Key Points

- Iran-Israel Ceasefire: A fragile ceasefire between Iran and Israel took effect on June 24, 2025, following US intervention and mediation by President Trump, dramatically shifting market sentiment from risk-off to risk-on.

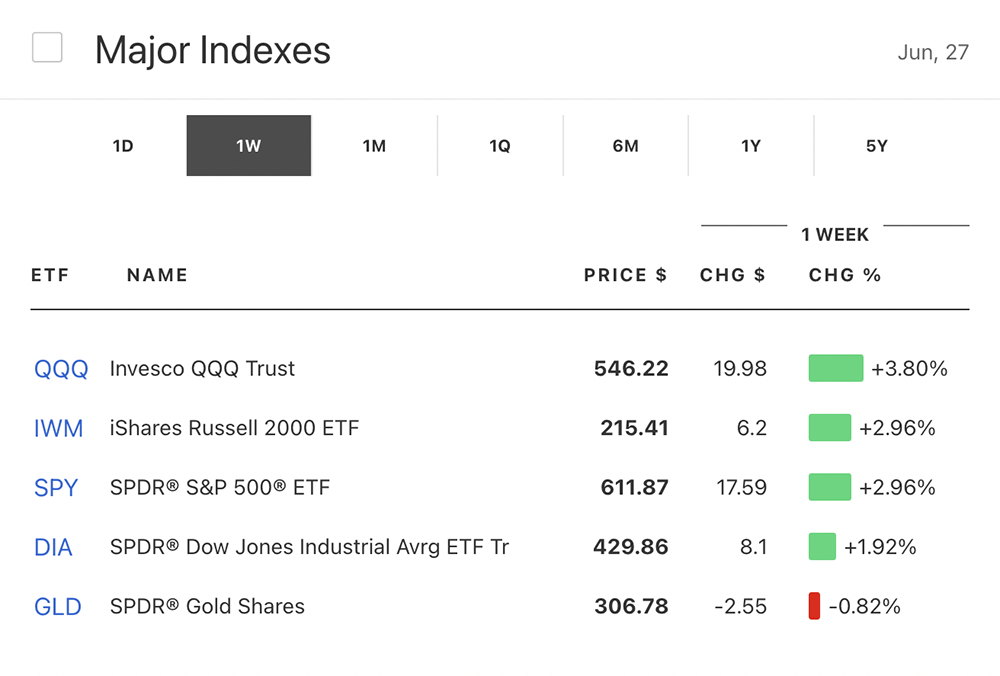

- Market Rally: The S&P 500 (SPY) surged over 1% on Tuesday to within 1% of its February record high, while the Nasdaq (QQQ) climbed to just 8 points below its all-time record.

- Federal Reserve Testimony: Fed Chair Jerome Powell's testimony to Congress suggested potential interest rate cuts could come as early as September, providing market optimism amid inflation concerns.

- Nvidia's Historic Milestone: Nvidia (NVDA) became the first company ever to reach a $3.8 trillion market cap, surpassing Microsoft (MSFT) as the world's most valuable company.

