Key Points

- Fed Decision: The Federal Reserve kept interest rates steady at 4.25%-4.50%, maintaining projections for two rate cuts in 2025 despite raising inflation forecasts to 3% from 2.7% previously.

- Central Bank Decisions: The Bank of England held rates at 4.25% while the Bank of Japan maintained its 0.5% rate, both citing economic uncertainties.

- Market Volatility: Markets experienced significant swings as Middle East tensions escalated midweek, with the Dow Jones dropping 300 points following President Trump's comments on Iran.

- Dollar Dynamics: The U.S. dollar strengthened following the Fed's hawkish tone on inflation, reversing its previous three-year low position.

- Tech Sector: Microsoft's partnership with OpenAI faced uncertainty, while Meta's aggressive AI hiring spree raised questions about future profitability.

Overview

The week of June 16-20, 2025, was characterized by central bank decisions, geopolitical tensions, and significant market volatility. The week began with optimism as markets shrugged off Middle East concerns, but sentiment shifted dramatically midweek following escalating rhetoric from President Trump regarding Iran and the Federal Reserve's cautious stance on inflation. By week's end, markets had processed these developments alongside key economic data from the UK and Japan, resulting in a complex landscape for investors navigating between monetary policy signals and geopolitical risks.

Financial Markets Weekly Recap

Equities

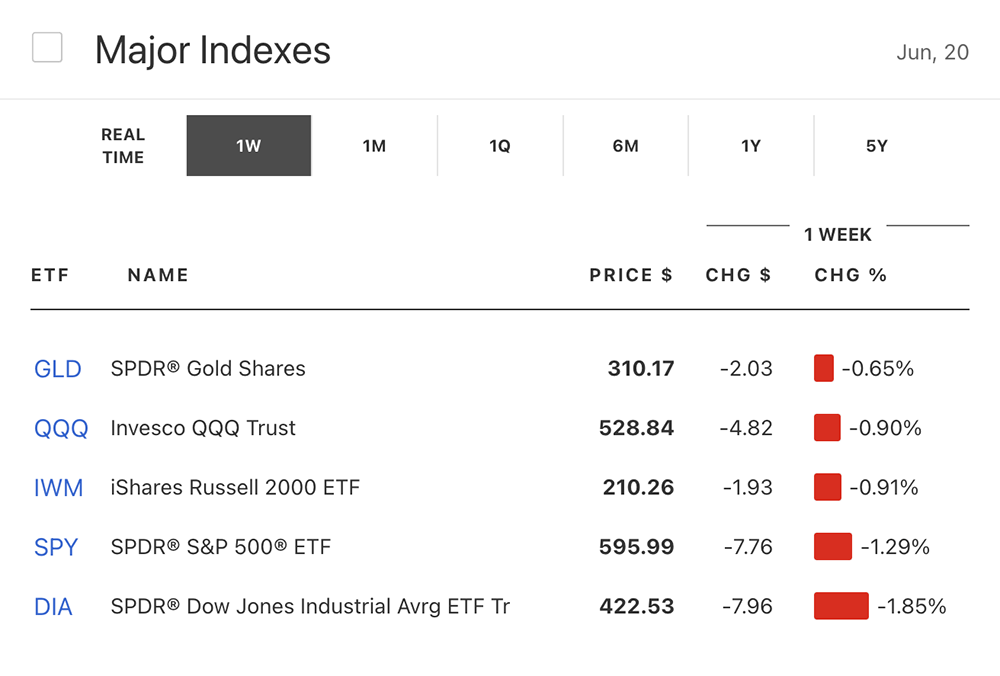

Market Indices: The S&P 500 started the week on a positive note, rising modestly as traders initially showed resilience to Middle East tensions. The Nasdaq Composite posted a strong 1.5% gain on Monday as cooling tensions temporarily boosted tech stocks. However, market sentiment deteriorated Tuesday when the Dow Jones tumbled 300 points following President Trump's provocative comments toward Iran. By Wednesday, following the Fed's decision to hold rates steady while warning of inflation risks, the Nasdaq barely managed to close in positive territory.

Sector Performance: Technology stocks experienced mixed performance, with the Magnificent Seven showing resilience early in the week before facing pressure after the Fed's hawkish tone on inflation. Energy stocks gained as Middle East tensions pushed oil prices higher, while defensive sectors found support amid the uncertainty.

