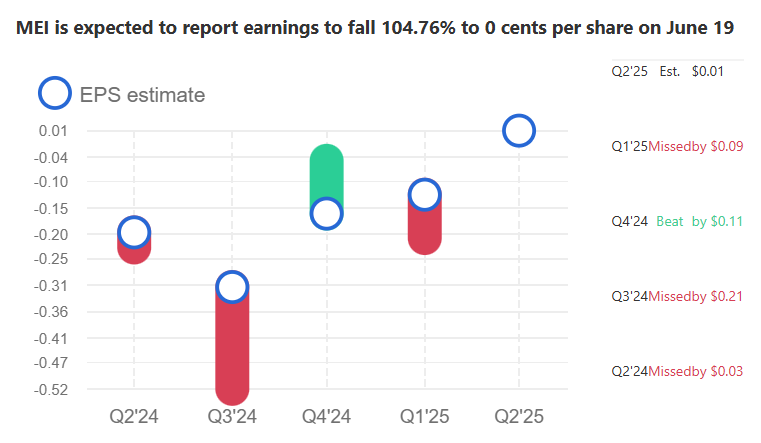

Methode Electronics released its fiscal Q4 2024 earnings (ended April 30, 2024) on July 11, 2024, revealing challenges that have persisted into 2025. The company reported a net loss of $57.9 million, or -$1.63 per share, compared to a net income of $8.1 million, or $0.22 per share, in the prior-year quarter. Revenue declined 8.3% year-over-year to $301.2 million, missing analyst expectations of $312.5 million. The downturn was driven by lower automotive sales in North America and Asia, coupled with operational inefficiencies and higher costs in the Industrial segment.

Management cited supply chain disruptions and softening demand in electric vehicle (EV) programs as key headwinds. However, MEI’s restructuring efforts, including facility consolidations, aim to save $15 million annually by fiscal 2026. For fiscal 2025, guidance projects revenue between $1.15 billion and $1.25 billion, with adjusted EPS ranging from -$0.50 to $0.10, signaling cautious optimism. The next earnings report, expected in early September 2025, will be critical for assessing progress.

Dividend Policy: A Steady Commitment

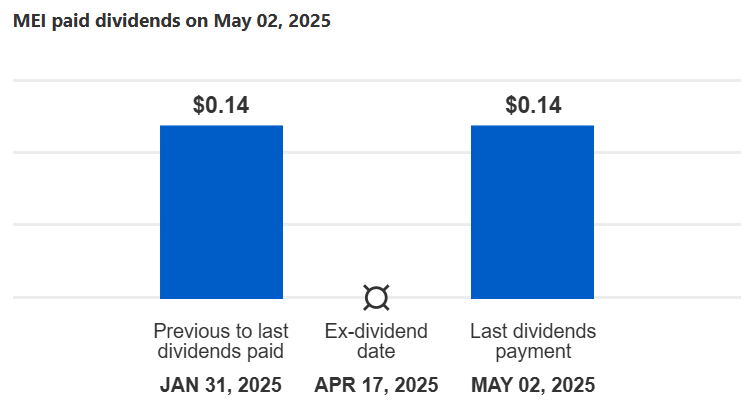

Despite financial challenges, Methode Electronics maintains a consistent dividend policy, appealing to income-focused investors. The company paid a quarterly dividend of $0.14 per share on April 2, 2025, to shareholders of record as of April 18, 2025. This translates to an annualized dividend of $0.56 per share, offering a yield of 6.14% at current prices—a standout feature given MEI’s low valuation.

MEI has a history of stable dividends, with no reductions in the past five years, even amid earnings volatility. The payout ratio, however, is elevated due to negative earnings, raising questions about long-term sustainability if profitability doesn’t recover. For now, the dividend remains a key attraction, particularly in a market where high-yield stocks are sought after, as evidenced by broader U.S. market trends favoring dividend payers in June 2025.