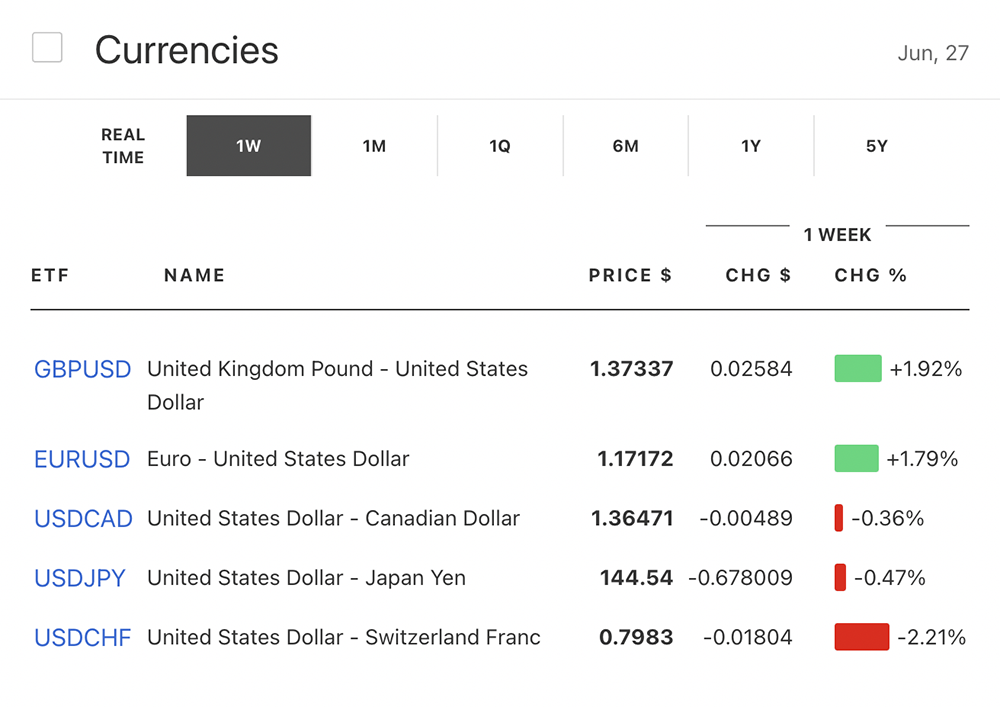

- Dollar Weakness: The US Dollar Index fell to three-year lows near 97.60 as expectations of Fed rate cuts and Trump's early Fed chair replacement comments pressured the greenback.

Overview

The week of June 23-27, 2025, marked a dramatic transformation in global markets as geopolitical tensions gave way to peace talks and risk assets surged. What began as a cautious trading period following the US strikes on Iranian nuclear facilities over the weekend evolved into a broad-based rally as President Trump announced a ceasefire agreement between Iran and Israel. The shift from risk-off to risk-on sentiment propelled major indices toward record highs while triggering significant currency movements and positioning changes across asset classes. The week also featured crucial Federal Reserve testimony that reinforced expectations for monetary policy easing, further supporting the bullish narrative that dominated financial markets by week's end.

Financial Markets Weekly Recap

Equities

Market Indices: The week showcased a remarkable turnaround in equity markets. The S&P 500 (SPY) experienced significant volatility early in the week, with futures initially trading sideways as markets awaited Iran's response to the US strikes. However, the index surged 1.1% on Tuesday following Trump's ceasefire announcement, closing at 6,141.02 and positioning itself within just 1% of its February record high of 6,144. The Nasdaq Composite (QQQ) delivered even stronger performance, jumping 1.4% on Tuesday and continuing its advance throughout the week to finish Thursday at 20,167.91, merely 8 points below its all-time record close. The Dow Jones (DIA) added 1.2% on Tuesday and maintained solid gains, closing Thursday up 1% at 43,386.84.

Sector Performance: Technology stocks led the market rally, with the sector benefiting from both the geopolitical de-escalation and Federal Reserve commentary. The standout performer was Nvidia (NVDA), which achieved a historic milestone by becoming the first company to reach a $3.8 trillion market capitalization, surpassing Microsoft (MSFT) as the world's most valuable company. The chip giant climbed 4.3% on Wednesday to close at $154.31, extending its remarkable 63% gain from its 2025 low and adding over $1.5 trillion in market value since April.

Corporate Highlights:

- Tesla (TSLA): Shares surged 8% on Monday following the company's robotaxi pilot program rollout in Austin, Texas, though the limited scope—just 10 cars in a geofenced area with safety monitors—led to mixed analyst reactions. The stock gained an additional 2% in pre-market trading Tuesday.

- Nike (NKE): The sportswear giant delivered a surprise 12% rally on Friday despite reporting disappointing quarterly results. While revenue fell 12% to $11.1 billion and net income plunged 86% to $211 million, investors focused on forward guidance and CEO Elliott Hill's turnaround strategy. The company expects a $1 billion hit from Chinese tariffs in fiscal 2026 but emphasized long-term supply chain diversification.

Currencies

US Dollar: The greenback experienced significant weakness throughout the week, with the US Dollar Index falling to three-year lows near 97.60. The decline accelerated after President Trump suggested he might name a new Federal Reserve chair "way earlier than expected"—potentially this summer rather than the traditional three to four months before the transition. This unprecedented timeline shift, combined with Powell's dovish testimony, fueled expectations of more accommodative monetary policy ahead.

EUR/USD: The euro surged to nearly four-year highs, breaking above $1.17 for the first time since November 2021. The pair gained 0.7% Thursday to reach $1.1716, marking its sixth consecutive day of gains in one of its strongest bullish streaks in recent memory. The move was primarily driven by dollar weakness rather than euro strength, as the European Central Bank continues its own easing cycle.

GBP/USD: Sterling delivered an impressive performance, breaking through the $1.3760 level to reach four-year highs. The pound gained nearly 400 pips over four days, benefiting from broad dollar weakness and optimism about UK economic resilience. The breakout above the former three-year high at $1.3640 opened the path toward potential targets of $1.39 and even $1.40.