Corporate Highlights:

- Microsoft: Shares slipped 1% as reports emerged that the company might abandon high-stakes negotiations with OpenAI over their partnership's future, with OpenAI reportedly considering alleging anticompetitive practices.

- Meta: The stock sought direction as investors assessed CEO Mark Zuckerberg's aggressive AI hiring spree, including a $14.3 billion investment in Scale AI and the recruitment of its CEO to lead Meta's AI efforts.

Fixed Income and Monetary Policy

Federal Reserve: The FOMC unanimously voted to maintain the federal funds rate at 4.25%-4.50% during its June meeting. While the Fed continued to project two quarter-point cuts by year-end, it revised economic forecasts to show weaker GDP growth of 1.4% (down from 1.7%) and higher inflation of 3% (up from 2.7%). Chair Powell's press conference emphasized that inflation remains "somewhat elevated" and that uncertainty around the economic outlook, while diminished, remains high.

Bank of England: The BoE kept its interest rate unchanged at 4.25% on Thursday, with six out of nine committee members voting for the hold while three favored a 25-basis-point cut. The decision came as UK inflation held steady at 3.4% in May, still well above the bank's 2% target.

Bank of Japan: The BoJ maintained its short-term interest rate at 0.5% on Tuesday, the highest level since 2008. Governor Ueda cited concerns about growth risks and noted that inflation expectations haven't yet reached the 2% level, signaling a cautious approach that could mean no rate hikes before 2026.

Currencies

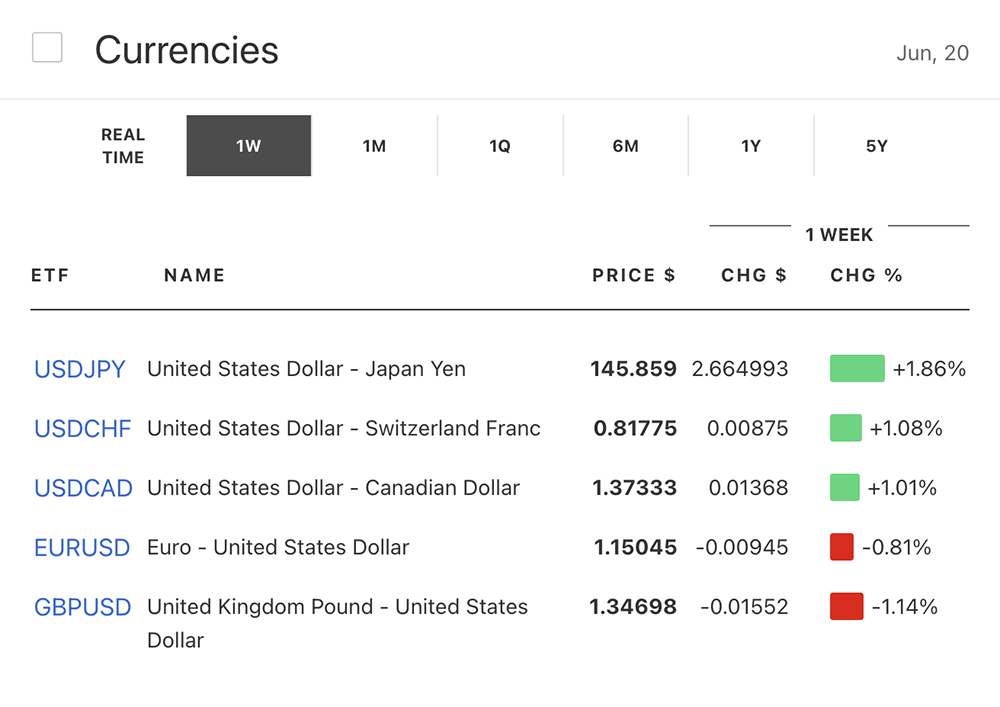

U.S. Dollar: The dollar reversed its downward trend following the Fed's hawkish tone on inflation, sending the euro down to $1.1450 from its previous three-year high above $1.16. The dollar had been languishing near three-year lows earlier in the week but found support as markets reassessed the Fed's rate cut timeline.

Euro: The common currency sank to $1.1450 following Powell's press conference, erasing gains made earlier in the week. The euro had previously benefited from investors seeking alternatives to dollar-denominated assets amid U.S. policy uncertainty.