Market Movements: June 17, 2025, Context

On June 17, 2025, U.S. markets displayed cautious optimism, driven by hopes that the Israel-Iran conflict would remain contained. The Dow Jones Industrial Average rose 0.5%, the S&P 500 gained 0.6%, and the Nasdaq Composite climbed 0.7%. Oil prices retreated, easing inflationary fears, while uranium-related stocks surged 7% due to AI-driven nuclear energy demand. These broader trends indirectly influenced MEI, as its industrial and automotive segments are sensitive to energy costs and macroeconomic stability.

MEI’s stock saw modest movement, trading near $9.10 with low volume, reflecting limited catalyst-driven activity. However, a significant development emerged: ME Group International plc, often confused with MEI due to ticker similarity, announced it was exploring strategic options, including a potential sale, sparking brief speculation around MEI. This confusion subsided, but it highlighted MEI’s quiet market presence. Short interest in MEI also dropped 26.1% to 1.05 million shares by May 31, 2025, suggesting reduced bearish sentiment.

Comparison with a Highly Correlated Stock: Vishay Intertechnology (VSH)

Methode Electronics exhibits a high correlation (approximately 0.78 over the past year) with Vishay Intertechnology, Inc. (NYSE: VSH), another electronic components manufacturer serving automotive and industrial markets. Both companies face similar headwinds, including supply chain constraints and EV market fluctuations. As of June 19, 2025, VSH trades at $19.75 with a P/E ratio of 14.2 and a dividend yield of 2.1%, reflecting a stronger earnings profile than MEI’s negative P/E and higher yield.

VSH’s revenue grew 2.1% year-over-year in Q1 2025 to $746.3 million, contrasting with MEI’s decline. However, VSH’s stock has also underperformed the S&P 500, down 15% year-to-date compared to MEI’s 30% decline. Investors may prefer VSH for its profitability but find MEI’s higher dividend yield compelling. Tracking both stocks provides insight into sector trends, with VSH serving as a benchmark for MEI’s recovery potential.

Trading with Inverse ETFs: Hedging MEI Volatility

For traders seeking to capitalize on MEI’s volatility, pairing it with an inverse ETF like the ProShares Short S&P 500 (SH) offers a strategic hedge. SH aims to deliver the daily inverse performance of the S&P 500, which MEI loosely tracks due to its 0.97 beta. Given MEI’s correlation with broader market movements, SH serves as an anti-correlated instrument. For example, if MEI declines 5% amid a market downturn, SH could theoretically gain 5%, offsetting losses.

Inverse ETFs like SH carry risks, including daily rebalancing effects that erode value over time, making them suitable for short-term trades. Traders can use technical indicators, such as MEI’s recent breach of its 50-day moving average, to time entries and exits. This strategy is particularly effective in volatile markets, as seen in June 2025, where geopolitical and economic uncertainties amplified price swings.

AI-Powered Trading Insights

Tickeron, led by CEO Sergey Savastiouk, is revolutionizing trading through its Financial Learning Models (FLMs), which blend advanced technical analysis with AI to uncover market patterns with high accuracy. For a stock like MEI, Tickeron’s tools—including beginner-friendly trading bots, high-liquidity stock robots, and real-time AI insights—offer traders actionable signals. Its AI Trading Bots and Double Agents identify bullish and bearish trends, enabling balanced strategies. By leveraging machine learning, Tickeron enhances decision-making, helping traders navigate MEI’s volatility with precision and aligning with the growing role of AI in finance as of June 2025.

Conclusion: MEI’s Path Forward

Methode Electronics faces a challenging yet intriguing landscape in June 2025. Its negative earnings and revenue declines reflect industry headwinds, but restructuring efforts and a robust 6.14% dividend yield offer hope for long-term investors. Market movements on June 17, 2025, underscored MEI’s sensitivity to macroeconomic factors, while comparisons with Vishay Intertechnology highlight its relative undervaluation. Trading strategies involving inverse ETFs like SH provide opportunities to hedge volatility, and AI-driven tools empower traders with precision.

3rd party Ad. Not an offer or recommendation by Investing.com.

Investors should monitor MEI’s upcoming earnings and restructuring progress closely. While risks remain, its low valuation and high yield make it a candidate for patient, value-oriented portfolios. As markets navigate uncertainty, MEI’s ability to adapt will determine its trajectory.