USD/JPY: The yen strengthened significantly against the dollar after initial weakness early in the week. The pair initially surged 1% Monday to ¥147.60 following the US strikes on Iran, but subsequently reversed course as risk sentiment improved and dollar weakness intensified, falling from ¥148.00 to ¥144.84 by week's end.

Commodities

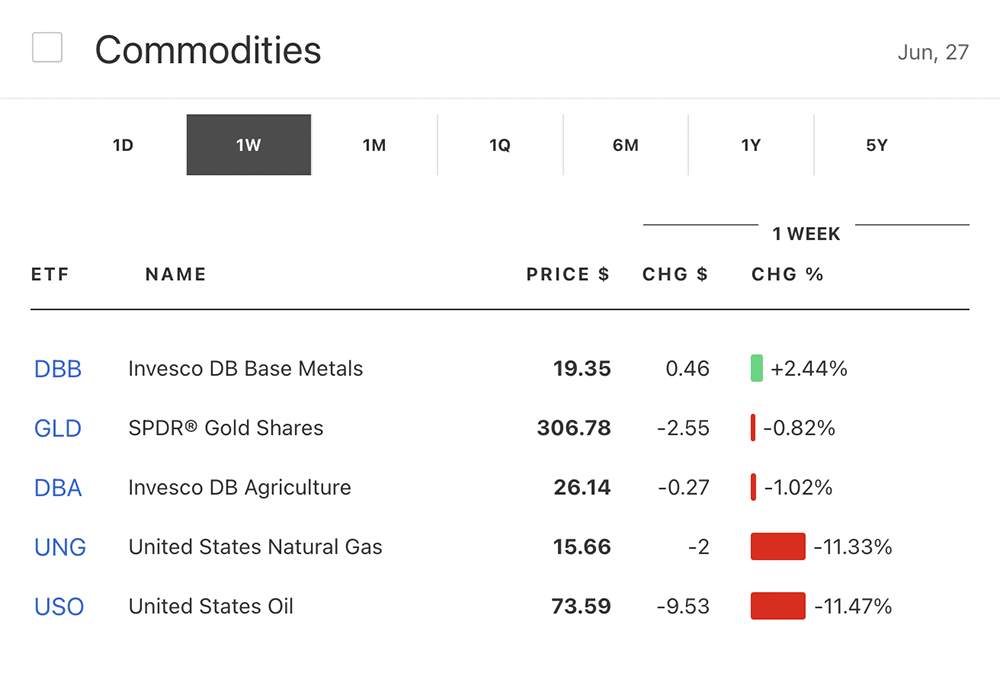

Gold (GLD): Gold prices experienced high volatility as safe-haven demand fluctuated with geopolitical developments. Prices initially traded near elevated levels but fell below $3,330 per ounce on Tuesday after Trump announced the ceasefire agreement. The precious metal faced pressure as investors rotated back into risk assets, with technical indicators suggesting the bears might be taking control in the short term as gold approached its 50-day moving average.

Oil: Crude oil prices remained elevated throughout the week despite the ceasefire announcement, reflecting ongoing supply concerns in the oil-rich Middle East region. The energy sector benefited from these dynamics, with major oil companies posting solid gains during the early part of the week.