British Pound: Sterling seesawed above $1.34 after the Bank of England's decision to keep rates flat at 4.25%. The pound had been seeking to rebound following UK inflation data that met consensus expectations at 3.4% for May.

Japanese Yen: The yen remained fragile despite the BoJ's decision to hold rates, trading near ¥144.50. Japan's core inflation jumped to a 28-month high of 3.7% in May, driven largely by soaring rice prices that increased by an astonishing 101.7% year-over-year.

Commodities

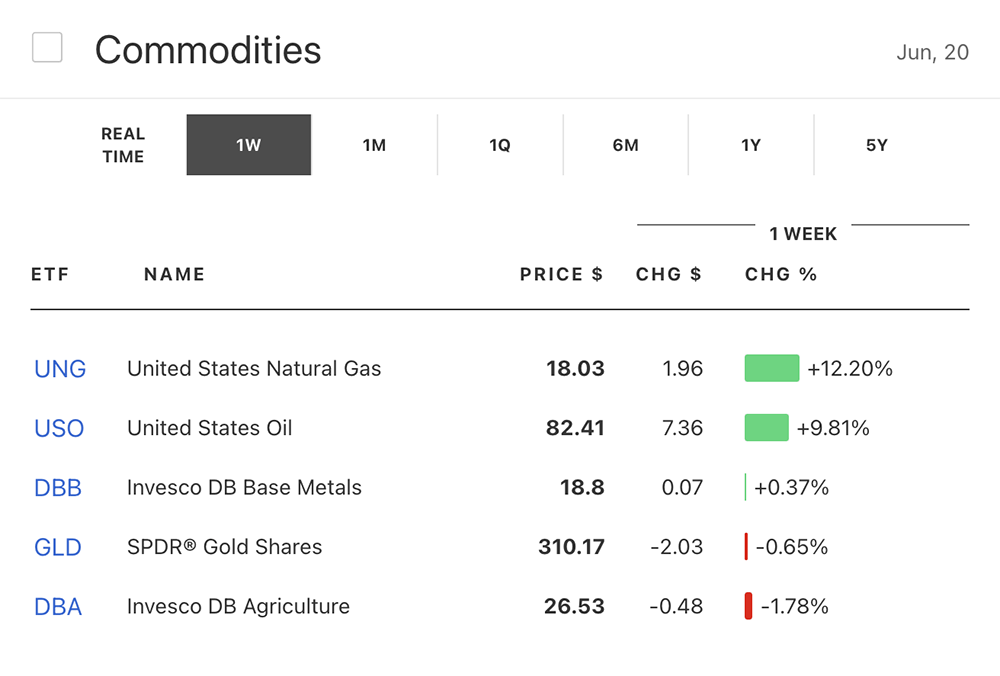

Gold: Gold extended its slide into a third day, breaking below $3,350 in quiet trading after earlier diving under $3,380 as traders braced for the Fed decision. The precious metal had touched $3,452, its highest level in eight weeks, before pulling back sharply amid hopes for diplomatic breakthroughs between Iran and the West.

Oil: Crude prices experienced volatility throughout the week, initially surging on Middle East tensions before moderating as diplomatic efforts to contain the conflict showed signs of progress. The market remained sensitive to President Trump's statements regarding potential U.S. involvement in the Israel-Iran conflict.

Cryptocurrencies

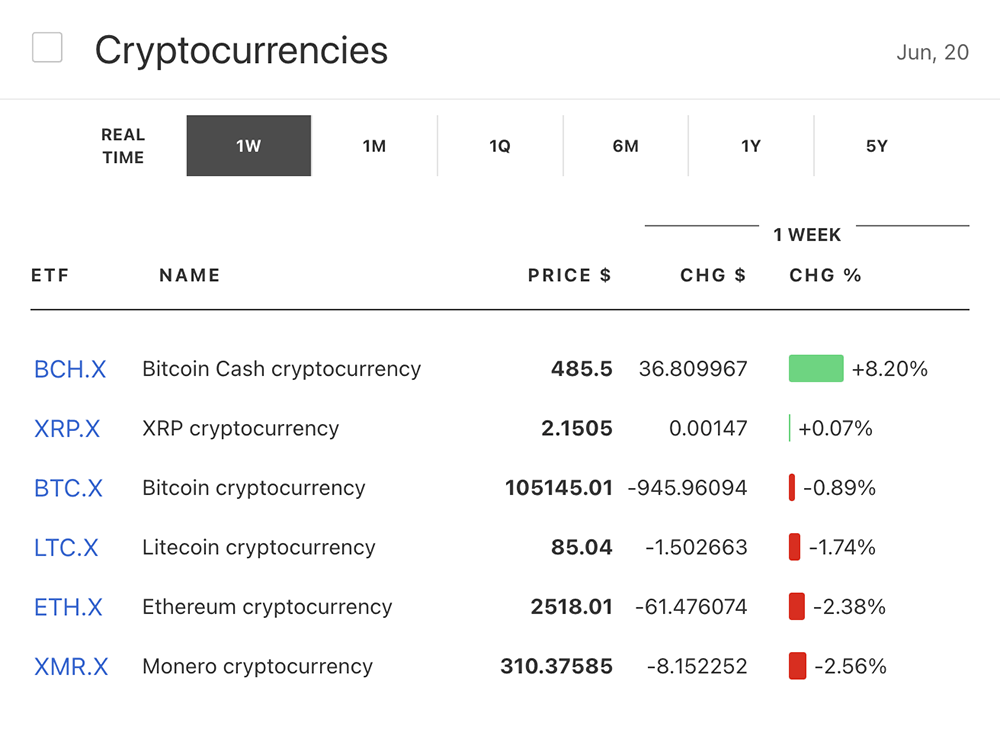

Bitcoin: Bitcoin demonstrated remarkable resilience, holding steady around $104,200 despite the Fed's decision to maintain rates and project higher inflation. The cryptocurrency's stability in the face of broader market volatility highlighted its evolving role as a separate asset class less tied to traditional financial markets.

Ethereum: Ethereum followed Bitcoin's lead, showing relative stability compared to traditional markets, though with less pronounced strength than its larger counterpart.

Economic Indicators and Policy Developments

U.S. Inflation Outlook: The Fed raised its PCE inflation forecast for 2025 to 3% from 2.7% previously, while core PCE inflation was projected at 3.1%, up from 2.8% in March. These revisions signaled the Fed's growing concern about persistent inflation pressures despite slowing economic growth.

UK Economic Data: UK inflation remained steady at 3.4% in May, in line with consensus expectations but still well above the Bank of England's 2% target. This data, coupled with the recent 0.3% GDP contraction in April (the biggest drop in over a year), underscored the challenges facing UK policymakers.

Japan Inflation: Japan's core consumer inflation jumped to 3.7% year-over-year in May, accelerating from 3.5% in April and marking the 38th consecutive month above the BoJ's 2% target. The dramatic rise in rice prices, up 101.7% year-over-year, contributed significantly to this inflationary pressure.

Geopolitical Developments

Middle East Tensions: The week began with a relative cooldown in Israel-Iran hostilities, but tensions escalated dramatically after President Trump's provocative comments demanding the "unconditional surrender" of Iran and suggesting that everyone should "immediately evacuate Tehran". These statements sent markets lower on Tuesday as investors feared potential U.S. involvement in the conflict.

U.S.-China Relations: Trade negotiations between the U.S. and China continued to influence market sentiment, with investors cautiously optimistic about progress following the framework agreement announced the previous week.

Market Outlook

As markets head into next week, investors will be closely watching several key developments:

Inflation Trajectory: With central banks globally maintaining higher rates amid persistent inflation concerns, upcoming inflation data will be crucial in determining the path of monetary policy.

Geopolitical Risks: The evolving situation in the Middle East, particularly any signs of U.S. involvement or further escalation between Israel and Iran, could trigger significant market volatility.

Tech Sector Developments: Microsoft's AI partnership challenges and Meta's aggressive hiring strategy will remain in focus as investors assess the long-term implications for the technology sector.

Central Bank Communications: Any further guidance from Fed officials regarding the timing and pace of potential rate cuts will be closely scrutinized, especially given the revised economic projections.

The week's events have created a complex landscape for investors, with positive developments in some areas counterbalanced by concerning signals in others. This environment suggests continued volatility as markets navigate between monetary policy considerations and geopolitical uncertainties in the coming weeks.