Cryptocurrencies

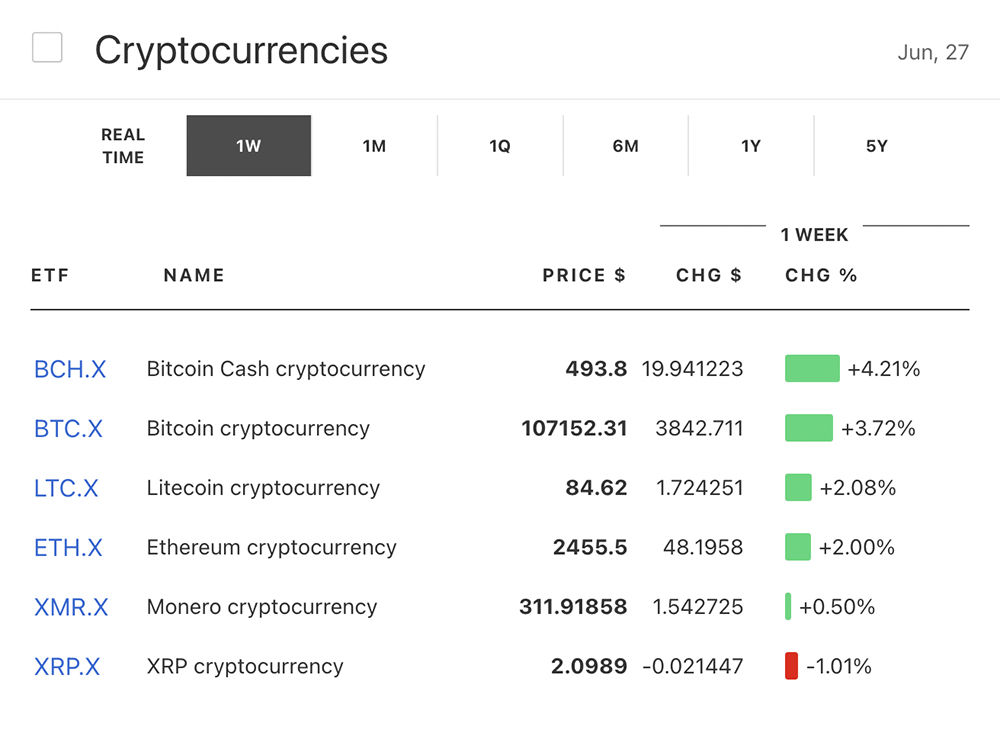

Bitcoin (BTC.X): Bitcoin demonstrated resilience after weekend volatility, recovering from a dip below $98,000 on Sunday to trade back above the $100,000 level by Monday morning. The cryptocurrency reached a session high of $102,000 as risk sentiment improved following the ceasefire announcement. However, broader uncertainty around geopolitical developments and Federal Reserve policy kept the digital asset range-bound.

Ethereum (ETH.X): The second-largest cryptocurrency showed relative weakness, trading around $2,240 and down approximately 2% by Monday. The broader cryptocurrency market remained sensitive to risk sentiment and macroeconomic developments throughout the week.

Economic Indicators and Policy Developments

Federal Reserve Policy: Chair Jerome Powell's testimony to Congress proved market-moving, as he indicated the Fed remains open to cutting interest rates if inflation continues its downward trajectory. Powell stated that if inflation data stays favorable, "we'll get to a place where we can cut rates sooner rather than later," while acknowledging the Fed has guided markets for two more cuts this year with only four policy meetings remaining. Market pricing showed an 18.6% chance of a July cut but an 87% probability of a September reduction.

GDP Data: Thursday's release of Q1 2025 GDP data showed a preliminary contraction of 0.2% on an annualized basis, though this was largely attributed to trade-related distortions as businesses imported goods ahead of potential tariffs. Private domestic final purchases, which exclude the volatile trade component, grew at a solid 2.5% rate.

Inflation Expectations: Markets awaited Friday's release of the Fed's preferred inflation gauge, the core PCE index, with expectations set for a 2.6% year-over-year rise in May, higher than April's 2.5%. The data was viewed as crucial for determining the timing of potential Fed rate cuts.

Geopolitical Developments

Iran-Israel Ceasefire: The most significant development of the week was President Trump's announcement of a ceasefire agreement between Iran and Israel, taking effect on the morning of June 24, 2025. The agreement followed a measured Iranian response to the US weekend strikes, with Iran launching 14 missiles at a US base in Qatar—13 of which were intercepted. Trump's statement that "THE CEASEFIRE IS NOW IN EFFECT. PLEASE DO NOT VIOLATE IT!" marked a dramatic shift from the heightened tensions that had gripped markets.

US Political Developments: Trump's suggestion that he might name a new Federal Reserve chair as early as summer 2025—far ahead of Powell's May 2026 term expiration—created significant market volatility. Among the names reportedly under consideration are Kevin Warsh, Kevin Hassett, Scott Bessent, David Malpass, and Christopher Waller, each with differing views on monetary policy.

Market Outlook

As markets head into the final days of June and the beginning of Q3, several key factors will shape sentiment:

Geopolitical Stability: The durability of the Iran-Israel ceasefire remains paramount, with markets continuing to monitor for any signs of renewed hostilities that could trigger risk-off sentiment.

Federal Reserve Policy: Friday's PCE inflation data and any additional Fed commentary will be crucial for determining whether the central bank will cut rates in July or wait until September. The potential early announcement of Powell's successor adds another layer of complexity to monetary policy expectations.

Record High Watch: Both the S&P 500 and Nasdaq are positioned within striking distance of new all-time highs, with any positive news potentially serving as the catalyst for fresh records.

Dollar Dynamics: The greenback's technical breakdown below key support levels could accelerate if the Fed turns more dovish or if Trump's early Fed chair announcement materializes, potentially benefiting international assets and commodities.

The week's events demonstrated the market's continued sensitivity to geopolitical developments while highlighting the powerful influence of monetary policy expectations on asset prices. The successful de-escalation of Middle East tensions, combined with accommodative signals from the Federal Reserve, has created a constructive environment for risk assets as the second half of 2025 approaches.